How to buy a house with bad credit in USA 2026 begins with matching your credit profile to the right mortgage. FHA financing, a qualified co-borrower, and focused credit repair can keep a purchase possible. Most buyers can assess their options within 7 days. Improving the application may take 30–180 days, as the Baltimore Chronicle editorial team notes.

A low score does not automatically block homeownership. The fastest route is to review all 3 credit reports, calculate your complete housing payment, and speak with several FHA-approved lenders. Do this before touring homes or making an offer.

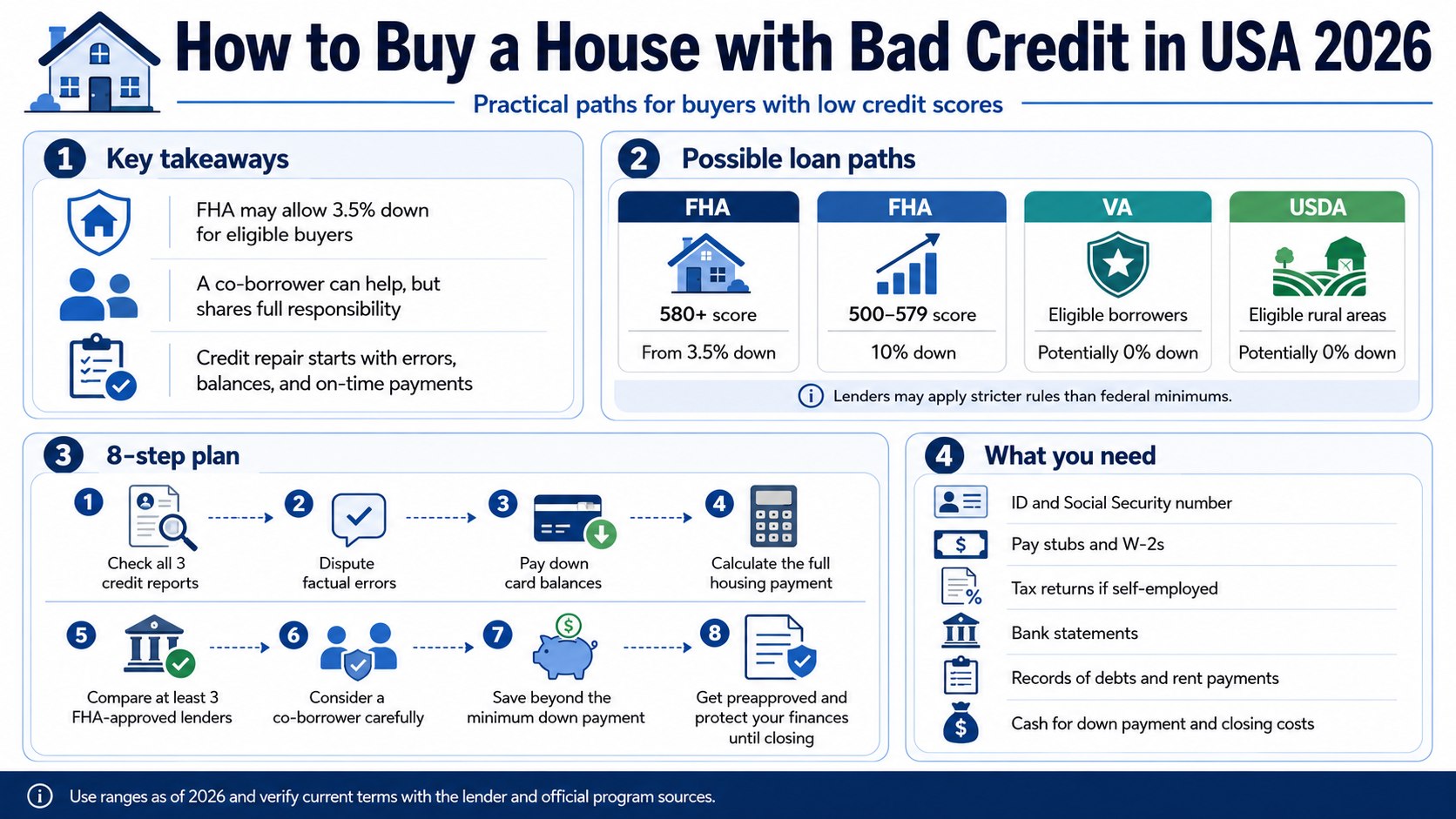

Key takeaways

- FHA financing may allow 3.5% down when the borrower meets the applicable credit and underwriting requirements.

- A co-borrower may add qualifying income, but becomes legally responsible for the entire mortgage debt.

- Credit repair should target reporting errors, high card balances, recent late payments, and undocumented debts.

The minimum program requirement is not a guaranteed approval. Lenders also examine income, employment, savings, recent delinquencies, property condition, and the proposed monthly payment.

What you need before applying

Prepare a complete financial file before contacting mortgage companies. Organized records help the loan officer identify problems before a seller accepts your offer.

- Credit reports from Equifax, Experian, and TransUnion

- Government-issued identification and Social Security number

- Pay stubs covering at least the latest 30 days

- W-2 forms from the previous 2 years

- Federal tax returns when self-employed or using variable income

- Bank and investment statements covering at least 2 months

- Statements for student loans, auto loans, cards, and other debts

- Records showing rent payments and additional income

- Funds for the down payment, inspection, appraisal, and closing costs

- 30–180 days for disputes, balance reductions, and lender review

Keep records for every large bank deposit. An underwriter may request a gift letter, transfer statement, sale receipt, or other proof of origin.

