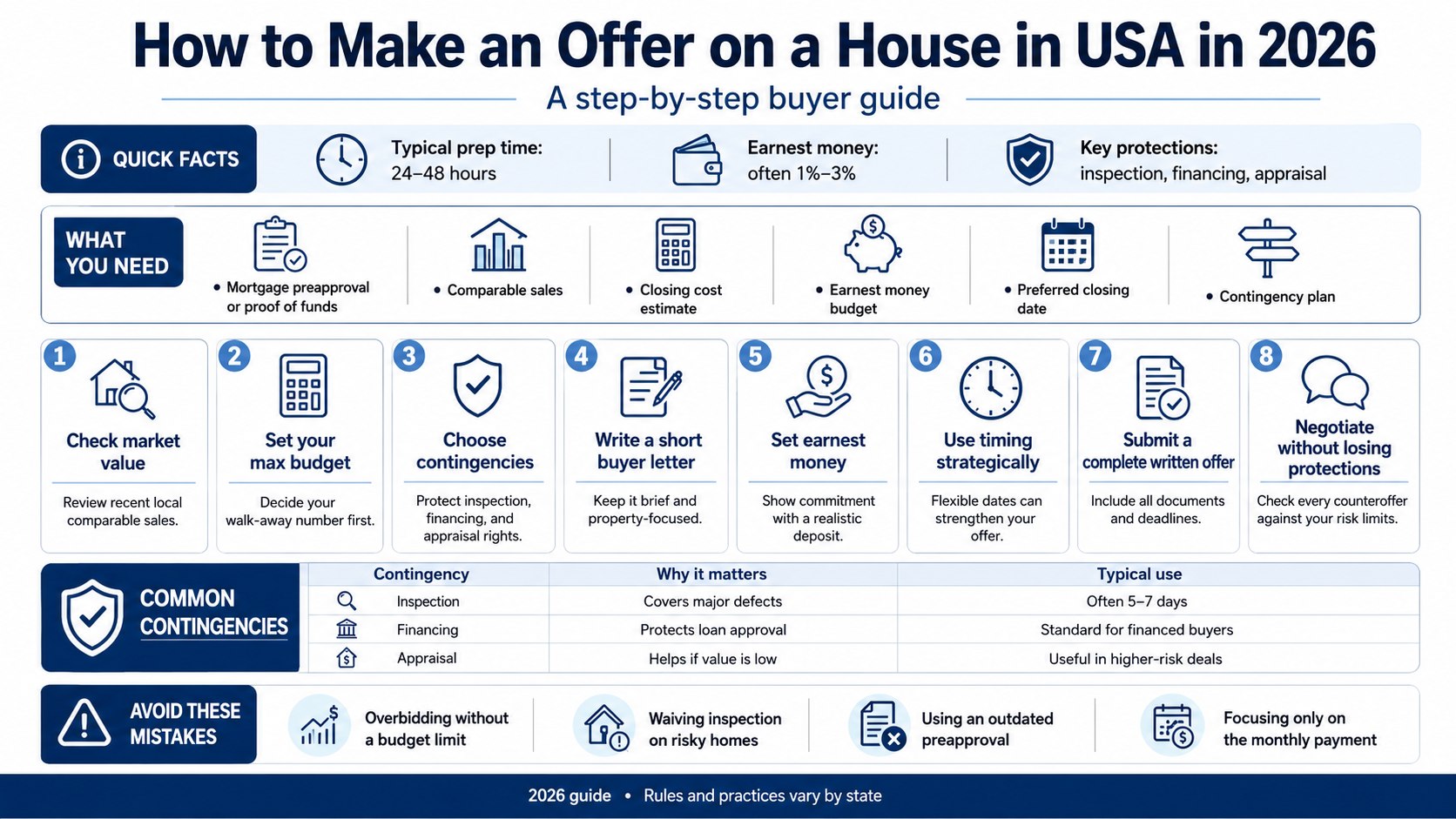

How to make an offer on a house in USA starts with 3 decisions: your price, your contingencies, and your deadline. In 2026, a serious buyer can usually prepare a clean offer in 24–48 hours if financing, proof of funds, and agent documents are ready, as noted by Baltimore Chronicle.

The practical answer is simple: get a fresh lender preapproval, study comparable sales, choose your walk-away number, protect yourself with inspection and financing contingencies, then send a written offer through your real estate agent. The seller does not need your life story. The seller needs confidence that you can close.

Key takeaways

- A strong offer is not always the highest offer; it is the offer least likely to collapse before closing.

- Contingencies protect your deposit, but too many weak conditions can make the seller choose another buyer.

- A buyer letter can help in rare cases, but price, timing, financing, and risk usually matter more.

What you need before making an offer

Before you write a home purchase offer, gather the documents that prove you are real, ready, and financially qualified. A seller in Maryland, Texas, California, Florida, or Ohio will usually compare more than price. They will look at loan strength, closing date, inspection terms, earnest money, and whether your agent communicates clearly.

