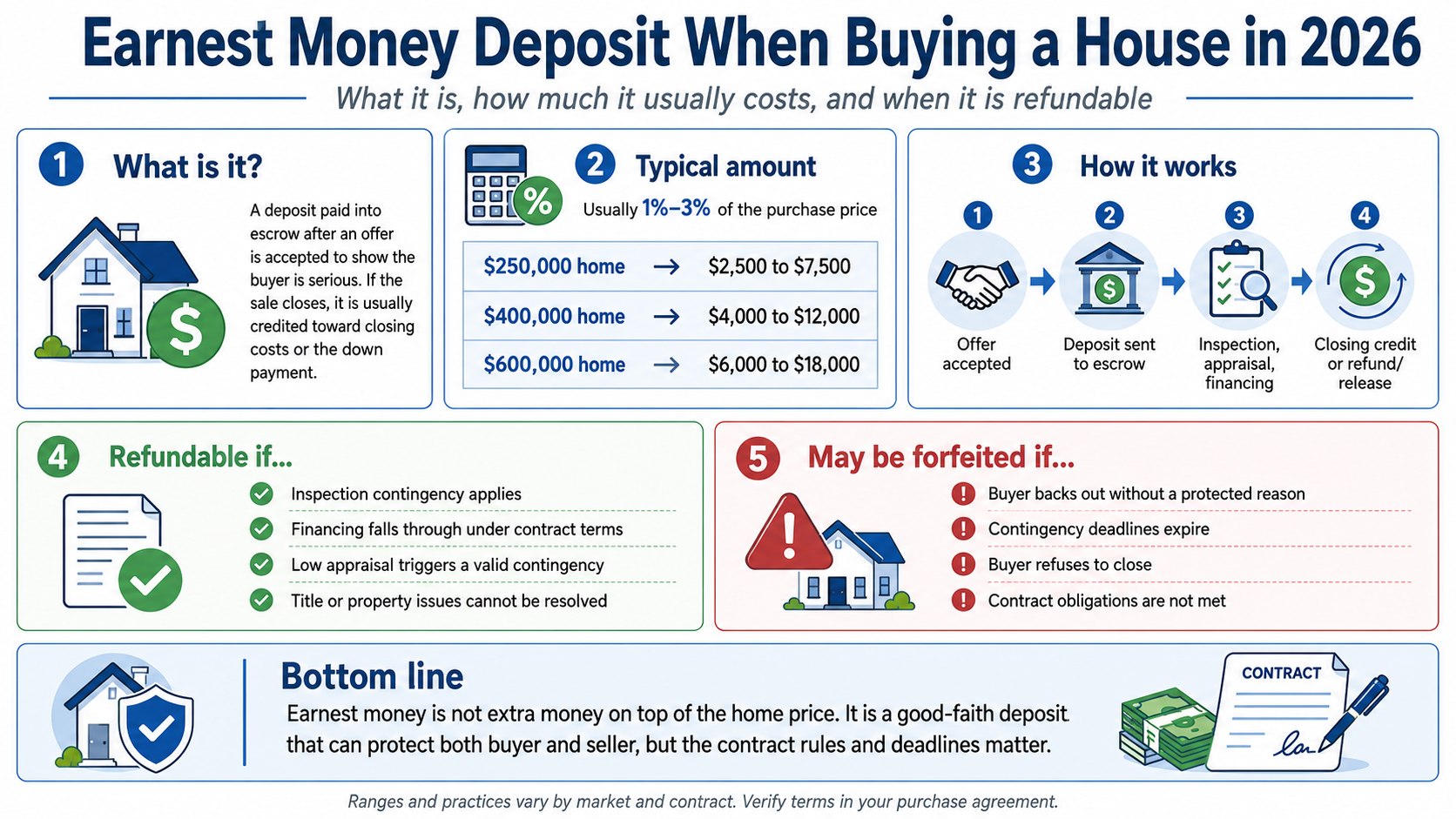

An earnest money deposit is money a homebuyer places in escrow after an offer is accepted to show the seller that the buyer intends to complete the purchase, аs noted by Baltimore Chronicle.

