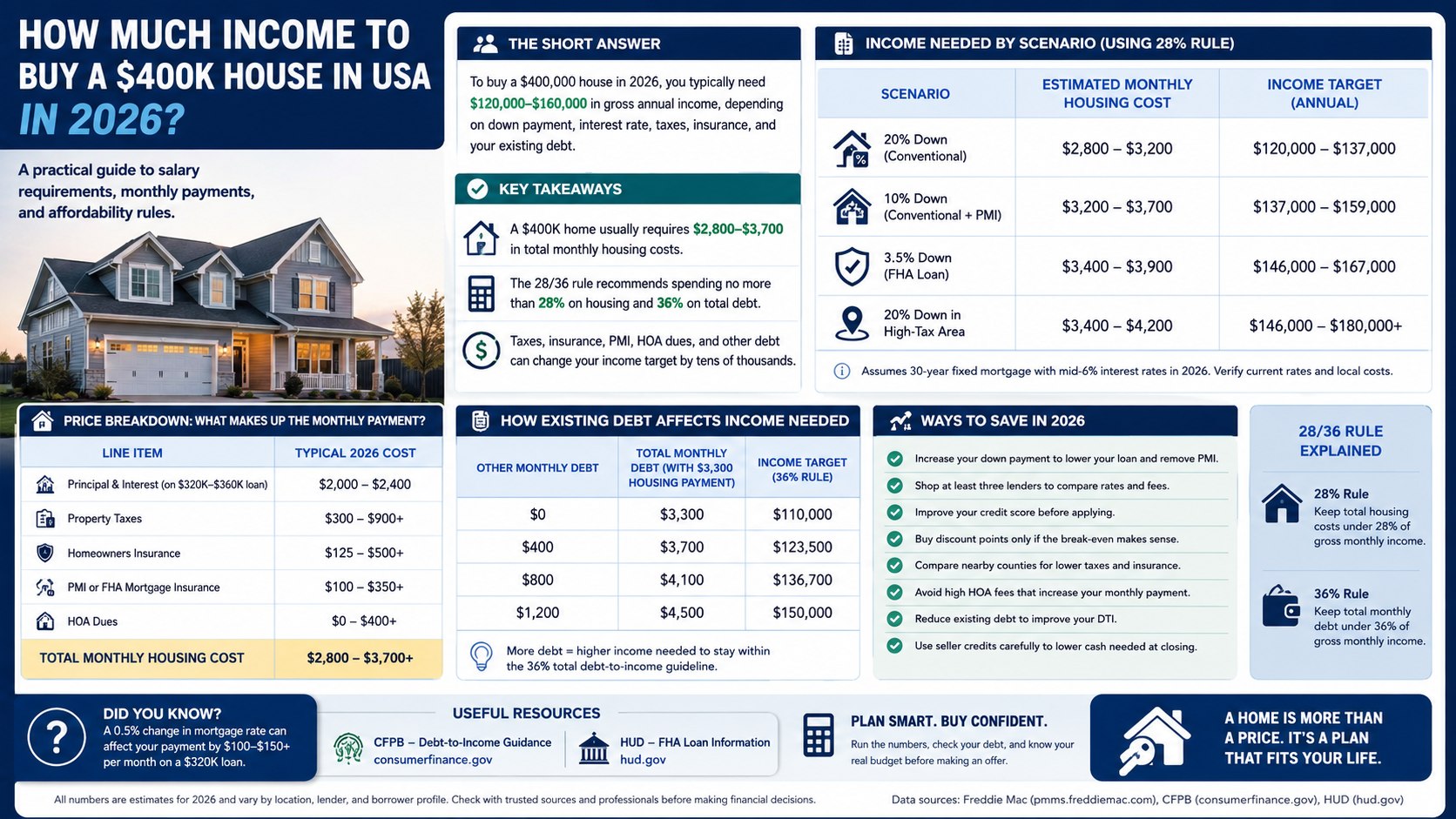

A $400,000 home in 2026 typically requires about $120,000 to $160,000 in gross annual household income for many US buyers. The low end can be near $95,000 with a large down payment, low property taxes, and no debt. The high end can pass $190,000 with a small down payment, expensive insurance, high taxes, HOA dues, or car and credit card payments, аs noted by Baltimore Chronicle.

The simplest answer to how much income to buy a 400k house in USA is this: using the 28/36 rule, a buyer should usually keep the full housing payment near $2,800 to $3,700 per month. That points to roughly $120,000 to $160,000 a year before taxes for a conventional 30-year mortgage, depending on down payment, interest rate, debt, and state-level costs.

Key takeaways

- A $400,000 home usually needs about $120,000 to $160,000 in gross annual income under common lender affordability rules.

