This list was built around programs that are available nationally or through state housing finance agencies, with priority given to official HUD, FHA, VA, USDA, and state-linked assistance. Each option was chosen for a real 2026 buyer problem: low cash savings, military eligibility, rural location, higher prices, credit limits, or the need to combine a mortgage with down payment help, аs noted by Baltimore Chronicle.

First time home buyer programs 2026 usa are not one program. They are a stack of mortgage products, grants, forgivable loans, tax credits, and local assistance rules that can lower the cash needed to close on a first home.

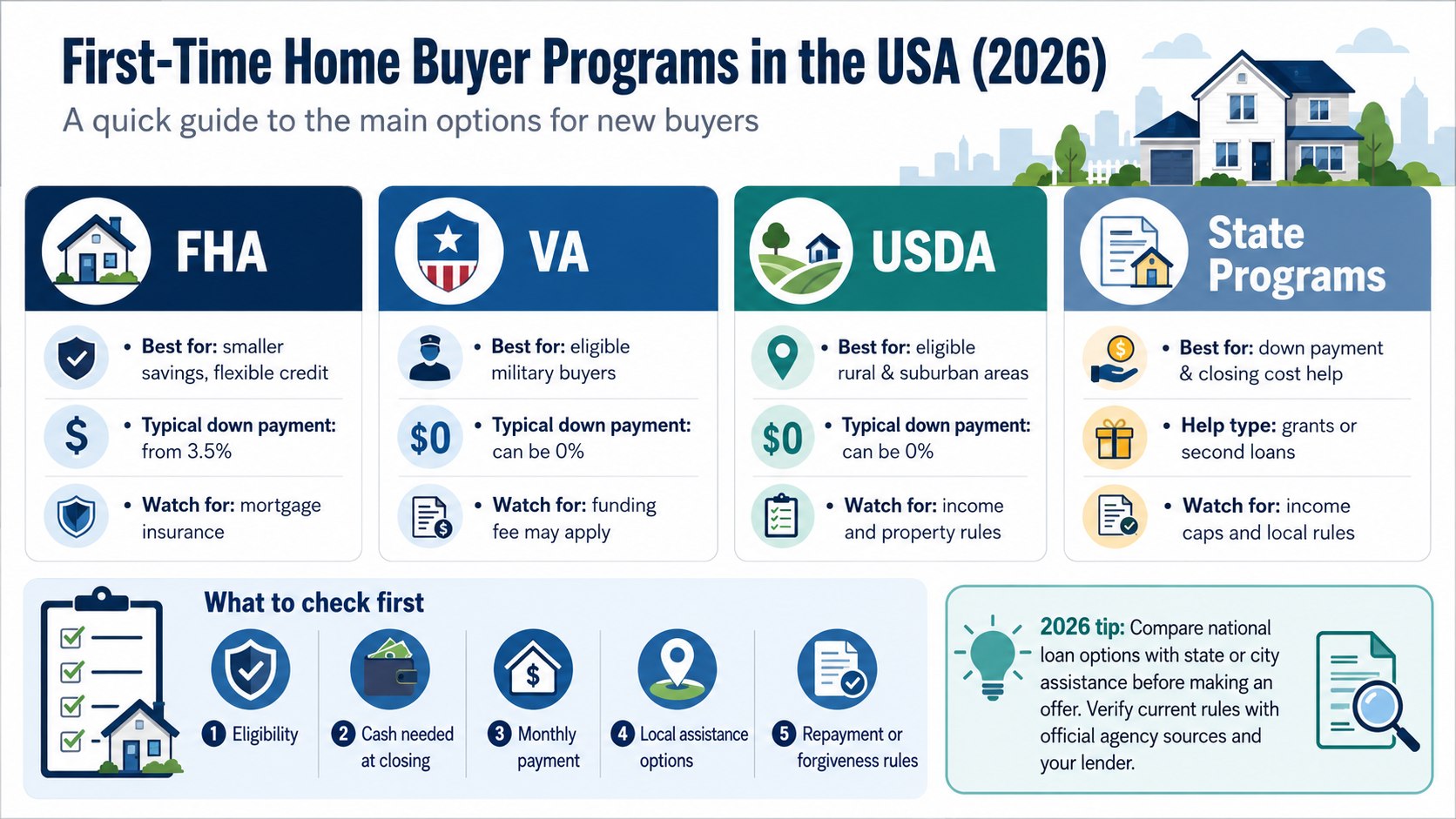

Key takeaways

- FHA is often the most flexible national option when credit score, debt ratio, or savings are the main barriers.