For anyone asking what is earnest money deposit when buying a house, the practical answer is simple. The money is usually credited toward the down payment or closing costs if the sale closes. It may be refunded when a protected contingency applies, but the buyer can lose it by breaking the contract without an allowed reason.

Key takeaways

- Earnest money commonly equals 1% to 3% of the purchase price, although local practices and competition affect the amount.

- The purchase agreement determines whether the deposit is refundable. There is no universal nationwide cancellation rule.

- Buyers should confirm the escrow holder, payment deadline, contingencies, and release procedure before transferring money.

In plain English

Earnest money works like a reservation deposit with contract conditions attached. The buyer asks the seller to stop considering other offers, while the seller asks for financial proof that the buyer will not walk away casually.

Consider a buyer whose $400,000 offer is accepted with a $6,000 deposit. The money normally goes to a title company, escrow company, real estate brokerage, or attorney named in the purchase agreement. It does not usually become an additional charge on top of the home price.

The deposit is held during the period between contract acceptance and closing. Baltimore Chronicle’s guide to how escrow works when buying a house explains the role of the neutral third party that controls the funds and follows the written purchase agreement.

If the transaction closes, the $6,000 appears as a credit in the final accounting. It may reduce the cash needed for the down payment, closing costs, or both.

If the transaction ends, the contract controls who receives the money. A buyer who cancels under a valid inspection, financing, appraisal, title, or home-sale contingency may be entitled to a refund. A buyer who changes plans after the protected periods expire may lose the deposit.

Earnest money is also called a good faith deposit on a house. It is different from a mortgage down payment, an option fee, lender charges, and the mortgage escrow account used after closing to pay property taxes and homeowners insurance.

How it actually works

The deposit process begins when the seller accepts an offer containing an earnest money provision. That provision should state the amount, payment deadline, escrow holder, permitted payment method, and conditions for releasing the money.

The buyer then delivers the funds according to the contract. Deadlines vary by state and contract form. Some contracts require payment within a few days after the agreement becomes effective, while others set a specific calendar date.

The escrow holder deposits the money into a trust or escrow account and keeps it separate while the transaction proceeds. Buyers should obtain written confirmation showing the amount received, property address, transaction parties, and deposit date.

During the contract period, the buyer completes inspections, mortgage underwriting, appraisal, title review, insurance arrangements, and other required steps. The deposit remains in escrow unless the parties authorize its release or another contract procedure applies.

At closing, the deposit is listed as money the buyer has already paid. It becomes one part of the broader cash-to-close calculation, which may also include lender fees, title charges, prepaid property taxes, homeowners insurance, and transfer costs. A separate Baltimore Chronicle breakdown explains what closing costs on a house include in 2026.

The process usually follows five steps:

- The buyer and seller sign a purchase agreement that identifies the earnest money terms.

- The buyer sends the deposit to the named escrow holder before the contractual deadline.

- The escrow holder safeguards the money while inspections, appraisal, financing, and title work proceed.

- The deposit is credited at closing or released after a valid termination or written settlement.

- A dispute may delay release until both parties agree or a legal process determines entitlement.

What is earnest money deposit when buying a house worth?

There is no single federal percentage required for every residential purchase. A common range is 1% to 3% of the accepted price, although buyers should verify local expectations before submitting an offer.

On a $300,000 home, that range equals approximately $3,000 to $9,000. On a $550,000 property, it equals approximately $5,500 to $16,500. These figures illustrate the percentage calculation rather than a mandatory amount.

| Accepted home price | 1% deposit | 2% deposit | 3% deposit |

|---|---|---|---|

| $250,000 | $2,500 | $5,000 | $7,500 |

| $400,000 | $4,000 | $8,000 | $12,000 |

| $600,000 | $6,000 | $12,000 | $18,000 |

| $850,000 | $8,500 | $17,000 | $25,500 |

The appropriate amount depends on the local housing market and the strength of the offer. Sellers in competitive areas such as Northern Virginia, suburban Maryland, Austin, Los Angeles, or parts of Florida may expect a larger deposit than sellers in slower markets.

