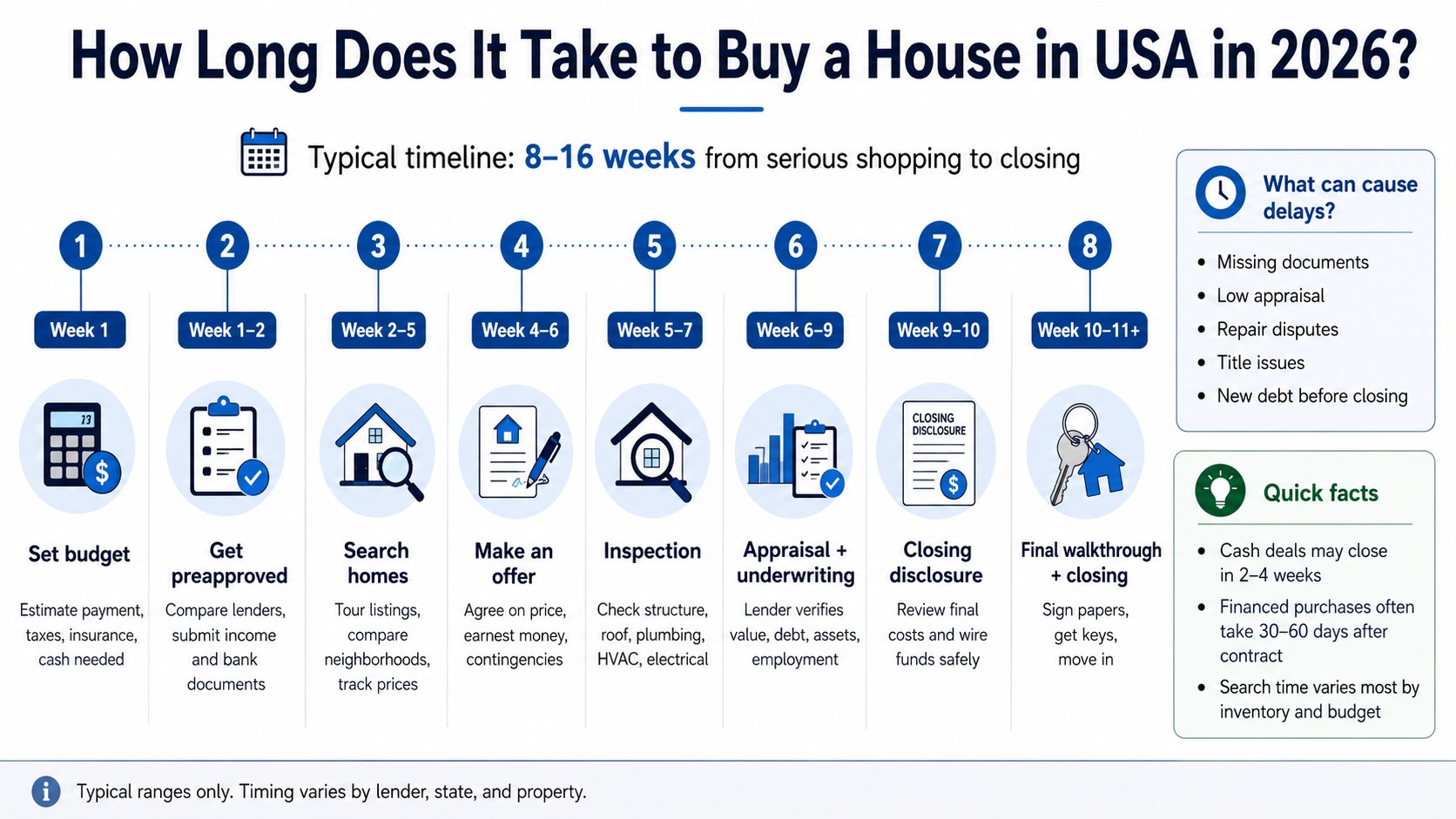

Most buyers should plan on 8 to 16 weeks from serious shopping to closing, but the answer to how long does it take to buy a house in usa depends on financing, inventory, inspections, appraisal timing, and state rules. A cash buyer in Texas or Florida may close in two to four weeks, while a first-time FHA buyer in California, New York, or Maryland may need three to four months, аs noted by Baltimore Chronicle.