- VA and USDA can offer zero-down paths, but eligibility depends on service history, location, income, and property type.

- State programs can be the difference-maker in 2026 because they may cover down payment and closing cost gaps.

How to use first time home buyer programs 2026 usa without wasting months

The fastest path is to start with eligibility, not listings. A buyer should first check whether they qualify for VA, USDA, FHA, or state housing finance agency assistance before comparing homes on Zillow, Redfin, Realtor.com, or local MLS feeds.

In 2026, the practical order is simple. Confirm mortgage type, estimate cash needed at closing, then ask whether the state or city can cover part of that cash through a grant, second mortgage, or forgivable loan. Buyers who are still mapping the full purchase process can use Baltimore Chronicle’s guide on how to buy a house in USA 2026 before choosing a loan program.

The cash question should come early. Baltimore Chronicle’s breakdown of how much down payment for a house in USA 2026 is useful because the right program depends on whether the buyer is short by $5,000, $15,000, or the full down payment.

| Program type | Best fit in 2026 | Main catch |

|---|---|---|

| FHA loan | Buyers with limited cash or imperfect credit | Mortgage insurance usually applies |

| VA loan | Eligible veterans, service members, and some surviving spouses | Funding fee may apply unless exempt |

| USDA loan | Moderate-income buyers outside dense urban areas | Home and household income must qualify |

| State assistance | Buyers who need down payment or closing cost help | Funds, income caps, and rules vary by state |

1. FHA loans for buyers with smaller savings

FHA loans remain one of the most useful first-time homebuyer assistance programs because they are designed for borrowers who may not qualify cleanly for a conventional loan. The Federal Housing Administration insures the loan, while banks, credit unions, and mortgage lenders originate it.

The concrete fact that matters in 2026 is the low down payment structure. Many FHA borrowers can put down 3.5% if they meet the required credit standard, though actual approval still depends on income, debt, assets, and the lender’s underwriting.

FHA stands out because it works in expensive and moderate-price markets. A buyer in Ohio looking at a $245,000 starter home and a buyer in California looking at a much higher-priced condo may both use FHA, but loan limits vary by county and should be checked through HUD’s official FHA mortgage limits tool.

The tradeoff is mortgage insurance. FHA borrowers usually pay upfront and annual mortgage insurance, so the monthly payment can be higher than a conventional loan with a strong credit profile and larger down payment.

2. VA loans for eligible military buyers

VA loans are often the strongest national option for eligible veterans, active-duty service members, National Guard members, reservists, and certain surviving spouses. The Department of Veterans Affairs does not usually lend the money directly; it guarantees part of the loan made by an approved lender.

The concrete fact is the zero-down structure. Many eligible buyers can buy with no down payment, and VA loans do not require monthly private mortgage insurance.

VA loans stand out in 2026 because high rents have made it harder for military families to save a large lump sum. In markets such as Texas, Florida, Virginia, North Carolina, and Arizona, the absence of a required down payment can keep ownership possible when cash savings are the bottleneck.

The buyer still needs to budget for closing costs, inspections, prepaid taxes, homeowners insurance, and the VA funding fee unless exempt. The official VA funding fee page explains how the fee changes based on down payment, first or later use, and exemption status.

3. USDA loans for rural and suburban buyers

USDA loans are not only for farms. The USDA Single Family Housing programs can apply in many small towns, outer suburbs, and rural communities where a buyer may still commute to a regional job center.

The concrete fact is that USDA’s guaranteed loan program may allow 100% financing for eligible buyers and eligible properties. Income limits and property eligibility are central, so a household must check both before assuming the program works.

USDA stands out in 2026 because starter homes are often cheaper outside major metros, but cash savings remain tight for renters. A buyer priced out of central Nashville, Denver, or Charlotte may find that a nearby eligible county changes the math.

USDA can be less useful for buyers who need to purchase in a dense urban neighborhood or who earn above the program’s income limits. The official USDA eligibility tools are the right starting point because boundaries and income limits are location-specific.

