How to get a construction loan 2026 USA is mostly about proving 3 things: you can repay the debt, the builder can finish the project, and the home will be worth enough when construction ends. You can prepare the core file in 2–7 days if your income documents, land papers, plans, bids, and credit profile are already organized, as noted by Baltimore Chronicle.

This guide shows what lenders check, which documents slow approvals, how construction-to-permanent loans differ from renovation loans, and where borrowers usually lose time. The practical target is simple: walk into a bank, credit union, or mortgage lender with a file that looks financeable before the underwriter asks for it.

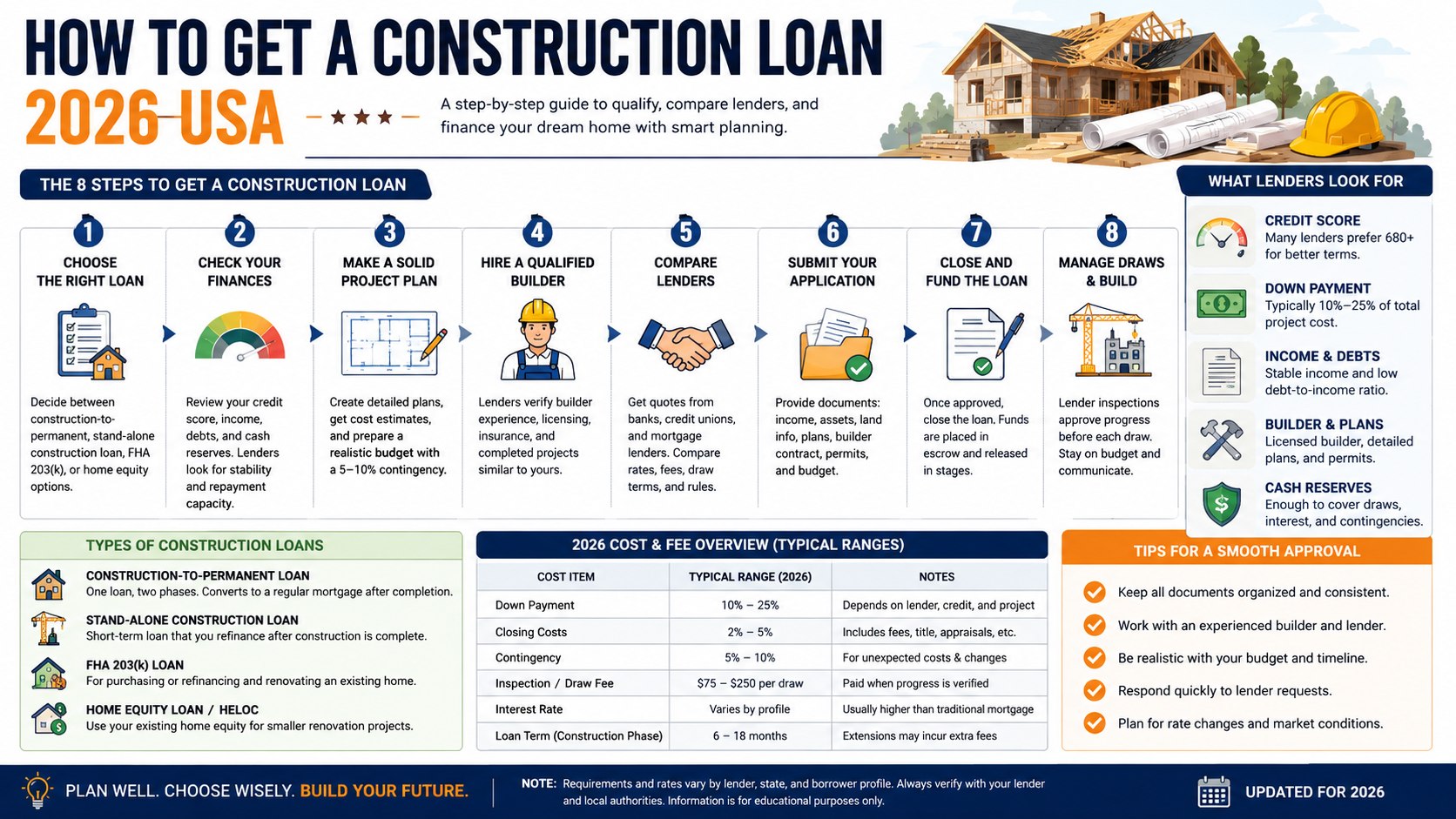

How to Get a Construction Loan 2026 USA

Key takeaways:

- Most lenders want strong credit, verified income, a detailed budget, approved plans, and a licensed builder before issuing a commitment.