This guide gives a week-by-week house buying timeline for the United States in 2026, including what to do, why it matters, and the mistake that slows buyers down. For buyers still at the beginning of the process, Baltimore Chronicle’s guide on how to buy a house in USA in 2026 gives the broader sequence before the timeline becomes urgent.

Key takeaways

- Most financed purchases take 30 to 60 days after contract, plus extra time for searching and preapproval.

- Preapproval, inspection, appraisal, underwriting, title work, and insurance create the main timeline checkpoints.

- Closing delays usually come from document gaps, appraisal issues, repair disputes, title problems, or last-minute credit changes.

How long does it take to buy a house in USA week by week?

A typical buyer needs one to three weeks to prepare, two to eight weeks to find a home, and 30 to 60 days to close after the seller accepts the offer. In a competitive market with limited inventory, the search phase can stretch longer than the mortgage phase.

The national process follows the same pattern, but local details matter. A condo in Chicago may require HOA documents and board review. A rural USDA loan in Georgia may need extra property eligibility checks. A home in Baltimore, Phoenix, or Denver may move faster if the buyer already has a strong preapproval and cash ready for earnest money.

| Phase | Typical 2026 timing | Main risk |

|---|---|---|

| Budget and preapproval | 3 days to 2 weeks | Missing income, tax, or bank documents |

| Home search | 2 to 8 weeks | Low inventory or unrealistic price range |

| Offer and contract | 1 to 7 days | Weak offer terms or slow response |

| Inspection and negotiations | 5 to 14 days | Repair disputes or major defects |

| Appraisal and underwriting | 2 to 5 weeks | Low appraisal or new debt |

| Final review and closing | 3 days to 1 week | Closing Disclosure errors or wire fraud risk |

Buyers who are still deciding whether the numbers work should compare the timeline with Baltimore Chronicle’s breakdown of how much down payment for a house in USA in 2026. The timing often changes once the buyer knows how much cash must stay available for down payment, reserves, inspection, appraisal, and closing costs.

What you need before starting the home purchase process

The fastest buyers collect documents before they tour homes. Lenders such as Rocket Mortgage, Wells Fargo, Chase, Bank of America, Navy Federal Credit Union, and local credit unions usually ask for proof that income, assets, credit, and employment are stable.

- Government ID, Social Security number, and current address history.

- Recent pay stubs, W-2s, 1099s, or profit-and-loss records for freelancers.

- Two years of tax returns if self-employed or using variable income.

- Two to three months of bank, retirement, and investment statements.

- Credit report access and explanations for late payments or large deposits.

- Cash for earnest money, inspection, appraisal, down payment, and closing costs.

- Online accounts for the lender portal, e-signature, insurance quotes, and document uploads.

- Time for showings, calls, inspection appointments, and closing paperwork.

As of 2026, many buyers should budget for earnest money from about $500 to $10,000 depending on price and market norms, inspection fees often in the hundreds of dollars, and closing costs commonly estimated at 2% to 5% of the purchase price. Exact costs vary by lender, state, taxes, insurance, and title company.

Step 1: Set your budget and timeline

- Start with monthly payment, cash available, target move date, and backup housing. Include mortgage principal and interest, property taxes, homeowners insurance, HOA dues, utilities, repairs, and moving costs.

Why it matters: the home buying process in the United States is faster when the buyer knows the maximum payment before seeing listings.

Common mistake to avoid: shopping by list price only and ignoring insurance, taxes, flood coverage, or HOA dues.

HUD’s homebuying guidance starts with affordability, credit rating, monthly expenses, down payment, and interest rate because those factors control the realistic price range. Buyers can also use HUD-approved housing counseling agencies when they need help comparing options.

Step 2: Get mortgage preapproval before touring seriously

- Apply with two or three lenders and compare loan estimates, not just advertised rates. A preapproval usually requires income documents, asset statements, credit review, and permission for the lender to verify debts.