You should prepare:

- Fresh mortgage preapproval or proof of cash funds

- Recent comparable sales from the same neighborhood

- Estimated closing costs and monthly payment range

- Earnest money budget, often 1%–3% of the purchase price in many markets

- Preferred closing date and move-in flexibility

- Inspection, appraisal, financing, and title contingency decisions

- Real estate agent contact information and state-required disclosure forms

This preparation matters because an offer is a legal and financial move, not a casual message. Buyers who are still checking whether they are financially ready can compare this step with Baltimore Chronicle’s guide on how to get pre-approved for a mortgage in USA in 2026. It explains which documents lenders usually request before a buyer can submit a serious offer.

Do not rely on a lender’s rough text message or an old preapproval from 3 months ago. Sellers may ask for proof that your approval reflects current income, credit, and rates. A buyer who has documents ready can move faster when a good listing appears.

Step 1: Check the true market value before choosing your offer price

Start with comparable sales, not the listing price. Ask your agent for homes sold in the last 3–6 months within the same school zone, property type, bedroom count, square footage range, and condition level.

This matters because a $495,000 listing can be underpriced to start a bidding war, fairly priced, or overpriced by $40,000. Zillow, Redfin, Realtor.com, and MLS data can help, but recent closed sales carry more weight than active listings.

The common mistake is anchoring to the seller’s asking price. Your offer should reflect real market value, repair risk, and competition, not the seller’s hope.

Step 2: Decide your walk-away number before negotiations begin

Set your maximum offer before the seller responds. Include mortgage payment, taxes, homeowners insurance, HOA dues, utilities, maintenance, and any planned repairs.

This matters because buyers often stretch after losing 1 or 2 homes. In high-demand areas of California, New Jersey, Massachusetts, and parts of Texas, emotional bidding can turn a good house into a risky purchase.

The mistake to avoid is saying, “We can figure it out later.” If your payment depends on perfect rates, perfect insurance, and no repairs, the offer is already too fragile.

Step 3: Choose contingencies that protect you without weakening the offer

A contingency gives you a legal exit if a defined problem appears. The most common are inspection, financing, appraisal, title, sale-of-current-home, and HOA document review.

This matters because contingencies decide whether you can recover your earnest money if the deal fails for a valid reason. Once the seller accepts the contract, the deal usually moves into escrow. Baltimore Chronicle’s explainer on what escrow means when buying a house is useful for understanding where the deposit goes and why deadlines matter.

The mistake is removing protections just to win. Waiving inspection on an older house with a 20-year roof, aluminum wiring, basement moisture, or an aging HVAC system can create a repair bill larger than your down payment.

| Offer element | Buyer protection | Seller reaction | 2026 strategy |

|---|---|---|---|

| Inspection contingency | Protects against major defects | Can slow the deal | Use a short inspection window, often 5–7 days |

| Financing contingency | Protects if loan approval fails | Standard for financed buyers | Attach strong preapproval from Chase, Wells Fargo, Rocket Mortgage, or a local lender |

| Appraisal contingency | Protects if appraisal is low | Weaker in bidding wars | Consider a limited appraisal gap only if cash reserves allow |

| Home sale contingency | Protects buyers who must sell first | Often unattractive | Use only when necessary, or offer a stronger price and flexible closing |

The right mix depends on the house and the market. A 1998 townhouse in Phoenix may need a different approach than a 1920 rowhouse in Baltimore or a newer suburban home outside Raleigh. Older properties deserve more inspection protection because hidden repairs are more common.

Cash reserves also matter. If you offer an appraisal gap, you may need to bring extra cash if the lender’s appraisal comes in below contract price. That can be useful, but only when the amount is capped and affordable.

Never copy another buyer’s strategy without checking your own risk. A buyer with $150,000 in reserves can absorb problems that a buyer with $14,000 cannot. Winning the contract is not the same as closing safely.

Step 4: Write the offer letter carefully, or skip it when risk is high

A buyer letter can humanize your offer, but it should be short, property-focused, and careful. Mention what you appreciate about the home, such as the garden, natural light, workshop, kitchen layout, or proximity to work.

This matters because some sellers care about continuity. A family selling a long-owned home in Pennsylvania or Virginia may respond to a respectful note more than an investor-style offer.

The common mistake is including personal details that could create fair housing concerns. Avoid references to religion, family status, nationality, disability, or protected characteristics. Keep the letter about the house, not your identity.

Simple buyer letter structure

- Thank the seller for showing the property.

- Name 2 specific features you value.

- State that your offer is serious and financially prepared.

- Keep the tone respectful, not desperate.

- Let your agent handle price, dates, and contract terms separately.

A letter should never repair a weak offer. If your price is low, your financing is uncertain, and your closing date is inconvenient, kind words will not solve the seller’s problem. In competitive markets, clean terms usually speak louder than sentiment.