- Construction loans in 2026 usually fund the project in draws, not one lump sum, after inspections confirm progress.

- Compare local banks, credit unions, and national lenders because land rules, down payments, and builder requirements vary by state.

What you need before applying for a construction loan in 2026

Before you contact lenders, assemble a file that answers the questions an underwriter will ask first. A construction loan is not priced like a regular mortgage because the home is not finished yet. The lender is financing an asset that still depends on permits, materials, labor, weather, inspections, and the builder’s performance.

You will usually need these items before a serious quote:

- Government ID, Social Security number, and current address history.

- 2 years of W-2s or 1099s, recent pay stubs, tax returns, and bank statements.

- Credit profile strong enough for mortgage underwriting, often cleaner than minimum purchase-loan standards.

- Land deed, purchase contract, or lot settlement statement if you already own the parcel.

- Building plans, specifications, signed builder contract, and itemized cost breakdown.

- Permit status, zoning notes, survey, soil report, and utility access details where required.

- Cash for down payment, closing costs, interest reserve, inspections, and contingency funds.

After this list, check your documents for consistency. The name on the land deed should match the borrower or legal entity applying for the loan. The builder contract should match the square footage, finish level, garage count, site work, and allowances used in the budget.

If the plans say 2,400 sq ft and the cost sheet prices 2,100 sq ft, the file may stall. Keep a separate folder for change orders, because lenders dislike unexplained cost movement. For broader cost planning before the loan conversation, read how much it costs to build a house in the USA in 2026.

Step 1: Choose the right type of construction financing

Decide whether you need a construction-to-permanent loan, a stand-alone construction loan, a renovation mortgage, or a home equity product. A construction-to-permanent loan starts as short-term construction financing and converts into a regular mortgage after completion.

This matters because each option changes the closing process, rate risk, inspection schedule, and cash needed. A one-time close may reduce duplicate closing costs, while a two-time close can offer more flexibility if you want to shop the permanent mortgage later.

The common mistake is asking for “a construction loan” without knowing whether the project is a new build, major renovation, teardown, ADU, modular home, or owner-builder project.

| Loan path | Best fit | What lenders usually review harder |

|---|---|---|

| Construction-to-permanent loan | New primary home on owned or purchased land | Builder contract, appraisal “subject to completion,” reserves |

| Stand-alone construction loan | Borrowers who plan to refinance after completion | Exit strategy, interest reserve, refinance risk |

| FHA 203(k) | Buying or refinancing and rehabilitating an older home | Eligible repairs, HUD rules, consultant role when required |

| Home equity loan or HELOC | Smaller remodel on an existing home | Available equity, combined loan-to-value ratio, repayment capacity |

Use this comparison as a first filter, not a final decision. FHA 203(k) can be useful for rehabilitation, but it is not a blank check for every custom build. HUD says Section 203(k) covers purchase or refinance plus rehabilitation of a home that is at least 1 year old, and HUD lists a Limited 203(k) option for repairs up to $75,000.

For a ground-up build in Texas, Florida, Ohio, Arizona, Georgia, or Maryland, a bank construction product is usually the conversation to start. For an older rowhouse renovation in Baltimore, Philadelphia, or Chicago, a renovation loan may deserve a closer look.

Step 2: Check credit, income, and cash before lenders do

Pull your credit reports, confirm your debt payments, and estimate the future mortgage payment before submitting applications. In 2026, many borrowers are still dealing with elevated mortgage rates, so payment shock matters.

Lenders will examine debt-to-income ratio, job history, self-employment income, cash reserves, and large recent deposits. They need proof that you can carry housing costs during construction and after the loan converts.