Why it matters: the mortgage preapproval timeline can decide whether a seller takes the offer seriously, especially in markets where Redfin, Zillow, and local MLS listings move quickly.

Common mistake to avoid: relying on a casual prequalification that has not reviewed documents.

The FTC advises mortgage shoppers to get details and terms from several lenders or mortgage brokers before choosing a loan. A slightly lower rate can be less useful than a lender that communicates clearly, closes on time, and explains fees in writing.

Buyers who have not started lender screening can use Baltimore Chronicle’s guide on how to get pre-approved for a mortgage in USA in 2026 before scheduling serious tours. Preapproval is the point where a casual search becomes a purchase plan.

Step 3: Search by neighborhood, property type, and trade-offs

- Use a real estate agent, MLS alerts, Zillow, Realtor.com, Redfin, and open houses to compare homes in the same price band. Track days on market, price cuts, taxes, school zones, commute time, and visible repair needs.

Why it matters: the search phase often determines how many weeks to buy a home more than the closing phase.

Common mistake to avoid: touring homes without ranking must-haves against negotiable features.

Week-by-week search pattern

Week 1 is for listings, lender updates, and neighborhood filters. Weeks 2 to 4 are usually the first serious offer window if the buyer’s price range matches local inventory.

Weeks 5 to 8 often mean one of three things: the buyer is in a tight market, the budget is below the local median, or the search criteria are too narrow. A buyer looking for a detached 3-bedroom home under $350,000 in a high-demand suburb may need more patience than a buyer considering townhomes or smaller square footage.

Step 4: Make an offer and negotiate contract terms

- Submit an offer with price, earnest money, financing type, closing date, contingencies, inspection terms, and seller concessions. The agent should support the offer with comparable sales rather than emotion.

Why it matters: the accepted contract starts the formal timeline to close on a house.

Common mistake to avoid: waiving inspection or appraisal protections without understanding the cash risk.

Offer strength is not only price. A conventional loan with 20% down may look cleaner to a seller than a low-down-payment loan, but FHA, VA, and USDA offers can still win when the buyer is well-prepared and the property condition fits the loan type.

A strong offer removes uncertainty for the seller without creating hidden risk for the buyer.

Step 5: Schedule inspection and handle repairs

- Book the general home inspection as soon as the contract is signed. Add specialty inspections when needed, including roof, sewer scope, termite, radon, well, septic, mold, or structural review.

Why it matters: inspection findings can affect price, credits, repairs, insurance, and whether the buyer continues.

Common mistake to avoid: treating the inspection as a punch list for cosmetic fixes instead of focusing on safety, structure, water, electrical, plumbing, HVAC, and roof life.

Inspection negotiations can take a few days or more than a week. A seller may agree to repair an unsafe electrical panel, offer a closing credit, reduce the price, or refuse changes. The buyer’s leverage depends on the contract, market conditions, and the seriousness of the defect.

Step 6: Complete appraisal, underwriting, title, and insurance

- The lender orders an appraisal, sends the file through underwriting, verifies assets, and checks conditions. The title company or closing attorney searches ownership records, liens, taxes, easements, and payoff details.

Why it matters: this phase determines whether the loan, property value, and legal ownership can support closing.

Common mistake to avoid: opening a new credit card, financing furniture, changing jobs, or moving large deposits without lender guidance.

This is where many delays happen. A low appraisal can trigger a price renegotiation, appraisal gap payment, dispute, or cancellation. Title issues may require payoff letters, estate documents, divorce decrees, lien releases, or corrected legal descriptions.

Buyers comparing fixed-rate, FHA, VA, USDA, jumbo, or adjustable-rate mortgages should keep an eye on current financing conditions. Baltimore Chronicle’s coverage of US mortgage rates and homebuyer costs explains why rate changes can affect monthly payments even when the purchase price stays the same.

Step 7: Review the Closing Disclosure and prepare funds

- Review the Closing Disclosure, final cash-to-close amount, loan terms, monthly payment, taxes, insurance, and closing fees. Confirm wiring instructions by phone using a trusted number, not a number from a suspicious email.

Why it matters: the CFPB says lenders must provide the Closing Disclosure at least three business days before scheduled closing.