A higher deposit can strengthen an offer because more buyer money is exposed if the contract is breached. It does not automatically make an offer safer. Buyers should not offer more than they can afford to have tied up or potentially disputed.

Real estate brands such as Zillow, Redfin, Realtor.com, and local Multiple Listing Services may provide market context, but they do not set the required deposit. The amount remains negotiable unless a builder, auction, or specialized sales program imposes specific terms.

The earnest money amount should also be evaluated alongside the down payment. Baltimore Chronicle’s guide to down payment requirements for US homebuyers in 2026 compares conventional, FHA, VA, and other common financing paths.

When earnest money is refundable

An earnest money refund usually depends on whether the buyer followed a specific contract clause and met its deadline. Having a problem with the property or mortgage does not guarantee a refund when notice is late or the relevant contingency was waived.

Inspection contingency

An inspection contingency may allow the buyer to terminate, request repairs, or renegotiate after reviewing the home inspection. The buyer must act within the inspection period and deliver notice in the form required by the contract.

Problems involving a roof, foundation, electrical system, plumbing, mold, or major HVAC equipment can affect the decision. A defect does not automatically release the deposit when the contract lacks an inspection right.

A buyer might receive the deposit back after discovering a major structural issue if the contract permits cancellation during the inspection period. The same buyer could lose that protection by allowing the deadline to pass without sending proper notice.

Financing contingency

A mortgage contingency may protect the buyer when financing cannot be obtained despite a timely and good-faith application. The clause may contain deadlines for the loan application, lender approval, and notice of denial.

Preapproval from lenders such as Bank of America, Chase, Wells Fargo, Rocket Mortgage, or a local credit union is not a final loan commitment. Changes in employment, debt, credit, property eligibility, or underwriting findings can still affect approval.

Mortgage denial does not automatically guarantee the return of earnest money. The buyer may need to provide a lender rejection letter, show that the application was submitted on time, and terminate before the financing deadline.

Appraisal contingency

An appraisal contingency can provide options when the appraised value is below the agreed price. The buyer may renegotiate, contribute additional cash, challenge the appraisal, or terminate according to the contract.

Suppose a buyer agrees to pay $450,000, but the lender’s appraisal values the property at $425,000. The lender may calculate the mortgage using the lower value, leaving the buyer to cover a larger gap in cash.

Without adequate protection, a low appraisal may not excuse performance. Buyers considering an appraisal gap should understand how much additional money they could be required to bring to closing.

Title and property-related contingencies

A title contingency may apply when the seller cannot provide marketable title or resolve liens, ownership claims, boundary issues, or other recorded defects.

Separate provisions may address homeowners association documents, insurance availability, septic systems, wells, flood-zone findings, or the sale of the buyer’s current home.

A refundable deposit is not the same as an automatically refunded deposit. The buyer must use the correct contract right before its deadline and document the termination.

When a buyer can lose the deposit

The buyer may forfeit the house deposit before closing after defaulting on contractual obligations. Common examples include cancelling for personal preference after contingencies expire, missing financing deadlines, refusing to close without a protected reason, or failing to deliver required documents.

A change of mind is usually not a contractual contingency. Concerns about furniture placement, commute time, neighborhood preference, or finding another property at a better price may not provide a valid reason to cancel.

The buyer may also create a default by taking financial actions that damage mortgage approval. Opening a new auto loan, financing expensive furniture, changing jobs, or making large undocumented bank deposits before closing can disrupt underwriting.

A seller does not always receive the money immediately after alleging default. Many escrow holders require matching written instructions from the buyer and seller before releasing disputed funds.

When the parties disagree, mediation, arbitration, interpleader, litigation, or another state-specific procedure may follow. The escrow company generally does not decide which party is legally correct based only on competing phone calls or emails.

Buyers should avoid wiring funds from instructions received only by email. Real estate transactions are frequent targets for wire fraud. The title company or settlement provider’s phone number should be verified independently before money is sent.

Use this checklist before delivering the deposit:

- Confirm the exact amount and payment deadline.

- Identify the licensed escrow, title, brokerage, or attorney account receiving the money.

- Verify wiring instructions through a trusted phone number.

