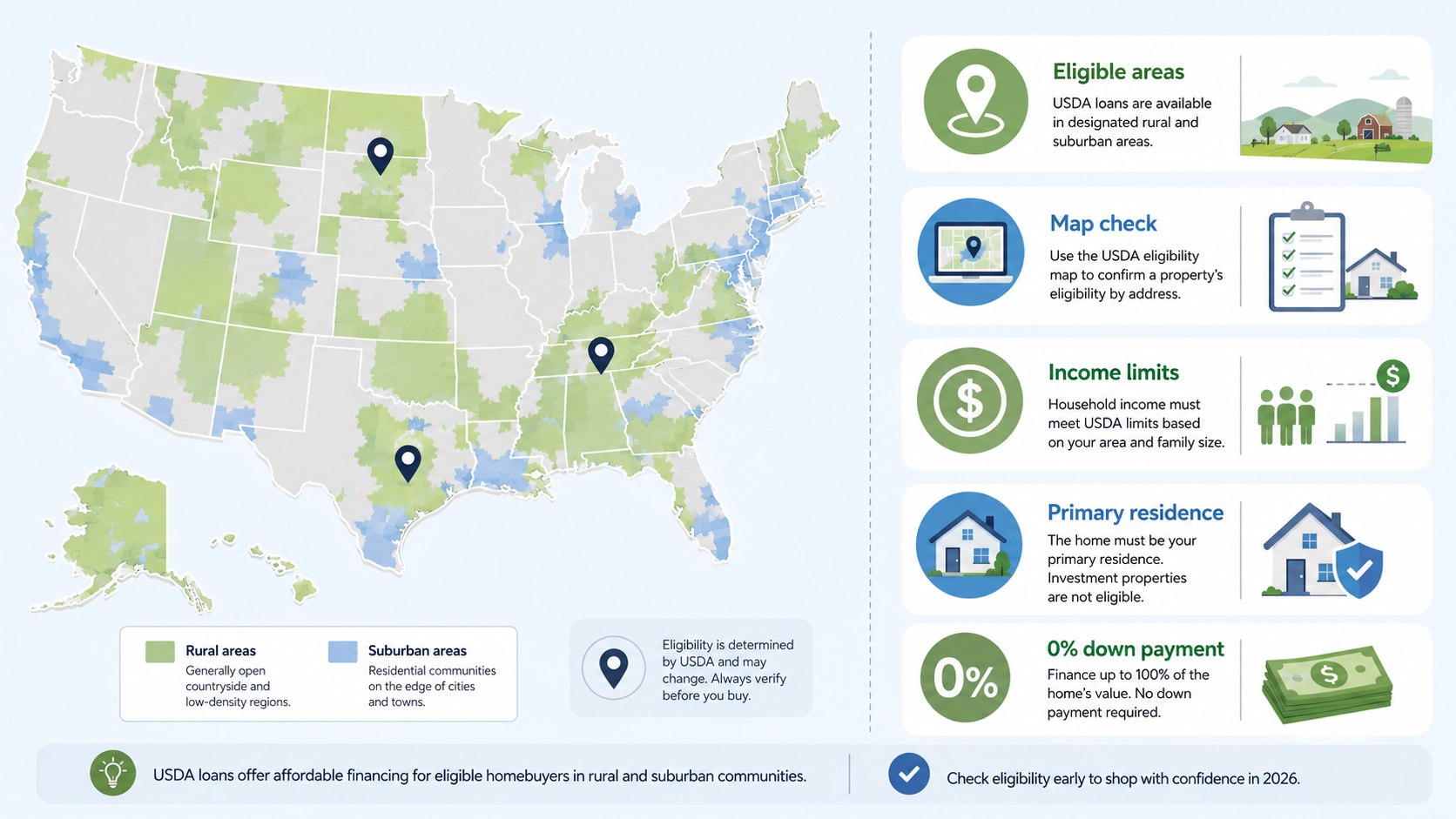

USDA loan eligible areas 2026 are locations where buyers may use USDA-backed financing for a qualifying primary residence. Check the exact street address on the official USDA map before touring, making an offer, or paying inspection fees. Then compare your total household income with the limit for that county and household size, as noted by Baltimore Chronicle.

A property can sit only a few blocks outside an excluded city boundary and still qualify. However, an eligible address does not guarantee loan approval. The borrower must also meet income, occupancy, credit, debt, appraisal, and lender requirements.

Key takeaways

- USDA eligibility is determined by the property’s exact address, not merely its county, ZIP code, or rural appearance.

- Guaranteed-loan household income generally cannot exceed 115% of the applicable median household income.

- The USDA map offers an initial screening result, while Rural Development makes the final property eligibility determination.

In plain English

Think of USDA eligibility as 2 locked doors. The first door tests the home’s location. The second tests the household’s finances.

A buyer must open both doors. A house may appear rural and still fall inside an excluded area. A household may also earn too much, even when the property qualifies.

The program is called “rural,” but eligible communities can include suburbs, small cities, county seats, and areas near major metropolitan markets.

The boundaries do not follow a simple national population rule visible to consumers. They are based on federal rural-area definitions and USDA determinations. That makes an address search more reliable than assumptions based on town size.

Buyers comparing mortgage choices can also review first-time homebuyer programs available in 2026. USDA financing is not limited to first-time buyers, but it often competes with FHA and conventional low-down-payment loans.