The mistake to avoid is spending down cash on design deposits, appliances, or land improvements before the lender verifies reserves.

Step 3: Build a lender-ready project budget

Create a line-item budget that separates land, site work, foundation, framing, roofing, windows, HVAC, electrical, plumbing, insulation, drywall, finishes, driveway, landscaping, permits, and contingency. Do not rely on a one-page estimate if the project costs hundreds of thousands of dollars.

This matters because the lender’s appraisal, draw schedule, and loan amount depend on the cost breakdown. A missing septic system, utility trench, stormwater fee, or impact fee can break the numbers late in underwriting.

The mistake to avoid is treating allowances as real prices. If the kitchen allowance says $18,000 but the borrower wants Sub-Zero refrigeration, Wolf appliances, quartz counters, and custom cabinetry, the lender will see a gap. Before sending a builder’s bid to the bank, check how to read a construction estimate in 2026, because unclear line items often create lender questions.

Step 4: Select a builder lenders will approve

Choose a licensed, insured builder with verifiable experience in the state where the home will be built. Ask for proof of general liability coverage, workers’ compensation, trade references, supplier references, and completed projects close to your planned size and finish level.

This matters because lenders underwrite the builder as part of the risk. A strong borrower with a weak contractor can still receive a denial or a long list of conditions.

The mistake to avoid is signing with a builder before asking whether local lenders accept that builder’s contract format, insurance, draw process, and warranty terms.

Step 5: Compare lenders for how to get a construction loan 2026 USA

Request quotes from 3–5 sources: a local bank, a credit union, a regional mortgage lender, a national bank, and one lender with strong construction experience in your state. Ask each lender the same questions so the comparison is fair.

This matters because pricing is only part of the deal. Draw fees, inspection fees, interest-only terms, lock policy, permanent mortgage terms, contingency requirements, and maximum loan-to-cost can change the real cost.

The mistake to avoid is choosing the lowest advertised rate without asking how many closings, inspections, extensions, and re-inspections you may pay for.

Ask each lender these questions:

- Does the loan convert automatically to a permanent mortgage?

- Is the rate locked before construction, after completion, or both?

- How much down payment is required if the borrower already owns the land?

- How many draws are included, and what does each inspection cost?

- What happens if construction exceeds 12 months?

- Are owner-builder projects allowed?

- Can modular, manufactured, ADU, or barndominium projects qualify?

These questions reveal lender behavior better than marketing pages. Some local banks are excellent for rural land, septic systems, and custom builders. Some national lenders are better for standardized documentation and faster permanent-loan processing.

In California and Washington, permitting timelines can affect rate-lock choices. In Florida, wind insurance and flood zones can change escrow numbers. In Colorado or Montana, winter building schedules may force a longer construction term. Keep notes in one spreadsheet and compare total cash to close, not only monthly payment.

Step 6: Understand rates, fees, and the 2026 payment risk

Construction loan rates in 2026 often run higher than standard mortgage rates because the home is unfinished and draws are released over time. As of 2026, many borrowers should expect quotes to vary by credit score, loan size, state, project type, and whether the rate converts to permanent financing.

Use realistic ranges, then verify directly with the lender on the day you apply. CFPB guidance says a Loan Estimate is a 3-page form that provides key mortgage information after the lender receives the required application details.

The mistake to avoid is comparing a construction-only interest rate with a permanent fixed mortgage rate as if they were the same product.

| Cost item | 2026 planning range | Why it matters |

| Down payment | Often 10%–25% of project cost | Depends on credit, land equity, loan type, and lender appetite |

| Closing costs | Often 2%–5% of financed amount | CFPB uses this range for homebuyer planning, but actual costs vary |

| Contingency | Often 5%–10% of construction cost | Protects against price changes, mistakes, and change orders |

| Inspection or draw fee | Often $75–$250 per draw | Charged when progress is verified before funds are released |

| Extension fee | Varies by lender | Can appear if the build exceeds the approved term |

These figures are planning ranges, not promises. A $450,000 build in North Carolina will not price the same as a $950,000 custom home in New Jersey. Materials also matter: standing-seam metal roofing, Marvin or Andersen windows, high-SEER HVAC, spray foam insulation, and complex foundation work can change the budget fast.

