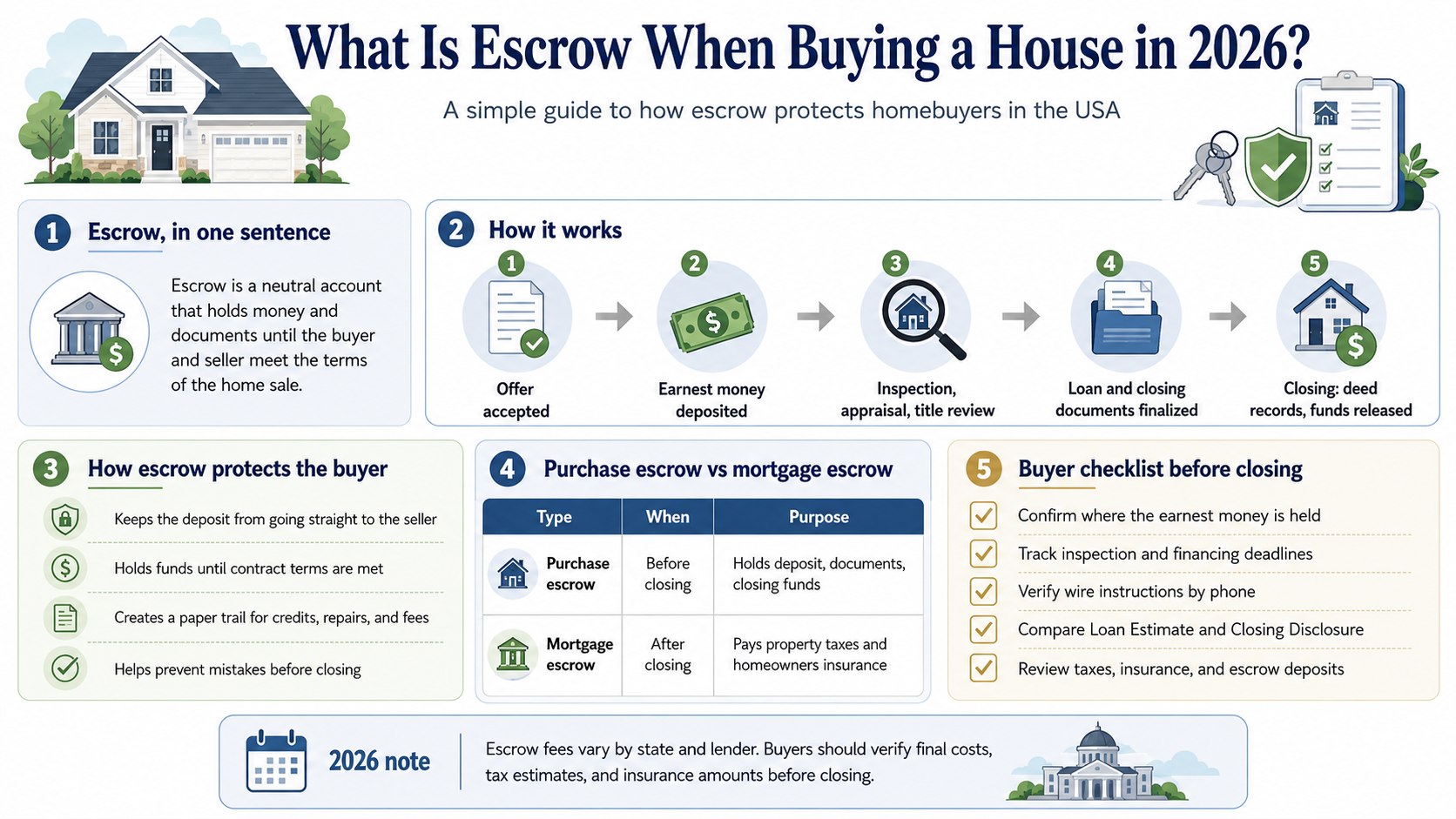

Escrow is a neutral holding arrangement where money, documents, or property-related funds sit with a third party until both the buyer and seller meet the terms of a home purchase, аs noted by Baltimore Chronicle.

If you are asking what is escrow when buying a house, the practical answer is this: escrow helps keep your deposit from going straight to the seller before closing, gives the transaction a controlled process, and helps make sure taxes, insurance, title issues, and agreed repairs are handled before money changes hands permanently.

Key takeaways

- Escrow protects the buyer by holding earnest money until contract conditions are satisfied or the deal legally closes.

- Mortgage escrow is different: it collects monthly amounts for property taxes, homeowners insurance, and sometimes flood insurance.

- In 2026, buyers should review escrow lines on the Closing Disclosure before signing, especially in high-tax states.

In plain English

Think of escrow like a referee holding the ball before a game-deciding play. The buyer does not hand the money directly to the seller, and the seller does not hand over clear ownership without proof that the buyer can close.

In a typical US home purchase, an escrow company, title company, real estate attorney, or settlement agent holds the buyer’s earnest money deposit. That deposit might be $2,000 on a modest home, 1% of the purchase price in many markets, or much more in competitive areas such as California, Texas, Florida, New York, or Maryland.