How USDA loan eligible areas 2026 actually work

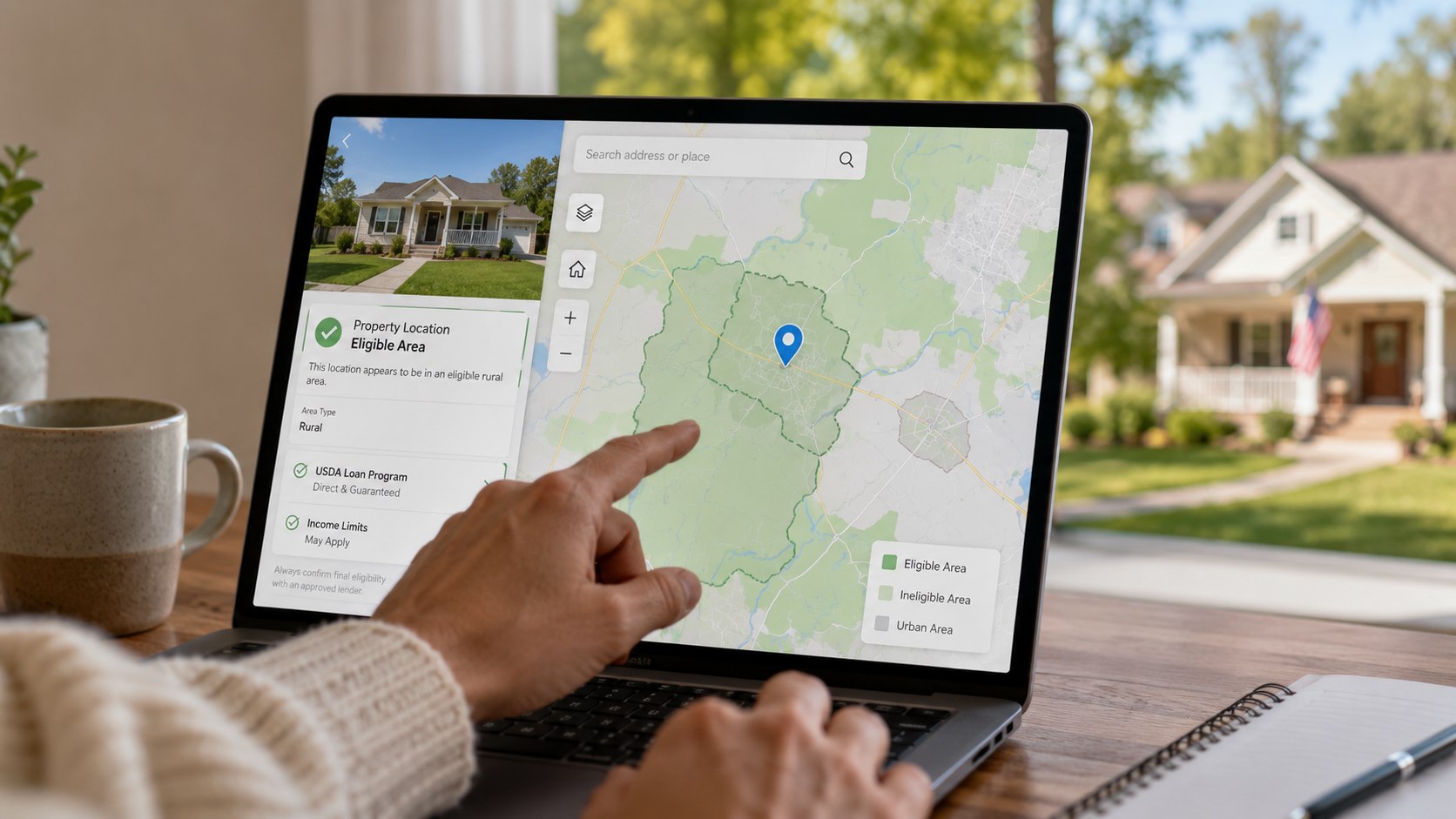

The official USDA property eligibility map lets buyers search a complete address. Enter the street number, street name, city, state, and ZIP code. The tool then places the property against current program boundaries.

An eligible result means the location passes the initial geographic test. It does not mean the house meets appraisal standards. It also does not confirm the borrower’s income or credit qualification.

When a property appears ineligible, zoom in carefully. Boundary lines can run through ZIP codes, subdivisions, roads, or growing communities. Search the exact address rather than relying on a real estate listing’s town name.

USDA warns that the online map is not a final agency decision. Rural Development determines final eligibility after receiving a complete application. Buyers should keep this condition in their purchase contract when location eligibility remains uncertain.

How to check an address before making an offer

Use the following process before spending money on an inspection, appraisal, survey, or attorney review:

- Open the official USDA Single Family Housing property eligibility map.

- Accept the property eligibility disclaimer shown by the agency.

- Enter the complete street address, city, state, and ZIP code.

- Zoom in and confirm the marker falls outside an ineligible shaded area.

- Save a screenshot or PDF showing the search result and date.

- Ask a USDA-approved lender to confirm the address before contract deadlines expire.

The saved result can help a lender identify map discrepancies. It also records what the public tool displayed when the buyer made the offer. Still, it does not override the agency’s final determination.

Check new-construction addresses with extra care. Recently assigned streets may not appear correctly in older address databases. A lender may need a parcel number, legal description, county record, or USDA review.

Do not search only by ZIP code. One ZIP code can include both eligible and ineligible properties. Two houses with the same mailing city may receive different results.

Buyers should also verify the address again before closing. Eligibility boundaries and agency records can change. A current lender review offers better protection than an old screenshot from a listing agent.

How income limits are checked

The USDA Guaranteed Loan Program generally limits household income to 115% of the applicable median household income. The exact dollar ceiling varies by location and household size. Limits can differ between counties within the same state.

USDA considers household income, which can be broader than the income used to qualify for the mortgage. Earnings from certain adult household members may count even when they are not loan applicants.

The agency may allow deductions when calculating adjusted household income. These can involve dependents, child care costs, disability-related expenses, and elderly household status. The lender must apply current USDA rules to the household’s documented circumstances.

| Income concept | What it generally measures | Why it matters |

|---|---|---|

| Annual household income | Qualifying income from relevant household members before allowed deductions | Establishes the starting point for program eligibility |

| Adjusted household income | Annual income after eligible USDA deductions | Compared with the local program income limit |

| Repayment income | Stable income used by the lender to evaluate mortgage repayment | Helps determine whether the borrower can afford the loan |

| Area income limit | USDA ceiling based on location and household size | Determines whether household income is within program rules |

These categories explain why an online mortgage calculator cannot confirm USDA approval. A household may pass the program income test but lack enough repayment income. Another household may afford the payment but exceed the local income ceiling.

Income from overtime, bonuses, commissions, self-employment, retirement, benefits, or a second job may require additional documentation. Lenders often review tax returns, pay stubs, bank statements, employment records, and benefit letters.