Common mistake to avoid: waiting until closing day to question a fee, name spelling, loan term, escrow amount, or seller credit.

The CFPB’s official Closing Disclosure explainer is the best source for checking loan details before signing. The CFPB also warns buyers to stay alert for mortgage closing scams during the final stage of the purchase.

Step 8: Final walkthrough, signing, and keys

- Complete the final walkthrough, verify agreed repairs, check that appliances remain, test major systems, and confirm the home is in the expected condition. Sign closing documents with the title company, escrow officer, attorney, or notary as required by state practice.

Why it matters: this is the last practical chance to catch missing repairs, new damage, or possession problems before ownership transfers.

Common mistake to avoid: skipping the walkthrough because the buyer is busy moving or traveling.

In many states, buyers receive keys after signing and funding. In some attorney states or escrow-heavy markets, recording and fund disbursement may affect the exact handoff time.

Sample 2026 timeline from preapproval to closing

| Week | Buyer action | Expected result |

|---|---|---|

| Week 1 | Collect documents, compare lenders, get preapproved | Clear budget and loan type |

| Weeks 2–5 | Tour homes, monitor listings, refine neighborhoods | Shortlist and first offers |

| Week 6 | Negotiate offer and sign contract | Earnest money deposited |

| Week 7 | Inspection, repair request, insurance quotes | Decision to continue or renegotiate |

| Weeks 8–10 | Appraisal, underwriting, title work | Loan conditions cleared |

| Week 11 | Closing Disclosure, final walkthrough, signing | Ownership transfer and keys |

This example shows an 11-week purchase. A cash buyer may compress it. A buyer using down payment assistance, a VA loan, a condo approval, or a property with title problems may need more time.

Troubleshooting delays before closing

- Preapproval stalls: upload complete documents, explain large deposits, and respond to lender requests the same day.

- Offer keeps losing: adjust price range, improve earnest money, shorten response times, or widen neighborhoods.

- Inspection finds major defects: focus on safety, structural, water, roof, electrical, and HVAC issues before cosmetic items.

- Appraisal comes in low: review comparable sales, renegotiate price, bring gap cash, or use the contingency if available.

- Closing Disclosure looks wrong: contact the lender immediately and compare it with the earlier Loan Estimate.

For official process guidance, HUD’s Buying a Home page covers affordability, rights, loans, homebuying programs, shopping, offers, inspections, insurance, and closing. The FTC’s mortgage shopping FAQs explain why comparing lenders can improve the buyer’s position before committing.

FAQ

Can you buy a house in 30 days in 2026?

Yes, but it is easier with a clean conventional loan, fast appraisal, responsive lender, simple title history, and no major inspection problems. Cash purchases can close faster, but title work, inspections, insurance, HOA documents, and state practices still take time.

How long does mortgage approval take after an offer is accepted?

Mortgage approval after contract often takes two to five weeks, depending on appraisal scheduling, underwriting conditions, borrower response time, and title work. The process slows when buyers change jobs, add debt, miss document requests, or have unexplained deposits.

What is the fastest way to shorten the house buying timeline?

Get fully documented preapproval before touring, keep cash in traceable accounts, avoid new credit, respond to lender requests quickly, and schedule inspections immediately after contract. A realistic offer strategy also reduces wasted weeks.

Does buying a house take longer with FHA, VA, or USDA loans?

It can, depending on property condition, appraisal requirements, eligibility checks, and lender workload. FHA, VA, and USDA loans are common in 2026, but buyers should choose homes that fit the program’s standards and keep extra time for review.

When should a buyer start packing and giving notice?

Start light packing after the contract is stable, but avoid giving nonrefundable notice until inspection, appraisal, and major loan conditions are cleared. Renters should check lease rules, notice periods, and backup housing before relying on an exact closing date.

What causes most last-minute closing delays?

The most common late problems are incorrect Closing Disclosure details, missing insurance, title issues, wire verification concerns, final employment checks, repair disputes, and buyer credit changes. Most are preventable when documents are reviewed several days before closing.

Earlier we wrote about How Long Does IKEA Furniture Last? Real Lifespan by Line in 2026