- The 28/36 rule limits housing costs to 28% of gross income and total debts to 36%.

- Taxes, insurance, PMI, HOA dues, and existing debt can change the salary target by tens of thousands.

How much income to buy a 400k house in USA under the 28/36 rule

The 28/36 rule is a budgeting guideline many buyers use before applying for a mortgage. It says housing costs should stay under 28% of gross monthly income, while total monthly debt should stay under 36%.

Housing costs include principal, interest, property taxes, homeowners insurance, mortgage insurance, and HOA dues. Total debt adds car loans, student loans, credit cards, personal loans, and other recurring obligations.

For a $400,000 home, a typical 2026 payment can land between $2,800 and $3,700 per month. At 28% of gross income, that means an annual salary of about $120,000 to $159,000.

The Consumer Financial Protection Bureau defines debt-to-income ratio as monthly debt payments divided by gross monthly income. Different loan products and lenders use varying DTI limits, so the 28/36 rule is a planning tool rather than a universal approval rule. CFPB debt-to-income guidance explains the calculation.

For more insights on managing household debt before buying a home, Baltimore Chronicle covers strategies to reduce debt for homebuyers in 2026.

Quick salary estimates for a $400,000 home

The salary needed for a $400k mortgage depends heavily on the loan amount. A buyer who puts 20% down borrows $320,000. A buyer who puts 10% down borrows $360,000. An FHA buyer with 3.5% down borrows about $386,000 before upfront FHA mortgage insurance.

| Scenario | Estimated 2026 monthly housing cost | Income target using 28% rule |

|---|---|---|

| 20% down, conventional loan | $2,800–$3,200 | $120,000–$137,000 |

| 10% down, conventional loan with PMI | $3,200–$3,700 | $137,000–$159,000 |

| 3.5% down, FHA loan | $3,400–$3,900 | $146,000–$167,000 |

| 20% down, high-tax or high-insurance area | $3,400–$4,200 | $146,000–$180,000 |

These ranges assume a 30-year fixed mortgage rate around mid-6% in 2026. Borrowers should verify live rates before making an offer because even a 0.5 percentage point change can shift the monthly payment meaningfully. Freddie Mac mortgage rate data updates weekly.

For local market comparisons, Baltimore Chronicle also explains state-by-state home affordability in 2026, including Maryland, Texas, and Florida.

What drives the price

Mortgage rate

The interest rate is usually the biggest moving part after the home price. On a $320,000 loan, a rate in the low-6% range can create a very different payment from a rate near 7%.

Credit score, loan type, points, lender margin, and market conditions all affect the rate quote. Bank of America, Chase, Rocket Mortgage, Wells Fargo, Navy Federal Credit Union, and local credit unions may quote different rates for the same buyer on the same day.

Down payment

A larger down payment reduces the loan balance and can remove private mortgage insurance on many conventional loans. On a $400,000 purchase, 20% down equals $80,000 before closing costs.

A smaller down payment makes the home accessible sooner, but the monthly payment rises. The buyer may also carry PMI or FHA mortgage insurance, which changes the income needed.

Property taxes by state and county

Property taxes vary sharply across the USA. A $400,000 house in New Jersey, Texas, Illinois, or parts of New York can carry a much higher tax bill than a similarly priced home in states with lower effective property tax burdens.

County-level taxes matter more than national averages. Two homes with the same sale price can have different monthly payments because of school district taxes, municipal taxes, special assessments, and exemptions.

Homeowners insurance

Insurance is a major 2026 affordability factor, especially in Florida, Louisiana, Texas, California, and wildfire- or hurricane-exposed areas. Premiums can be modest in some inland markets and much higher near coastal or disaster-prone areas.

Lenders include insurance in the escrow payment when calculating affordability. Buyers comparing Phoenix, Tampa, Dallas, Baltimore, Denver, and Atlanta should treat insurance quotes as part of the mortgage math.

Mortgage insurance

Private mortgage insurance often applies when a conventional borrower puts less than 20% down. FHA loans use mortgage insurance premiums under HUD rules, with a minimum 3.5% down payment for eligible borrowers.

HUD publishes official FHA loan limits and program updates through the Federal Housing Administration. Buyers should check current HUD rules before assuming a $400,000 home fits the program. HUD FHA information

Existing monthly debt

A buyer with no car payment and no credit card balance can qualify on less income than a buyer with $900 per month in existing debt. The 36% side of the 28/36 rule is where debt becomes the blocker.

For example, a $3,300 housing payment plus $900 in monthly debt equals $4,200 total obligations. At 36% DTI, that requires about $140,000 in gross annual income before considering lender overlays or reserves.