Household changes also matter. A working adult moving into the home can affect program income. A dependent leaving may alter both household size and available deductions.

Use USDA’s current income tool rather than a third-party chart. Published limits can be revised. The applicable amount depends on the property’s county and the number of household members.

Who it matters to in 2026

Buyers priced out of nearby cities

A renter searching around Atlanta, Dallas, Nashville, Raleigh, Phoenix, or another expanding metro may find eligible properties beyond excluded urban boundaries. The commute may increase, but the financing can reduce upfront cash requirements.

A $300,000 home with 3.5% down requires $10,500 before closing costs. A 5% down payment requires $15,000. A qualifying USDA loan may allow 100% financing, although closing costs and reserves can still require cash.

Moderate-income households with limited savings

USDA loans can suit buyers with stable income but little money saved for a down payment. The program does not eliminate affordability checks. Property taxes, homeowners insurance, association dues, debt, and the interest rate still affect approval.

Before choosing a loan, compare the full cash requirement. Baltimore Chronicle’s guide to down payments for a house in 2026 explains how USDA compares with FHA, VA, and conventional options.

Existing homeowners planning another purchase

USDA financing is not automatically restricted to first-time buyers. However, the new property must usually serve as the borrower’s primary residence. The lender must also examine any existing home ownership and occupancy circumstances.

A buyer should not assume that owning another property creates an automatic denial. The facts, occupancy plan, housing adequacy, and program guidance require lender review.

USDA loan costs and property conditions

A USDA guaranteed loan can offer 100% financing, but it is not free financing. The program generally includes an upfront guarantee fee and an annual fee. The annual charge is usually collected through the monthly mortgage payment.

USDA materials have commonly listed a 1% upfront guarantee fee and a 0.35% annual fee. Borrowers must verify the effective charges for their closing date. Program fees can change through official annual guidance.

The upfront fee may often be financed when the appraised value and loan structure permit it. Financing the fee reduces cash at closing but increases the loan balance and total interest paid.

The home must be a qualifying primary residence. It should be modest, safe, sanitary, and suitable for residential use. Existing homes, certain new homes, approved condominiums, and planned-unit properties may qualify when program requirements are met.

USDA financing is not intended for a vacation property or a property primarily designed to produce income. Large commercial features, extensive working farmland, or income-producing structures can create eligibility problems.

Documents to prepare before lender review

An early document review helps prevent delays after the buyer signs a contract. Requirements vary by lender, employment type, and household structure.

- Recent pay stubs covering the lender’s requested period

- W-2 forms and federal tax returns when required

- Bank, investment, and retirement account statements

- Identification and Social Security information

- Employment history and employer contact details

- Records for bonuses, overtime, commissions, or second jobs

- Self-employment profit-and-loss statements and business returns

- Benefit, pension, child support, or alimony documentation

- Names, ages, and income details for relevant household members

Provide complete statements, including blank pages. Large deposits may need a documented source. Moving money between accounts shortly before underwriting can create avoidable questions.

Self-employed applicants should prepare earlier. Lenders may analyze business income, noncash expenses, declining revenue, ownership percentage, and current-year performance. Taxable income alone may not equal qualifying income.

Do not hide income from an adult household member because that person is not applying. USDA program eligibility and mortgage underwriting use different income concepts. An omission can delay approval or create a compliance issue.

Keep digital copies in a secure folder. Updated pay stubs and bank statements may be requested before closing. Fast responses help protect financing deadlines in the purchase agreement.

Common myths

Several assumptions cause buyers to reject USDA financing too early or pursue homes that cannot qualify:

- Myth: Only farms qualify. Correction: USDA housing loans finance eligible primary residences, not only agricultural properties.

- Myth: Every small town qualifies. Correction: The exact address must fall within a current eligible boundary.

- Myth: USDA loans are only for first-time buyers. Correction: Qualified repeat buyers may also use the program.

- Myth: Zero down means zero cash. Correction: Buyers may still pay inspections, closing costs, prepaid expenses, and reserves.

- Myth: The map result guarantees approval. Correction: USDA makes the final determination after reviewing a complete application.

The “farm loan” myth is especially persistent because USDA administers agricultural programs. Rural Development’s housing programs serve residential buyers in eligible communities.

Zero-down financing also needs context. Sellers may contribute toward permitted costs, and some expenses may be financed. However, the available structure depends on the appraisal, contract, lender, and program limits.

Buyers should compare interest rates and total costs, not only the down payment. USDA, FHA, VA, and conventional loans use different fees and underwriting rules.

Closing expenses can materially change the budget. The Baltimore Chronicle guide to closing costs on a house separates lender charges, title costs, prepaid taxes, insurance, and escrow deposits.

FAQ about USDA loan eligible areas 2026

How do I know whether my house is in a USDA eligible area?

Search the complete address on the official USDA property eligibility map. Then ask a USDA-approved lender to verify the result. The online map provides preliminary guidance, while USDA makes the final determination.

Can part of a city qualify for a USDA loan?

Yes. Eligibility boundaries can divide cities, ZIP codes, roads, and subdivisions. A mailing address may use a city name even when the property lies outside the excluded urban boundary.

What is the USDA income limit for 2026?

There is no single national dollar limit. Guaranteed-loan income generally cannot exceed 115% of the applicable median household income. The actual ceiling depends on location and household size.

Does everyone living in the house count toward the income limit?

Income from relevant adult household members may count, even when they are not borrowers. USDA rules also provide certain deductions when calculating adjusted household income.

Can I use a USDA loan for an investment property?

No. USDA single-family housing financing is designed for an eligible primary residence. Vacation homes and properties primarily intended to generate income generally do not qualify.

Can a USDA map change after I make an offer?

Boundaries and records can change. Include a financing contingency and obtain lender confirmation early. Recheck the address before closing when eligibility is essential to the purchase.

USDA loan eligible areas 2026 are locations where buyers may use USDA-backed financing for a qualifying primary residence. Check the exact street address on the official USDA map before touring, making an offer, or paying inspection fees. Then compare your total household income with the limit for that county and household size, as noted by Baltimore Chronicle.