Some brokerages discourage buyer letters because they can create compliance risk. If your agent advises against one, listen. A concise, professional offer summary can often do the same job without personal details.

Step 5: Set earnest money and deadlines that show commitment

Earnest money is the deposit that signals you intend to close. In many US markets, buyers commonly offer 1%–3% of the purchase price, though local customs vary by state and price range.

This matters because a $7,500 deposit on a $500,000 home may look more serious than $1,000, especially when the seller has multiple offers. The funds are usually held by an escrow company, title company, broker, or attorney, depending on the state.

Cash planning should include more than the down payment. Baltimore Chronicle’s breakdown of closing costs on a house in USA in 2026 shows why lender fees, title fees, insurance, taxes, and prepaid costs can change the real amount needed before closing.

The mistake is offering money you cannot afford to risk. If you miss deadlines or cancel outside contract protections, your deposit may be disputed.

Step 6: Use timing as a negotiation tool

Price is only 1 lever. Closing date, rent-back, inspection period, appraisal terms, and seller-paid repairs can decide the winner.

This matters because sellers often have their own problem to solve. They may need 30 days to buy another home, 45 days to relocate, or a 2-week rent-back after closing.

The mistake is assuming every seller wants the fastest close. A flexible buyer with conventional financing may beat a higher offer if the higher buyer creates timing pressure.

Step 7: Send a complete written offer through your agent

Your agent should submit the purchase agreement, preapproval letter, proof of funds when needed, contingency terms, offer deadline, proposed closing date, and any addenda required by state law. In attorney states such as New York and New Jersey, legal review may also shape the process.

This matters because incomplete offers look careless. Listing agents remember buyers who create extra work before the deal even starts.

For readers who are earlier in the process, Baltimore Chronicle’s full guide on how to buy a house in USA in 2026 gives the broader timeline from budgeting and touring to inspection, appraisal, and closing.

The mistake is texting numbers without documents. A verbal offer may start a conversation, but the seller needs written terms before making a decision.

Step 8: Negotiate without losing your protections

If the seller counters, compare every change against your budget and risk limits. A counteroffer may change price, closing date, repairs, appliances, earnest money, or contingency deadlines.

This matters because small wording changes can shift thousands of dollars in risk. For example, accepting a broad “as-is” clause may limit repair leverage after inspection.

The mistake is focusing only on the monthly payment. You should also check cash due at closing, inspection rights, appraisal exposure, and post-closing repair costs.

Troubleshooting: what to do when the offer gets difficult

Real estate deals rarely move in a straight line. Use the problem in front of you to decide whether to improve the offer, hold firm, or walk away.

- Your offer is below asking: Explain the number with comps, repair estimates, and realistic closing terms.

- There are multiple offers: Shorten deadlines, increase earnest money, or add limited flexibility before raising price.

- The appraisal may come in low: Offer a capped appraisal gap only if you have verified cash reserves.

- The inspection finds major defects: Ask for credits, price reduction, repairs, or cancellation under your contingency.

- The seller wants a rent-back: Require written dates, insurance clarity, deposit terms, and local legal review.

These scenarios are common in 2026 because affordability remains tight in many metro areas. Buyers are trying to control monthly payments while sellers still remember higher pandemic-era prices. That tension makes negotiation more technical.

A good agent will separate emotion from leverage. The question is not whether the house feels perfect. The question is whether the contract still works after price, repairs, loan terms, and timing are counted together.

If the seller pressures you to waive everything, slow down. Strong buyers are not reckless buyers. A house that requires unsafe terms may not be the right house.

FAQ

How much should I offer below asking price on a house?

There is no national rule. In a slow market, 3%–7% below asking may be reasonable. In a hot market, even full price may lose. Use local sold comps, days on market, repairs, and competing offers.

Can I make an offer on a house without a real estate agent?

Yes, but it is risky if you do not understand contracts, deadlines, disclosures, escrow, title, and state rules. Many buyers use an agent because the paperwork creates legal and financial consequences.

Should I waive the home inspection to win?

Usually no. A safer option is a shorter inspection period or an informational inspection. Waiving inspection can expose you to roof, foundation, electrical, plumbing, mold, or HVAC problems.

What is a good earnest money amount in 2026?

Many buyers use 1%–3% of the purchase price, but local practice matters. Ask your agent what is normal in your county and price range before sending the offer.

Does a personal letter to the seller still help?

Sometimes, but it is not the main factor. Keep it short and property-focused. Avoid personal details that could raise fair housing concerns.

What happens after my offer is accepted?

You enter escrow or attorney review, depending on the state. Then come inspections, appraisal, loan underwriting, title work, homeowners insurance, final walk-through, and closing.

Earlier we wrote about How Long Does USPS First Class Take in 2026? Delivery Times by Zone Explained