Price breakdown

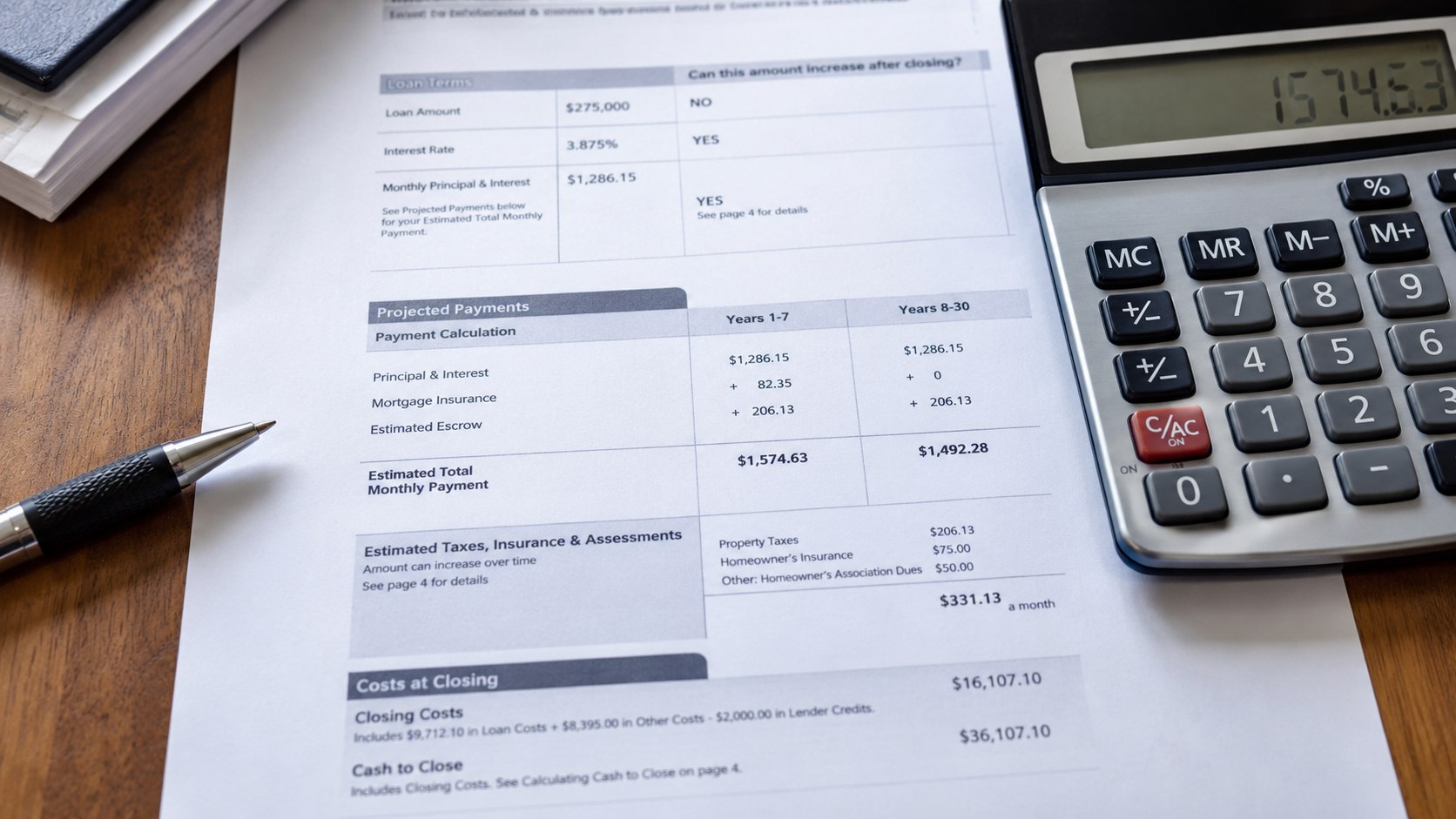

A $400,000 purchase price is not the same as a $400,000 mortgage. The real monthly cost includes financing, taxes, insurance, and sometimes association or mortgage insurance charges.

| Line item | Typical 2026 cost |

|---|---|

| Down payment, 20% conventional | $80,000 |

| Down payment, 10% conventional | $40,000 |

| Down payment, 3.5% FHA | $14,000 |

| Principal and interest, $320,000 loan at mid-6% | $2,000–$2,100/mo |

| Principal and interest, $360,000 loan at mid-6% | $2,250–$2,400/mo |

| Property taxes | $300–$900+/mo |

| Homeowners insurance | $125–$500+/mo |

| PMI or FHA mortgage insurance | $100–$350+/mo |

| HOA dues | $0–$400+/mo |

| Closing costs | $8,000–$20,000 |

The monthly payment is what affects approval. Cash-to-close affects whether the buyer can complete the purchase without draining emergency savings. Baltimore Chronicle’s guide to closing costs for first-time homebuyers separates lender fees, title fees, prepaid taxes, escrow deposits, and discount points.