A property can sit only a few blocks outside an excluded city boundary and still qualify. However, an eligible address does not guarantee loan approval. The borrower must also meet income, occupancy, credit, debt, appraisal, and lender requirements.

Key takeaways

- USDA eligibility is determined by the property’s exact address, not merely its county, ZIP code, or rural appearance.

- Guaranteed-loan household income generally cannot exceed 115% of the applicable median household income.

- The USDA map offers an initial screening result, while Rural Development makes the final property eligibility determination.

In plain English

Think of USDA eligibility as 2 locked doors. The first door tests the home’s location. The second tests the household’s finances.

A buyer must open both doors. A house may appear rural and still fall inside an excluded area. A household may also earn too much, even when the property qualifies.

The program is called “rural,” but eligible communities can include suburbs, small cities, county seats, and areas near major metropolitan markets.

The boundaries do not follow a simple national population rule visible to consumers. They are based on federal rural-area definitions and USDA determinations. That makes an address search more reliable than assumptions based on town size.

Buyers comparing mortgage choices can also review first-time homebuyer programs available in 2026. USDA financing is not limited to first-time buyers, but it often competes with FHA and conventional low-down-payment loans.

How USDA loan eligible areas 2026 actually work

The official USDA property eligibility map lets buyers search a complete address. Enter the street number, street name, city, state, and ZIP code. The tool then places the property against current program boundaries.

An eligible result means the location passes the initial geographic test. It does not mean the house meets appraisal standards. It also does not confirm the borrower’s income or credit qualification.

When a property appears ineligible, zoom in carefully. Boundary lines can run through ZIP codes, subdivisions, roads, or growing communities. Search the exact address rather than relying on a real estate listing’s town name.

USDA warns that the online map is not a final agency decision. Rural Development determines final eligibility after receiving a complete application. Buyers should keep this condition in their purchase contract when location eligibility remains uncertain.

How to check an address before making an offer

Use the following process before spending money on an inspection, appraisal, survey, or attorney review:

- Open the official USDA Single Family Housing property eligibility map.

- Accept the property eligibility disclaimer shown by the agency.

- Enter the complete street address, city, state, and ZIP code.

- Zoom in and confirm the marker falls outside an ineligible shaded area.

- Save a screenshot or PDF showing the search result and date.

- Ask a USDA-approved lender to confirm the address before contract deadlines expire.

The saved result can help a lender identify map discrepancies. It also records what the public tool displayed when the buyer made the offer. Still, it does not override the agency’s final determination.

Check new-construction addresses with extra care. Recently assigned streets may not appear correctly in older address databases. A lender may need a parcel number, legal description, county record, or USDA review.

Do not search only by ZIP code. One ZIP code can include both eligible and ineligible properties. Two houses with the same mailing city may receive different results.

Buyers should also verify the address again before closing. Eligibility boundaries and agency records can change. A current lender review offers better protection than an old screenshot from a listing agent.

How income limits are checked

The USDA Guaranteed Loan Program generally limits household income to 115% of the applicable median household income. The exact dollar ceiling varies by location and household size. Limits can differ between counties within the same state.

USDA considers household income, which can be broader than the income used to qualify for the mortgage. Earnings from certain adult household members may count even when they are not loan applicants.

The agency may allow deductions when calculating adjusted household income. These can involve dependents, child care costs, disability-related expenses, and elderly household status. The lender must apply current USDA rules to the household’s documented circumstances.

| Income concept | What it generally measures | Why it matters |

|---|---|---|

| Annual household income | Qualifying income from relevant household members before allowed deductions | Establishes the starting point for program eligibility |

| Adjusted household income | Annual income after eligible USDA deductions | Compared with the local program income limit |

| Repayment income | Stable income used by the lender to evaluate mortgage repayment | Helps determine whether the borrower can afford the loan |

| Area income limit | USDA ceiling based on location and household size | Determines whether household income is within program rules |

These categories explain why an online mortgage calculator cannot confirm USDA approval. A household may pass the program income test but lack enough repayment income. Another household may afford the payment but exceed the local income ceiling.

Income from overtime, bonuses, commissions, self-employment, retirement, benefits, or a second job may require additional documentation. Lenders often review tax returns, pay stubs, bank statements, employment records, and benefit letters.

Household changes also matter. A working adult moving into the home can affect program income. A dependent leaving may alter both household size and available deductions.

Use USDA’s current income tool rather than a third-party chart. Published limits can be revised. The applicable amount depends on the property’s county and the number of household members.

Who it matters to in 2026

Buyers priced out of nearby cities

A renter searching around Atlanta, Dallas, Nashville, Raleigh, Phoenix, or another expanding metro may find eligible properties beyond excluded urban boundaries. The commute may increase, but the financing can reduce upfront cash requirements.

A $300,000 home with 3.5% down requires $10,500 before closing costs. A 5% down payment requires $15,000. A qualifying USDA loan may allow 100% financing, although closing costs and reserves can still require cash.

Moderate-income households with limited savings

USDA loans can suit buyers with stable income but little money saved for a down payment. The program does not eliminate affordability checks. Property taxes, homeowners insurance, association dues, debt, and the interest rate still affect approval.

Before choosing a loan, compare the full cash requirement. Baltimore Chronicle’s guide to down payments for a house in 2026 explains how USDA compares with FHA, VA, and conventional options.

Existing homeowners planning another purchase

USDA financing is not automatically restricted to first-time buyers. However, the new property must usually serve as the borrower’s primary residence. The lender must also examine any existing home ownership and occupancy circumstances.

A buyer should not assume that owning another property creates an automatic denial. The facts, occupancy plan, housing adequacy, and program guidance require lender review.

USDA loan costs and property conditions

A USDA guaranteed loan can offer 100% financing, but it is not free financing. The program generally includes an upfront guarantee fee and an annual fee. The annual charge is usually collected through the monthly mortgage payment.

USDA materials have commonly listed a 1% upfront guarantee fee and a 0.35% annual fee. Borrowers must verify the effective charges for their closing date. Program fees can change through official annual guidance.

The upfront fee may often be financed when the appraised value and loan structure permit it. Financing the fee reduces cash at closing but increases the loan balance and total interest paid.