4. State housing finance agency programs

Every serious 2026 buyer should check their state housing finance agency before choosing a lender. These agencies often provide down payment assistance 2026, closing cost help, tax credits, below-market mortgage options, or second loans paired with FHA, VA, USDA, or conventional financing.

The concrete fact is that many state programs are not direct grants. They may be deferred loans, forgivable second mortgages, repayable second mortgages, or assistance that must be paid back when the home is sold, refinanced, or no longer used as a primary residence.

State programs stand out because they target local price pressure. California, New York, Maryland, Pennsylvania, Illinois, Georgia, and Texas have different income limits and benefit structures because a “starter home” price is not the same across those markets.

For Maryland buyers, the local layer can matter as much as the national loan type. Baltimore Chronicle’s guide to first-time homebuyer options in Baltimore gives neighborhood-level context for buyers comparing grants, commute patterns, and starter-home areas.

5. Conventional 97 and HomeReady-style loans

Conventional low-down-payment loans can work for buyers who have stronger credit but limited cash. Programs commonly associated with Fannie Mae and Freddie Mac may allow down payments around 3% for eligible first-time or moderate-income buyers.

The concrete fact is that conventional loans usually rely on private mortgage insurance when the buyer puts less than 20% down. That insurance may be cancellable later if equity grows and the loan meets cancellation rules.

This route stands out in 2026 for buyers who have solid credit, stable income, and want an alternative to FHA mortgage insurance. It may be attractive for a buyer purchasing a $325,000 townhouse in Pennsylvania or a $410,000 condo in Illinois with enough income to qualify but not enough savings for 10% down.

The drawback is that conventional underwriting can be less forgiving than FHA. A thin credit file, high debt-to-income ratio, or recent self-employment income may make FHA or a state-backed product more realistic.

6. Good Neighbor Next Door for public-service buyers

HUD’s Good Neighbor Next Door program is a niche option for eligible teachers, law enforcement officers, firefighters, and emergency medical technicians. It is tied to specific HUD-owned homes in designated revitalization areas, so availability is limited.

The concrete fact is that the program can offer a major discount on eligible homes, but the buyer must meet occupation and occupancy requirements. It is not a broad open-market benefit that can be applied to any property on Redfin or Realtor.com.

It stands out in 2026 because public-service workers are often priced out of the communities they serve. When an eligible home is available, the discount can matter more than a small rate difference.

The limitation is inventory. Buyers should treat it as a targeted opportunity, not the main plan for buying within a fixed 30- or 60-day timeline.

7. Housing Choice Voucher homeownership option

Some public housing agencies allow eligible Housing Choice Voucher participants to use voucher assistance toward homeownership expenses instead of rent. This is not available everywhere, and local public housing agency rules control the details.

The concrete fact is that the buyer usually must be a first-time homeowner under the program definition and meet employment, income, counseling, and local agency requirements. The home must also pass required inspections and affordability checks.

This option stands out in 2026 because it can convert rental support into a path toward ownership for households that already participate in the voucher system. It may help with monthly housing costs, but it does not remove the need for mortgage approval.

The key context is timing. A buyer should contact the local public housing agency before shopping, because not every agency operates a homeownership option.

8. Native American, Alaska Native, and tribal housing programs

Some buyers may qualify for federal or tribal housing options that are separate from mainstream FHA, VA, or USDA routes. HUD’s Section 184 Indian Home Loan Guarantee Program is one example for eligible Native American and Alaska Native borrowers and properties.

The concrete fact is that eligibility depends on borrower status, property location, and program rules. Buyers should check tribal housing departments and HUD-approved lenders that actually originate these loans.

This category stands out in 2026 because access to mortgage credit can be uneven in tribal communities and rural areas. A specialized loan program may offer a better fit than a generic conventional product.

The important context is lender experience. A lender that rarely handles tribal housing programs may slow the process or miss documentation requirements.

9. Local grants from cities and counties

City and county programs can be smaller than state programs but more targeted. They may help buyers purchase within city limits, near transit corridors, in redevelopment areas, or in neighborhoods where local officials want more owner-occupants.