How existing debt changes the salary needed

The same $400,000 house can be affordable for one household and out of reach for another with the same salary. Debt payments explain much of the difference.

Assume a buyer has a $3,300 monthly housing payment. Under the 28% rule, the housing payment alone points to about $141,500 gross annual income.

Add other debts. Under the 36% rule, the lender compares all monthly debt to gross income.

| Other monthly debt | Total monthly debt with $3,300 housing | Income target using 36% rule |

|---|---|---|

| $0 | $3,300 | $110,000 |

| $400 | $3,700 | $123,500 |

| $800 | $4,100 | $136,700 |

| $1,200 | $4,500 | $150,000 |

A buyer with $1,200 in other monthly debt may need closer to $150,000 even if the house payment itself looks manageable.

The practical test is not the listing price. The practical test is whether the full monthly housing payment fits beside car loans, childcare, insurance, groceries, retirement savings, and emergency cash.

Ways to save in 2026

- Increase the down payment. Moving from 10% to 20% down can reduce the loan balance and may remove PMI.

- Shop at least three lenders. Compare a national bank, mortgage broker, and credit union before locking a rate.

- Improve credit before applying. Paying down revolving balances can improve credit utilization and loan pricing.

- Buy points only when break-even math works. Discount points can lower the rate if the buyer plans to keep the loan long enough.

- Compare nearby counties. Property taxes and insurance can change even when commute time is similar.

- Avoid HOA surprises. A $250 monthly HOA fee adds as much to the budget as a higher mortgage payment.

- Reduce debt before preapproval. Paying off a car loan or credit card can improve DTI more than saving a small additional down payment.

- Use seller credits carefully. Credits reduce cash needed at closing but may not reduce monthly payment.

Baltimore Chronicle also explains conventional vs FHA loans in 2026 to help buyers compare upfront costs and monthly payments.

When paying more makes sense

The home lowers other monthly costs

Paying more can make sense when the location cuts commuting costs, childcare, or parking. A higher mortgage near work may be cheaper than a cheaper house 40 miles away.

The property is move-in ready

A cheaper home needing roof, HVAC, electrical, or plumbing repairs can cost more in the first two years than a cleaner $400,000 home.

The school district replaces private tuition

Parents sometimes accept higher payments to access a public school district that reduces or eliminates private school tuition.

The buyer plans to stay long enough

Closing costs, moving, furnishing, repairs, and early interest-heavy mortgage payments make short-term ownership expensive.

Checklist before making an offer on a $400,000 house

- Confirm the full monthly payment with taxes, insurance, PMI, and HOA dues included.

- Check whether the payment stays near 28% of gross monthly income.

- Add all recurring debt and compare total with 36% DTI guideline.

- Get written loan estimates from at least three lenders.

- Request local insurance quotes before the inspection period ends.

- Review property tax history and reassessment possibilities.

- Keep emergency savings separate from down payment and closing costs.

- Budget for repairs, furniture, utilities, moving costs, and maintenance after closing.

FAQ

Can I buy a $400,000 house with a $100,000 salary?

It may be possible but tight. $100,000 gives about $2,333 per month under the 28% housing rule, often below full payment unless down payment is large, taxes low, and debt minimal.

What salary do I need for a 400k mortgage?

A $400,000 mortgage may require roughly $150,000–$180,000+ gross annual income in 2026 when taxes, insurance, and mortgage insurance are included.

How much should I make to afford a 400k home with 20% down?

With 20% down ($320,000 loan), a realistic income is $120,000–$140,000 assuming mid-6% rates, moderate property taxes, normal insurance, and limited debt.

Does the 28/36 rule guarantee mortgage approval?

No. It is a planning benchmark. Lenders also review credit score, employment history, assets, reserves, loan type, property condition, and appraisal.

Is a $400,000 house affordable for first-time buyers?

It can be with stable income, manageable debt, and enough cash for down payment, closing costs, and reserves. Monthly payment may rise in high-tax or high-insurance states.

How can I lower the income required to buy a $400,000 home?

Increase down payment, improve credit, compare lenders, reduce debt, choose a lower-tax location, and avoid unnecessary HOA costs. Compare full payments, not only sale price.

Earlier we wrote about IKEA Furniture Assembly Tips 2026: Tools, Steps, and Mistakes to Avoid