The home must be a qualifying primary residence. It should be modest, safe, sanitary, and suitable for residential use. Existing homes, certain new homes, approved condominiums, and planned-unit properties may qualify when program requirements are met.

USDA financing is not intended for a vacation property or a property primarily designed to produce income. Large commercial features, extensive working farmland, or income-producing structures can create eligibility problems.

Documents to prepare before lender review

An early document review helps prevent delays after the buyer signs a contract. Requirements vary by lender, employment type, and household structure.

- Recent pay stubs covering the lender’s requested period

- W-2 forms and federal tax returns when required

- Bank, investment, and retirement account statements

- Identification and Social Security information

- Employment history and employer contact details

- Records for bonuses, overtime, commissions, or second jobs

- Self-employment profit-and-loss statements and business returns

- Benefit, pension, child support, or alimony documentation

- Names, ages, and income details for relevant household members

Provide complete statements, including blank pages. Large deposits may need a documented source. Moving money between accounts shortly before underwriting can create avoidable questions.

Self-employed applicants should prepare earlier. Lenders may analyze business income, noncash expenses, declining revenue, ownership percentage, and current-year performance. Taxable income alone may not equal qualifying income.

Do not hide income from an adult household member because that person is not applying. USDA program eligibility and mortgage underwriting use different income concepts. An omission can delay approval or create a compliance issue.

Keep digital copies in a secure folder. Updated pay stubs and bank statements may be requested before closing. Fast responses help protect financing deadlines in the purchase agreement.

Common myths

Several assumptions cause buyers to reject USDA financing too early or pursue homes that cannot qualify:

- Myth: Only farms qualify. Correction: USDA housing loans finance eligible primary residences, not only agricultural properties.

- Myth: Every small town qualifies. Correction: The exact address must fall within a current eligible boundary.

- Myth: USDA loans are only for first-time buyers. Correction: Qualified repeat buyers may also use the program.

- Myth: Zero down means zero cash. Correction: Buyers may still pay inspections, closing costs, prepaid expenses, and reserves.

- Myth: The map result guarantees approval. Correction: USDA makes the final determination after reviewing a complete application.

The “farm loan” myth is especially persistent because USDA administers agricultural programs. Rural Development’s housing programs serve residential buyers in eligible communities.

Zero-down financing also needs context. Sellers may contribute toward permitted costs, and some expenses may be financed. However, the available structure depends on the appraisal, contract, lender, and program limits.

Buyers should compare interest rates and total costs, not only the down payment. USDA, FHA, VA, and conventional loans use different fees and underwriting rules.

Closing expenses can materially change the budget. The Baltimore Chronicle guide to closing costs on a house separates lender charges, title costs, prepaid taxes, insurance, and escrow deposits.

FAQ about USDA loan eligible areas 2026

How do I know whether my house is in a USDA eligible area?

Search the complete address on the official USDA property eligibility map. Then ask a USDA-approved lender to verify the result. The online map provides preliminary guidance, while USDA makes the final determination.

Can part of a city qualify for a USDA loan?

Yes. Eligibility boundaries can divide cities, ZIP codes, roads, and subdivisions. A mailing address may use a city name even when the property lies outside the excluded urban boundary.

What is the USDA income limit for 2026?

There is no single national dollar limit. Guaranteed-loan income generally cannot exceed 115% of the applicable median household income. The actual ceiling depends on location and household size.

Does everyone living in the house count toward the income limit?

Income from relevant adult household members may count, even when they are not borrowers. USDA rules also provide certain deductions when calculating adjusted household income.

Can I use a USDA loan for an investment property?

No. USDA single-family housing financing is designed for an eligible primary residence. Vacation homes and properties primarily intended to generate income generally do not qualify.

Can a USDA map change after I make an offer?

Boundaries and records can change. Include a financing contingency and obtain lender confirmation early. Recheck the address before closing when eligibility is essential to the purchase.USDA loan eligible areas 2026 are locations where buyers may use USDA-backed financing for a qualifying primary residence. Check the exact street address on the official USDA map before touring, making an offer, or paying inspection fees. Then compare your total household income with the limit for that county and household size, as noted by Baltimore Chronicle.

A property can sit only a few blocks outside an excluded city boundary and still qualify. However, an eligible address does not guarantee loan approval. The borrower must also meet income, occupancy, credit, debt, appraisal, and lender requirements.

Key takeaways

- USDA eligibility is determined by the property’s exact address, not merely its county, ZIP code, or rural appearance.

- Guaranteed-loan household income generally cannot exceed 115% of the applicable median household income.

- The USDA map offers an initial screening result, while Rural Development makes the final property eligibility determination.

In plain English

Think of USDA eligibility as 2 locked doors. The first door tests the home’s location. The second tests the household’s finances.

A buyer must open both doors. A house may appear rural and still fall inside an excluded area. A household may also earn too much, even when the property qualifies.

The program is called “rural,” but eligible communities can include suburbs, small cities, county seats, and areas near major metropolitan markets.

The boundaries do not follow a simple national population rule visible to consumers. They are based on federal rural-area definitions and USDA determinations. That makes an address search more reliable than assumptions based on town size.

Buyers comparing mortgage choices can also review first-time homebuyer programs available in 2026. USDA financing is not limited to first-time buyers, but it often competes with FHA and conventional low-down-payment loans.

How USDA loan eligible areas 2026 actually work

The official USDA property eligibility map lets buyers search a complete address. Enter the street number, street name, city, state, and ZIP code. The tool then places the property against current program boundaries.

An eligible result means the location passes the initial geographic test. It does not mean the house meets appraisal standards. It also does not confirm the borrower’s income or credit qualification.

When a property appears ineligible, zoom in carefully. Boundary lines can run through ZIP codes, subdivisions, roads, or growing communities. Search the exact address rather than relying on a real estate listing’s town name.

USDA warns that the online map is not a final agency decision. Rural Development determines final eligibility after receiving a complete application. Buyers should keep this condition in their purchase contract when location eligibility remains uncertain.

How to check an address before making an offer

Use the following process before spending money on an inspection, appraisal, survey, or attorney review:

- Open the official USDA Single Family Housing property eligibility map.