- Read every contingency and record its expiration date.

- Ask whether the deposit becomes nonrefundable at a particular stage.

- Keep receipts, notices, inspection reports, lender letters, and signed amendments.

- Confirm how a cancellation notice must be delivered.

- Review unusual or nonrefundable terms with a real estate attorney.

Who it matters to in 2026

First-time buyers with limited cash

A first-time buyer may need money for earnest money, inspections, appraisal charges, moving expenses, closing costs, and reserves within the same several-week period.

Although the deposit is normally credited at closing, the cash becomes unavailable while held in escrow. A buyer with $20,000 in accessible savings may struggle if $8,000 is deposited before inspection bills and lender charges become due.

Mortgage lenders may ask where the deposit funds came from. Bank statements, gift documentation, transfer records, or proof of the original check may be required during underwriting.

Borrowed or undocumented earnest money can create financing problems. Buyers should discuss the source of funds with the lender before moving money between accounts.

Buyers competing for a limited number of homes

A larger earnest money amount may make an offer more credible without increasing the purchase price. It can also increase the buyer’s financial exposure, especially when inspection or appraisal protections are shortened or waived.

Price, contingencies, closing date, financing strength, and seller concessions should be evaluated together. A $15,000 deposit does not compensate for a loan structure the seller considers uncertain, and a smaller deposit does not necessarily weaken an otherwise clean offer.

Buyers should distinguish between raising the deposit and making part of it nonrefundable. A larger refundable deposit may carry less risk than a smaller deposit that the contract allows the seller to keep immediately.

New-construction buyers

Builders may use deposit schedules that differ from standard resale transactions. A buyer might owe an initial amount when signing and additional deposits after selecting structural changes, cabinets, flooring, appliances, or other upgrades.

Deposits for custom options may become nonrefundable because the builder cannot easily resell personalized materials. The contract may also treat cancellation, financing failure, construction delays, and appraisal shortages differently from a standard resale agreement.

Buyers should ask when each payment becomes nonrefundable and whether the deposit is protected if the builder misses a completion deadline. Verbal assurances from a sales representative should not replace written contract language.

Common myths

- Myth: Earnest money is the down payment. It is an earlier deposit that may later be credited toward the down payment or closing costs.

- Myth: Buyers always receive it back after cancelling. Refund rights depend on the signed contract, deadlines, contingencies, and reason for termination.

- Myth: The seller holds the buyer’s check. A neutral title company, escrow company, attorney, or brokerage commonly holds the funds.

- Myth: Every buyer must pay 3%. The deposit is negotiable, and local customs vary across states and metropolitan areas.

- Myth: Mortgage denial guarantees a refund. The buyer must have an effective financing contingency and comply with its application and notice requirements.

Frequently asked questions

How soon is earnest money due after an offer is accepted?

The deadline appears in the purchase agreement and can range from the same day to several business days after acceptance. State forms differ, so the buyer should rely on the signed contract rather than a general national rule.

Does earnest money reduce the amount due at closing?

Yes. When the transaction closes, the deposit is generally credited to the buyer. The final Closing Disclosure should show it as money already paid and include it in the calculation of cash needed to close.

Can earnest money be paid with a personal check?

Payment methods depend on the escrow holder and contract. Personal checks, cashier’s checks, electronic transfers, and wire transfers may be accepted, although a company may require collected funds by a certain deadline.

Who receives the interest earned on earnest money?

Many short residential transactions use non-interest-bearing escrow accounts. When funds enter an interest-bearing account, the contract, escrow agreement, tax documentation, and applicable state rules determine how the interest is handled.

Can the seller keep more than the earnest money?

Possibly. Some contracts treat the deposit as liquidated damages and limit the seller to that remedy, while others preserve additional remedies. The wording and enforceability vary by state.

How long does an earnest money refund take?

An uncontested refund may be processed after the escrow holder receives all required signed instructions. A disputed refund can take much longer because the holder may be unable to release the funds until the parties settle or complete the applicable legal procedure.

Earlier we wrote about How to Expedite a Passport in USA 2026: Fees, Appointments, and Processing Times