The same word also appears after closing. A mortgage lender such as Chase, Wells Fargo, Rocket Mortgage, Bank of America, or a local credit union may set up a mortgage escrow account to collect property taxes and insurance with the monthly payment.

Those two uses are connected but not identical. Purchase escrow protects the transaction before closing. Mortgage escrow helps manage recurring bills after the buyer becomes the homeowner.

What is escrow when buying a house?

Escrow when buying a house is the legal and financial middle space between an accepted offer and a completed sale. It starts after the purchase agreement is signed and usually ends at closing, when the deed records and funds are released.

The buyer’s deposit is usually the first item placed into escrow. The seller can see that the buyer has real money at stake, while the buyer keeps protection if the contract allows cancellation because of inspection problems, financing denial, appraisal issues, or title defects.

The escrow holder does not decide whether a house is a good deal. The escrow holder follows written instructions in the purchase contract, lender documents, and state-specific closing rules.

For a buyer, the core protection is simple: the seller cannot just take the deposit because negotiations changed. If the buyer cancels under a valid contingency, the contract usually controls how the money is returned.

Escrow is also where closing funds are coordinated. Down payment money, lender funds, seller payoff amounts, county recording fees, transfer taxes, title insurance premiums, and prorated property taxes all flow through the settlement process.

Buyers who are still planning the full purchase path can use Baltimore Chronicle’s guide on how to buy a house in the USA in 2026 before signing an offer.

How it actually works

The escrow process usually begins when the seller accepts the buyer’s offer. The signed purchase agreement names the escrow holder or settlement agent, then sets deadlines for inspections, financing, appraisal, title review, and closing.

The buyer sends the earnest money deposit according to the contract instructions. In 2026, buyers should be cautious with wire instructions because real estate wire fraud remains a known risk; confirm instructions by calling a verified phone number from the title company, escrow company, or attorney.

The title company or attorney searches ownership records, liens, unpaid taxes, easements, and other title issues. If the seller has an existing mortgage, the settlement agent requests payoff information so that the seller’s loan can be paid from closing proceeds.

The lender prepares final loan documents and provides a Closing Disclosure. The Consumer Financial Protection Bureau says lenders must provide the Closing Disclosure at least three business days before scheduled closing, giving buyers time to check loan terms, projected payments, and closing costs.

At closing, the buyer signs the mortgage documents, the seller signs transfer documents, the lender sends loan funds, and the settlement agent records the deed with the county. After recording, escrow releases funds to the seller, real estate brokers, tax authorities, insurance providers, and other parties listed on the final settlement statement.

Purchase escrow vs mortgage escrow

| Type of escrow | When it applies | What it holds | How it protects the buyer |

|---|---|---|---|

| Purchase escrow | After offer acceptance and before closing | Earnest money, closing funds, signed documents | Prevents premature release of money before contract terms are met |

| Mortgage escrow account | After closing, during mortgage repayment | Monthly tax and insurance reserves | Helps avoid missed property tax or insurance bills |

The CFPB describes a mortgage escrow account as an account a lender or servicer uses to pay property-related expenses such as property taxes, insurance premiums, and flood insurance when applicable. Buyers can review the federal explanation at the CFPB escrow account guide.

How escrow protects the buyer

Escrow does not make a bad contract safe, but it gives the buyer a structured place to enforce the contract. The biggest protection is control over timing: money is not released until agreed conditions are met.

For example, a buyer in Baltimore may place a $7,500 deposit on a $375,000 rowhome. If the inspection contingency allows cancellation after discovering serious foundation damage, escrow instructions can keep the deposit from being released to the seller automatically.

Escrow also creates a paper trail. Buyers can compare the purchase contract, loan estimate, Closing Disclosure, title commitment, inspection repair addendum, and final settlement statement. That matters when a charge appears twice or a seller credit is missing.

The protection is strongest when the buyer understands the deadlines. A missed inspection deadline or expired financing contingency can change who has the stronger claim to the earnest money.

For more context on cash needed at settlement, Baltimore Chronicle has a separate guide to closing costs on a house in the USA in 2026. Buyers comparing loan readiness can also review how to get pre-approved for a mortgage in the USA in 2026.

Escrow is not a substitute for reading the purchase agreement. It is the mechanism that follows the agreement once everyone signs.

What escrow may cost in 2026

Escrow costs vary by state, county, purchase price, title company, and whether the closing uses an attorney. In many 2026 US transactions, escrow or settlement fees may range from a few hundred dollars to more than $2,000, but buyers should verify the actual amount on the Loan Estimate and Closing Disclosure.

Some states use title companies heavily, while others rely more on closing attorneys. California buyers often see escrow companies as a standard part of the transaction, while buyers in parts of New York, Massachusetts, Georgia, and South Carolina may work closely with real estate attorneys.

Escrow-related charges can appear under different names. Common labels include settlement fee, escrow fee, closing fee, document preparation, courier fee, wire fee, recording fee, title search, lender’s title insurance, owner’s title insurance, tax service fee, and prepaid escrow deposits.