- Accept the property eligibility disclaimer shown by the agency.

- Enter the complete street address, city, state, and ZIP code.

- Zoom in and confirm the marker falls outside an ineligible shaded area.

- Save a screenshot or PDF showing the search result and date.

- Ask a USDA-approved lender to confirm the address before contract deadlines expire.

The saved result can help a lender identify map discrepancies. It also records what the public tool displayed when the buyer made the offer. Still, it does not override the agency’s final determination.

Check new-construction addresses with extra care. Recently assigned streets may not appear correctly in older address databases. A lender may need a parcel number, legal description, county record, or USDA review.

Do not search only by ZIP code. One ZIP code can include both eligible and ineligible properties. Two houses with the same mailing city may receive different results.

Buyers should also verify the address again before closing. Eligibility boundaries and agency records can change. A current lender review offers better protection than an old screenshot from a listing agent.

How income limits are checked

The USDA Guaranteed Loan Program generally limits household income to 115% of the applicable median household income. The exact dollar ceiling varies by location and household size. Limits can differ between counties within the same state.

USDA considers household income, which can be broader than the income used to qualify for the mortgage. Earnings from certain adult household members may count even when they are not loan applicants.

The agency may allow deductions when calculating adjusted household income. These can involve dependents, child care costs, disability-related expenses, and elderly household status. The lender must apply current USDA rules to the household’s documented circumstances.

| Income concept | What it generally measures | Why it matters |

|---|---|---|

| Annual household income | Qualifying income from relevant household members before allowed deductions | Establishes the starting point for program eligibility |

| Adjusted household income | Annual income after eligible USDA deductions | Compared with the local program income limit |

| Repayment income | Stable income used by the lender to evaluate mortgage repayment | Helps determine whether the borrower can afford the loan |

| Area income limit | USDA ceiling based on location and household size | Determines whether household income is within program rules |

These categories explain why an online mortgage calculator cannot confirm USDA approval. A household may pass the program income test but lack enough repayment income. Another household may afford the payment but exceed the local income ceiling.

Income from overtime, bonuses, commissions, self-employment, retirement, benefits, or a second job may require additional documentation. Lenders often review tax returns, pay stubs, bank statements, employment records, and benefit letters.

Household changes also matter. A working adult moving into the home can affect program income. A dependent leaving may alter both household size and available deductions.

Use USDA’s current income tool rather than a third-party chart. Published limits can be revised. The applicable amount depends on the property’s county and the number of household members.

Who it matters to in 2026

Buyers priced out of nearby cities

A renter searching around Atlanta, Dallas, Nashville, Raleigh, Phoenix, or another expanding metro may find eligible properties beyond excluded urban boundaries. The commute may increase, but the financing can reduce upfront cash requirements.

A $300,000 home with 3.5% down requires $10,500 before closing costs. A 5% down payment requires $15,000. A qualifying USDA loan may allow 100% financing, although closing costs and reserves can still require cash.

Moderate-income households with limited savings

USDA loans can suit buyers with stable income but little money saved for a down payment. The program does not eliminate affordability checks. Property taxes, homeowners insurance, association dues, debt, and the interest rate still affect approval.

Before choosing a loan, compare the full cash requirement. Baltimore Chronicle’s guide to down payments for a house in 2026 explains how USDA compares with FHA, VA, and conventional options.

Existing homeowners planning another purchase

USDA financing is not automatically restricted to first-time buyers. However, the new property must usually serve as the borrower’s primary residence. The lender must also examine any existing home ownership and occupancy circumstances.

A buyer should not assume that owning another property creates an automatic denial. The facts, occupancy plan, housing adequacy, and program guidance require lender review.

USDA loan costs and property conditions

A USDA guaranteed loan can offer 100% financing, but it is not free financing. The program generally includes an upfront guarantee fee and an annual fee. The annual charge is usually collected through the monthly mortgage payment.

USDA materials have commonly listed a 1% upfront guarantee fee and a 0.35% annual fee. Borrowers must verify the effective charges for their closing date. Program fees can change through official annual guidance.

The upfront fee may often be financed when the appraised value and loan structure permit it. Financing the fee reduces cash at closing but increases the loan balance and total interest paid.

The home must be a qualifying primary residence. It should be modest, safe, sanitary, and suitable for residential use. Existing homes, certain new homes, approved condominiums, and planned-unit properties may qualify when program requirements are met.

USDA financing is not intended for a vacation property or a property primarily designed to produce income. Large commercial features, extensive working farmland, or income-producing structures can create eligibility problems.

Documents to prepare before lender review

An early document review helps prevent delays after the buyer signs a contract. Requirements vary by lender, employment type, and household structure.

- Recent pay stubs covering the lender’s requested period

- W-2 forms and federal tax returns when required

- Bank, investment, and retirement account statements

- Identification and Social Security information

- Employment history and employer contact details

- Records for bonuses, overtime, commissions, or second jobs

- Self-employment profit-and-loss statements and business returns

- Benefit, pension, child support, or alimony documentation

- Names, ages, and income details for relevant household members

Provide complete statements, including blank pages. Large deposits may need a documented source. Moving money between accounts shortly before underwriting can create avoidable questions.

Self-employed applicants should prepare earlier. Lenders may analyze business income, noncash expenses, declining revenue, ownership percentage, and current-year performance. Taxable income alone may not equal qualifying income.

Do not hide income from an adult household member because that person is not applying. USDA program eligibility and mortgage underwriting use different income concepts. An omission can delay approval or create a compliance issue.

Keep digital copies in a secure folder. Updated pay stubs and bank statements may be requested before closing. Fast responses help protect financing deadlines in the purchase agreement.

Common myths

Several assumptions cause buyers to reject USDA financing too early or pursue homes that cannot qualify:

- Myth: Only farms qualify. Correction: USDA housing loans finance eligible primary residences, not only agricultural properties.

- Myth: Every small town qualifies. Correction: The exact address must fall within a current eligible boundary.

- Myth: USDA loans are only for first-time buyers. Correction: Qualified repeat buyers may also use the program.

- Myth: Zero down means zero cash. Correction: Buyers may still pay inspections, closing costs, prepaid expenses, and reserves.