Borrowers should also ask whether energy upgrades may qualify for tax credits. The IRS says qualifying home energy improvements may be eligible for credits in the year the improvements are made, but eligibility depends on the specific product and tax situation.

Step 7: Submit a clean application and respond quickly

Apply only after your plans, budget, land documents, income file, and builder package are ready. The lender may order an appraisal based on the finished home, then match that valuation against the proposed cost and requested loan amount.

This matters because construction underwriting moves through borrower review, builder review, appraisal, title, insurance, and closing. A delay in any one file can pause the whole loan.

The mistake to avoid is sending documents in fragments. Use named PDFs such as “2025 federal tax return,” “builder contract signed,” “site plan,” and “draw schedule.”

Step 8: Manage draws, inspections, and change orders after closing

After closing, the lender will release money in stages as work is completed. Typical draws may cover foundation, framing, rough mechanicals, drywall, finishes, and final completion.

This matters because the builder does not receive all funds upfront. Inspections protect the lender and borrower by confirming that completed work matches the draw request.

The mistake to avoid is approving expensive changes without lender approval. A larger deck, upgraded windows, or different siding can create a funding gap if the loan was sized around the original contract. If your project includes interior finishes after major construction, this Baltimore Chronicle guide on interior doors that combine design and long-term value can help connect product choices with budget control and resale value.

Troubleshooting construction loan problems

Most construction-loan setbacks are fixable if you identify the problem early. The key is to separate borrower issues, builder issues, land issues, and appraisal issues instead of treating every delay as a lender delay.

Common scenarios:

- Credit score dropped before closing: pause new credit cards, vehicle loans, and large purchases until the lender clears the file.

- Appraisal came in low: review comparable sales, finish level, sq ft, and site value before increasing cash contribution.

- Builder is not approved: ask the lender what documents are missing before switching contractors.

- Permit is delayed: request written status from the county or city office and update the lender immediately.

- Budget changed after approval: submit a revised contract, change-order log, and proof of extra cash if required.

Do not hide problems from the lender. Construction lending depends on controlled risk, not perfect projects. If a county in Maryland asks for a revised stormwater plan, the lender needs to know because timing and cost may change.

If a builder discovers unsuitable soil, the loan file may need a new contingency review. Clean communication can prevent a technical issue from becoming a funding crisis.

FAQ

What credit score do I need for a construction loan in 2026?

Many lenders prefer stronger credit than a basic mortgage file, often because the project carries more risk. Exact cutoffs vary by lender, loan type, down payment, and borrower reserves. A higher score can improve pricing and reduce conditions, but the builder and budget still matter.

Can I get a construction loan if I already own the land?

Yes, land equity can sometimes count toward the borrower’s contribution. The lender will review the deed, title, land value, zoning, access, utilities, and whether any loan is already secured by the parcel. Owned land helps only if the project still appraises and the borrower qualifies.

How long does construction loan approval take?

A clean file can move faster, but 30–60 days is a realistic planning window for many borrowers in 2026. Complex land, rural utilities, appraisal issues, or incomplete builder documents can extend the timeline. Start before your builder needs the first draw.

Is a construction-to-permanent loan better than a stand-alone construction loan?

It can be better if you want one closing and a clearer path to permanent financing. A stand-alone loan may work if you expect better terms after completion or need flexibility. Compare total costs, lock policy, and extension terms before deciding.

Do lenders allow owner-builder construction loans?

Some lenders allow them, but many restrict or reject owner-builder files. They may require professional experience, higher cash reserves, stronger credit, and more documentation. If you plan to act as your own general contractor, ask this question before ordering plans.

What is the biggest reason construction loan applications fail?

The most common failure is not one document. It is a weak total package: unclear budget, unapproved builder, low reserves, appraisal gap, or land issue. Fix the project file before trying to negotiate the rate.

Earlier we wrote about How to Change Your Name After Marriage in USA 2026: SSA, DMV, Passport