The prepaid escrow deposit is not the same as an escrow service fee. Prepaids are buyer funds placed into the mortgage escrow account at closing so the lender has enough money to pay the first property tax or insurance bill when due.

| Line item | Typical purpose | What to check in 2026 |

|---|---|---|

| Escrow or settlement fee | Pays the company or attorney managing closing | Compare the Loan Estimate with the Closing Disclosure |

| Prepaid homeowners insurance | Funds the first year or initial premium | Confirm the carrier, premium, deductible, and coverage dates |

| Initial escrow deposit | Starts the lender’s tax and insurance reserve | Check property tax estimates, especially after reassessment |

| Title insurance | Protects against covered title defects | Ask whether the owner’s policy is optional or customary locally |

HUD’s housing counseling materials note that closing costs can include loan origination fees, appraisal fees, title insurance, legal fees, real estate professional fees, and prepayments for taxes and insurance. Buyers can review HUD homebuying resources through HUD’s buying a home page.

Who it matters to in 2026

First-time buyers using FHA or low-down-payment loans

First-time buyers often have less room for closing surprises. Escrow matters because the earnest money deposit, repair credits, seller concessions, tax proration, and initial insurance reserves can all affect the cash needed to close.

Low-down-payment borrowers should ask the lender early whether monthly mortgage escrow is required. FHA loans commonly include escrow for taxes and insurance, and conventional lenders may require escrow when the down payment is below a certain threshold.

Buyers still deciding how much cash to reserve can compare escrow with down payment planning in Baltimore Chronicle’s guide on how much down payment for a house in the USA in 2026.

Renters moving into ownership

Renters are used to one monthly housing payment. Homeownership splits that reality into principal, interest, property taxes, insurance, possible HOA dues, maintenance, and utilities.

An escrow account can make the transition easier because tax and insurance bills are spread across monthly payments. The tradeoff is that the monthly mortgage payment can rise if property taxes or insurance premiums increase.

Parents, freelancers, and variable-income buyers

Parents and freelancers often care less about technical closing language and more about cash-flow risk. Escrow can reduce the chance of a large semiannual tax bill arriving at the same time as child care, medical bills, quarterly taxes, or slow client payments.

Variable-income buyers should still keep a separate home reserve. Escrow handles scheduled tax and insurance payments; it does not pay for a broken furnace, roof leak, sewer backup, or surprise HOA special assessment.

Escrow checklist before you close

A buyer does not need to become a real estate lawyer to use escrow well. The safest approach is to check the documents that control the money before signing.

- Confirm where the earnest money deposit is held and when it becomes nonrefundable.

- Match every contingency deadline against the calendar, including inspection, appraisal, financing, and title review.

- Verify wire instructions by phone using a known title company, escrow company, or attorney number.

- Compare the Loan Estimate with the Closing Disclosure line by line.

- Check that seller credits, repair credits, and rate buydown credits appear correctly.

- Review prepaid taxes, homeowners insurance, flood insurance, and initial escrow deposits.

- Ask whether property taxes could change after the sale because of reassessment or loss of exemptions.

- Keep copies of the purchase agreement, addenda, title commitment, Closing Disclosure, and final settlement statement.

Common myths

- Myth: Escrow means the seller already has my deposit. Correction: escrow holds the deposit until the contract allows release.

- Myth: Escrow protects me from overpaying. Correction: escrow controls funds and documents, but price negotiation is still the buyer’s job.

- Myth: The escrow company works for the buyer. Correction: the escrow holder is a neutral party following written instructions.

- Myth: Mortgage escrow makes taxes cheaper. Correction: it spreads payments out, but it does not reduce the tax bill.

- Myth: A fixed-rate mortgage means the payment never changes. Correction: principal and interest may stay fixed, while escrow amounts can change with taxes or insurance.

FAQ

Is escrow required when buying a house?

Purchase escrow is standard in many US real estate transactions because it gives both sides a controlled closing process. Mortgage escrow after closing may be required by the lender, loan type, down payment size, or state rules.

Who owns the money in escrow before closing?

The buyer usually has a claim to the earnest money unless the purchase contract gives the seller a right to keep it after a default. The escrow holder does not own the money; it holds the funds under the written agreement.

Can I lose my earnest money deposit?

Yes. A buyer can lose the deposit by breaching the contract, missing deadlines, or canceling without a valid contingency. The exact result depends on the purchase agreement and state law.

Is escrow the same as title insurance?

No. Escrow is the holding and settlement process. Title insurance is a policy that protects against certain covered title problems, such as undisclosed liens or ownership defects.

Why did my mortgage escrow payment increase?

A mortgage escrow payment can rise when property taxes, homeowners insurance, flood insurance, or required reserves increase. The loan’s principal and interest may be fixed while the escrow portion changes.

What should I ask before wiring money to escrow?

Ask for written instructions, then verify them by calling a trusted phone number from the title company, escrow company, or attorney. Do not rely only on email instructions, especially if wiring a down payment or closing funds.

Earlier we wrote about How to Unclog a Shower Drain Without Chemicals Using a Snake and Baking Soda