- Myth: The map result guarantees approval. Correction: USDA makes the final determination after reviewing a complete application.

The “farm loan” myth is especially persistent because USDA administers agricultural programs. Rural Development’s housing programs serve residential buyers in eligible communities.

Zero-down financing also needs context. Sellers may contribute toward permitted costs, and some expenses may be financed. However, the available structure depends on the appraisal, contract, lender, and program limits.

Buyers should compare interest rates and total costs, not only the down payment. USDA, FHA, VA, and conventional loans use different fees and underwriting rules.

Closing expenses can materially change the budget. The Baltimore Chronicle guide to closing costs on a house separates lender charges, title costs, prepaid taxes, insurance, and escrow deposits.

FAQ about USDA loan eligible areas 2026

How do I know whether my house is in a USDA eligible area?

Search the complete address on the official USDA property eligibility map. Then ask a USDA-approved lender to verify the result. The online map provides preliminary guidance, while USDA makes the final determination.

Can part of a city qualify for a USDA loan?

Yes. Eligibility boundaries can divide cities, ZIP codes, roads, and subdivisions. A mailing address may use a city name even when the property lies outside the excluded urban boundary.

What is the USDA income limit for 2026?

There is no single national dollar limit. Guaranteed-loan income generally cannot exceed 115% of the applicable median household income. The actual ceiling depends on location and household size.

Does everyone living in the house count toward the income limit?

Income from relevant adult household members may count, even when they are not borrowers. USDA rules also provide certain deductions when calculating adjusted household income.

Can I use a USDA loan for an investment property?

No. USDA single-family housing financing is designed for an eligible primary residence. Vacation homes and properties primarily intended to generate income generally do not qualify.

Can a USDA map change after I make an offer?

Boundaries and records can change. Include a financing contingency and obtain lender confirmation early. Recheck the address before closing when eligibility is essential to the purchase.USDA loan eligible areas 2026 are locations where buyers may use USDA-backed financing for a qualifying primary residence. Check the exact street address on the official USDA map before touring, making an offer, or paying inspection fees. Then compare your total household income with the limit for that county and household size, as noted by Baltimore Chronicle.

A property can sit only a few blocks outside an excluded city boundary and still qualify. However, an eligible address does not guarantee loan approval. The borrower must also meet income, occupancy, credit, debt, appraisal, and lender requirements.

Key takeaways

- USDA eligibility is determined by the property’s exact address, not merely its county, ZIP code, or rural appearance.

- Guaranteed-loan household income generally cannot exceed 115% of the applicable median household income.

- The USDA map offers an initial screening result, while Rural Development makes the final property eligibility determination.

In plain English

Think of USDA eligibility as 2 locked doors. The first door tests the home’s location. The second tests the household’s finances.

A buyer must open both doors. A house may appear rural and still fall inside an excluded area. A household may also earn too much, even when the property qualifies.

The program is called “rural,” but eligible communities can include suburbs, small cities, county seats, and areas near major metropolitan markets.

The boundaries do not follow a simple national population rule visible to consumers. They are based on federal rural-area definitions and USDA determinations. That makes an address search more reliable than assumptions based on town size.

Buyers comparing mortgage choices can also review first-time homebuyer programs available in 2026. USDA financing is not limited to first-time buyers, but it often competes with FHA and conventional low-down-payment loans.

How USDA loan eligible areas 2026 actually work

The official USDA property eligibility map lets buyers search a complete address. Enter the street number, street name, city, state, and ZIP code. The tool then places the property against current program boundaries.

An eligible result means the location passes the initial geographic test. It does not mean the house meets appraisal standards. It also does not confirm the borrower’s income or credit qualification.

When a property appears ineligible, zoom in carefully. Boundary lines can run through ZIP codes, subdivisions, roads, or growing communities. Search the exact address rather than relying on a real estate listing’s town name.

USDA warns that the online map is not a final agency decision. Rural Development determines final eligibility after receiving a complete application. Buyers should keep this condition in their purchase contract when location eligibility remains uncertain.

How to check an address before making an offer

Use the following process before spending money on an inspection, appraisal, survey, or attorney review:

- Open the official USDA Single Family Housing property eligibility map.

- Accept the property eligibility disclaimer shown by the agency.

- Enter the complete street address, city, state, and ZIP code.

- Zoom in and confirm the marker falls outside an ineligible shaded area.

- Save a screenshot or PDF showing the search result and date.

- Ask a USDA-approved lender to confirm the address before contract deadlines expire.

The saved result can help a lender identify map discrepancies. It also records what the public tool displayed when the buyer made the offer. Still, it does not override the agency’s final determination.

Check new-construction addresses with extra care. Recently assigned streets may not appear correctly in older address databases. A lender may need a parcel number, legal description, county record, or USDA review.

Do not search only by ZIP code. One ZIP code can include both eligible and ineligible properties. Two houses with the same mailing city may receive different results.

Buyers should also verify the address again before closing. Eligibility boundaries and agency records can change. A current lender review offers better protection than an old screenshot from a listing agent.

How income limits are checked

The USDA Guaranteed Loan Program generally limits household income to 115% of the applicable median household income. The exact dollar ceiling varies by location and household size. Limits can differ between counties within the same state.

USDA considers household income, which can be broader than the income used to qualify for the mortgage. Earnings from certain adult household members may count even when they are not loan applicants.

The agency may allow deductions when calculating adjusted household income. These can involve dependents, child care costs, disability-related expenses, and elderly household status. The lender must apply current USDA rules to the household’s documented circumstances.

| Income concept | What it generally measures | Why it matters |

|---|---|---|

| Annual household income | Qualifying income from relevant household members before allowed deductions | Establishes the starting point for program eligibility |

| Adjusted household income | Annual income after eligible USDA deductions | Compared with the local program income limit |

| Repayment income | Stable income used by the lender to evaluate mortgage repayment | Helps determine whether the borrower can afford the loan |

| Area income limit | USDA ceiling based on location and household size | Determines whether household income is within program rules |

These categories explain why an online mortgage calculator cannot confirm USDA approval. A household may pass the program income test but lack enough repayment income. Another household may afford the payment but exceed the local income ceiling.