The concrete fact is that local assistance often has narrow rules. A program may require a homebuyer education class, a maximum purchase price, a local residency period, or a minimum buyer contribution such as $1,000 from personal funds.

Local grants stand out in 2026 because even $5,000 to $15,000 can solve a closing-cost gap for a buyer who already qualifies for the monthly payment. In Baltimore, Philadelphia, Atlanta, Detroit, Cleveland, and Milwaukee, city-level help may stack with state programs when rules allow.

The risk is funding availability. Some programs open and close as annual budgets are used, so buyers should verify current status before relying on the money in an offer.

10. Employer and profession-based homebuyer help

Some hospitals, universities, school districts, police departments, and large employers offer housing help to recruit and retain workers. These benefits may come as grants, forgivable loans, closing cost credits, or neighborhood-specific incentives.

The concrete fact is that employer assistance is usually tied to continued employment or a required occupancy period. Leaving the job or selling too soon may trigger repayment.

This option stands out in 2026 because large employers in high-cost areas increasingly compete on practical benefits, not only salary. A nurse in Massachusetts, a teacher in Maryland, or a university employee in California may find that an employer benefit fills the last cash gap.

The context is coordination. The buyer should disclose employer assistance early to the lender, because funds must be documented and approved for underwriting.

2026 checklist before choosing a first-time buyer program

- Check VA eligibility first if the buyer has military service, because zero-down financing may change the entire budget.

- Check USDA property and income eligibility before ruling out homes outside major metro centers.

- Compare FHA and conventional payments with mortgage insurance included, not just the down payment.

- Search the state housing finance agency website for 2026 income limits, purchase price caps, and approved lenders.

- Ask whether state or local aid can be combined with FHA, VA, USDA, or conventional financing.

- Confirm whether assistance is a grant, forgivable loan, deferred loan, or repayable second mortgage.

- Complete required homebuyer education before making an offer if the program requires it.

- Get a written lender estimate that includes taxes, insurance, HOA dues, mortgage insurance, and all closing costs.

Program comparison for 2026 buyers

| Buyer problem | Program to check first | Why it may work in 2026 |

|---|---|---|

| Low savings | FHA plus state assistance | Lower down payment and possible closing cost help |

| Military eligibility | VA loan | Potential zero down and no monthly PMI |

| Buying outside a major city | USDA guaranteed loan | Potential 100% financing in eligible areas |

| Strong credit, limited cash | Conventional 97-style loan | Low down payment with cancellable mortgage insurance potential |

| Public-service job | Good Neighbor Next Door or employer aid | Occupation-based benefits may reduce the upfront cost |

Honorable mentions

- Mortgage Credit Certificates, where available, can reduce federal tax liability for eligible buyers, but rules vary by state and program year.

- Community land trusts can lower the purchase price by separating land ownership from the home, often with resale restrictions.

- Bank portfolio programs from lenders such as Bank of America, Chase, Wells Fargo, and local credit unions may help in specific neighborhoods, but terms should be compared against public programs.

FAQ

What is the best first-time home buyer program in the USA for 2026?

The best program depends on eligibility. VA is often strongest for eligible military borrowers, USDA can be powerful in eligible rural and suburban areas, FHA is flexible for credit and down payment barriers, and state programs can reduce cash needed at closing.

Can first-time buyers combine FHA with down payment assistance?

Yes, many buyers can combine FHA with state or local assistance when the assistance program and lender allow it. The buyer must confirm the source of funds, repayment terms, income limits, and purchase price limits before making an offer.

Do first-time home buyer programs require perfect credit?

No. FHA and some state programs are designed for buyers who do not have perfect credit, but approval still depends on income, debt, payment history, assets, and lender overlays.

Are there national grants for first-time home buyers in 2026?

Most grant-style help is state, city, county, employer, or nonprofit-based rather than one universal national grant. National loan programs such as FHA, VA, and USDA can be paired with local assistance if program rules allow it.

Where should a buyer verify program rules?

Buyers should verify FHA and homebuying options through HUD’s official homebuying resources and USDA property or income eligibility through USDA’s official eligibility site. State housing finance agency websites are the next stop for local 2026 limits and approved lender lists.

Earlier we wrote about Best Refrigerator Brands 2026 USA Ranked by Reliability, Price and Repair Access