Income from overtime, bonuses, commissions, self-employment, retirement, benefits, or a second job may require additional documentation. Lenders often review tax returns, pay stubs, bank statements, employment records, and benefit letters.

Household changes also matter. A working adult moving into the home can affect program income. A dependent leaving may alter both household size and available deductions.

Use USDA’s current income tool rather than a third-party chart. Published limits can be revised. The applicable amount depends on the property’s county and the number of household members.

Who it matters to in 2026

Buyers priced out of nearby cities

A renter searching around Atlanta, Dallas, Nashville, Raleigh, Phoenix, or another expanding metro may find eligible properties beyond excluded urban boundaries. The commute may increase, but the financing can reduce upfront cash requirements.

A $300,000 home with 3.5% down requires $10,500 before closing costs. A 5% down payment requires $15,000. A qualifying USDA loan may allow 100% financing, although closing costs and reserves can still require cash.

Moderate-income households with limited savings

USDA loans can suit buyers with stable income but little money saved for a down payment. The program does not eliminate affordability checks. Property taxes, homeowners insurance, association dues, debt, and the interest rate still affect approval.

Before choosing a loan, compare the full cash requirement. Baltimore Chronicle’s guide to down payments for a house in 2026 explains how USDA compares with FHA, VA, and conventional options.

Existing homeowners planning another purchase

USDA financing is not automatically restricted to first-time buyers. However, the new property must usually serve as the borrower’s primary residence. The lender must also examine any existing home ownership and occupancy circumstances.

A buyer should not assume that owning another property creates an automatic denial. The facts, occupancy plan, housing adequacy, and program guidance require lender review.

USDA loan costs and property conditions

A USDA guaranteed loan can offer 100% financing, but it is not free financing. The program generally includes an upfront guarantee fee and an annual fee. The annual charge is usually collected through the monthly mortgage payment.

USDA materials have commonly listed a 1% upfront guarantee fee and a 0.35% annual fee. Borrowers must verify the effective charges for their closing date. Program fees can change through official annual guidance.

The upfront fee may often be financed when the appraised value and loan structure permit it. Financing the fee reduces cash at closing but increases the loan balance and total interest paid.

The home must be a qualifying primary residence. It should be modest, safe, sanitary, and suitable for residential use. Existing homes, certain new homes, approved condominiums, and planned-unit properties may qualify when program requirements are met.

USDA financing is not intended for a vacation property or a property primarily designed to produce income. Large commercial features, extensive working farmland, or income-producing structures can create eligibility problems.

Documents to prepare before lender review

An early document review helps prevent delays after the buyer signs a contract. Requirements vary by lender, employment type, and household structure.

- Recent pay stubs covering the lender’s requested period

- W-2 forms and federal tax returns when required

- Bank, investment, and retirement account statements

- Identification and Social Security information

- Employment history and employer contact details

- Records for bonuses, overtime, commissions, or second jobs

- Self-employment profit-and-loss statements and business returns

- Benefit, pension, child support, or alimony documentation

- Names, ages, and income details for relevant household members

Provide complete statements, including blank pages. Large deposits may need a documented source. Moving money between accounts shortly before underwriting can create avoidable questions.

Self-employed applicants should prepare earlier. Lenders may analyze business income, noncash expenses, declining revenue, ownership percentage, and current-year performance. Taxable income alone may not equal qualifying income.

Do not hide income from an adult household member because that person is not applying. USDA program eligibility and mortgage underwriting use different income concepts. An omission can delay approval or create a compliance issue.

Keep digital copies in a secure folder. Updated pay stubs and bank statements may be requested before closing. Fast responses help protect financing deadlines in the purchase agreement.

Common myths

Several assumptions cause buyers to reject USDA financing too early or pursue homes that cannot qualify:

- Myth: Only farms qualify. Correction: USDA housing loans finance eligible primary residences, not only agricultural properties.

- Myth: Every small town qualifies. Correction: The exact address must fall within a current eligible boundary.

- Myth: USDA loans are only for first-time buyers. Correction: Qualified repeat buyers may also use the program.

- Myth: Zero down means zero cash. Correction: Buyers may still pay inspections, closing costs, prepaid expenses, and reserves.

- Myth: The map result guarantees approval. Correction: USDA makes the final determination after reviewing a complete application.

The “farm loan” myth is especially persistent because USDA administers agricultural programs. Rural Development’s housing programs serve residential buyers in eligible communities.

Zero-down financing also needs context. Sellers may contribute toward permitted costs, and some expenses may be financed. However, the available structure depends on the appraisal, contract, lender, and program limits.

Buyers should compare interest rates and total costs, not only the down payment. USDA, FHA, VA, and conventional loans use different fees and underwriting rules.

Closing expenses can materially change the budget. The Baltimore Chronicle guide to closing costs on a house separates lender charges, title costs, prepaid taxes, insurance, and escrow deposits.

FAQ about USDA loan eligible areas 2026

How do I know whether my house is in a USDA eligible area?

Search the complete address on the official USDA property eligibility map. Then ask a USDA-approved lender to verify the result. The online map provides preliminary guidance, while USDA makes the final determination.

Can part of a city qualify for a USDA loan?

Yes. Eligibility boundaries can divide cities, ZIP codes, roads, and subdivisions. A mailing address may use a city name even when the property lies outside the excluded urban boundary.

What is the USDA income limit for 2026?

There is no single national dollar limit. Guaranteed-loan income generally cannot exceed 115% of the applicable median household income. The actual ceiling depends on location and household size.

Does everyone living in the house count toward the income limit?

Income from relevant adult household members may count, even when they are not borrowers. USDA rules also provide certain deductions when calculating adjusted household income.

Can I use a USDA loan for an investment property?

No. USDA single-family housing financing is designed for an eligible primary residence. Vacation homes and properties primarily intended to generate income generally do not qualify.

Can a USDA map change after I make an offer?

Boundaries and records can change. Include a financing contingency and obtain lender confirmation early. Recheck the address before closing when eligibility is essential to the purchase.

Earlier we wrote about How to Win an eBay Return Dispute 2026: Evidence, MBG Rules and Appeals