Freelancers and business owners may need profit-and-loss statements. Lenders can also request business bank statements and additional tax documents. Avoid opening new accounts while preparing the file.

Do not finance a car or expensive furniture before closing. A new monthly payment can change your debt-to-income ratio and invalidate the original approval.

How to buy a house with bad credit in USA 2026: compare the available loans

There is no single mortgage definition of “bad credit.” A score accepted by one lender may be rejected by another. Mortgage companies use different risk limits and pricing policies.

Before selecting a program, review Baltimore Chronicle’s guide to the credit score needed to buy a house in 2026. It explains the practical differences between FHA, VA, and conventional credit ranges.

The comparison below shows the main financing paths. These figures describe common program rules and market practices. They do not guarantee approval.

| Mortgage option | Credit position | Possible down payment | Main benefit | Main limitation |

|---|---|---|---|---|

| FHA loan | 580 or higher for maximum financing under standard FHA rules | From 3.5% | Flexible underwriting for imperfect credit | Mortgage insurance and lender overlays apply |

| FHA with a 500–579 score | Potentially eligible under FHA rules | At least 10% | Provides a route for some low-score borrowers | Few lenders approve scores this low |

| Conventional loan | Common planning benchmark near 620 or higher | Often 3%–20% | Private mortgage insurance may later be removed | Weak credit can produce higher borrowing costs |

| VA loan | No universal VA-set minimum score | Potentially 0% | No monthly private mortgage insurance | Only available to eligible borrowers |

| USDA loan | Subject to lender and program review | Potentially 0% | Low upfront requirement for eligible buyers | Income and location restrictions apply |

| Non-occupying co-borrower | Based on the combined application | Depends on the selected loan | May provide additional qualifying income | Both borrowers become responsible for repayment |

FHA is often the first option considered by buyers with damaged credit. The program permits down payments as low as 3.5% for eligible borrowers. The lender may still require a higher score.

A conventional mortgage may become competitive after your score improves. Some programs allow 3% down, but pricing depends heavily on credit, income, property type, and other risks.

VA financing can be powerful for eligible veterans, service members, and qualifying surviving spouses. USDA financing may help income-qualified buyers purchasing eligible rural or suburban properties.

Loan choice should reflect total costs, not only the advertised down payment. Mortgage insurance, lender fees, property taxes, and homeowners insurance can change the result.

Step 1: Pull and review all 3 credit reports

Obtain reports from Equifax, Experian, and TransUnion. Check names, addresses, account limits, payment histories, collections, and reported balances.

This matters because mortgage lenders often review a tri-merge credit report. An error appearing at only 1 bureau may still affect underwriting.

The common mistake is relying on a free consumer score. Mortgage lenders may use different scoring models. Treat app-based scores as monitoring estimates, not approval promises.

Step 2: Dispute factual credit-report errors

Dispute incorrect information with the credit bureau and the company that supplied it. Attach account statements, payment records, identity documents, or court records supporting your position.

A duplicated collection or false late payment can damage both your score and underwriting profile. Correcting verified errors may make the file easier to approve.

Do not dispute accurate negative information only because it is harmful. Unsupported disputes may delay underwriting. Some lenders require active dispute remarks to be resolved before closing.

Step 3: Reduce revolving balances strategically

Prioritize credit cards that are close to their limits. High revolving utilization can signal financial pressure, even when every minimum payment arrives on time.

For example, a $900 balance on a $1,000 limit looks heavily used. Paying that balance down may help more than making an extra payment on a low-rate installment loan.

Keep paid cards open when fees and spending risks are manageable. Closing an account can reduce available credit and increase overall utilization.

Avoid charging mortgage expenses to cards. Inspection, appraisal, moving, and repair bills can quickly rebuild the balances you worked to reduce.

Step 4: Calculate the complete housing payment

Include principal, interest, property taxes, homeowners insurance, mortgage insurance, and homeowners association dues. Add a monthly reserve for repairs and maintenance.

A lender’s maximum approval is not necessarily a safe household budget. Childcare, medical costs, commuting, and irregular freelance income may receive limited attention during underwriting.

State and county costs also matter. A buyer in Florida may face substantial insurance premiums. A buyer in New Jersey may encounter high property taxes.

Do not compare rent with only the mortgage principal and interest. Ownership also brings maintenance, deductibles, utility changes, and emergency repairs.

Step 5: Interview at least 3 FHA-approved lenders

Contact a local bank, a credit union, and a national mortgage company. Ask each lender about score limits, recent late payments, collections, reserves, and debt-to-income policies.

This step matters because lenders can apply overlays above FHA’s basic rules. One company may require a 620 score while another considers a lower score.

Companies such as Chase, Rocket Mortgage, loanDepot, and regional credit unions may evaluate the same borrower differently. Compare written loan estimates when available.

Do not focus only on the quoted interest rate. Examine the annual percentage rate, lender charges, discount points, mortgage insurance, and estimated cash to close.

Step 6: Decide whether a co-signer solves the real problem

A co-signer or non-occupying co-borrower may help when qualifying income is insufficient. The combined file must still satisfy the selected program and lender.

The additional borrower becomes legally responsible for the entire mortgage. Missed payments can damage both credit files. The debt may also limit the co-borrower’s future borrowing.

A co-borrower cannot erase recent delinquencies or make an unaffordable home safe. The strategy is most useful when the main weakness is documented qualifying income.

Discuss ownership, monthly payments, repairs, taxes, insurance, sale proceeds, and exit plans before applying. A written agreement reviewed by a local attorney can prevent disputes.

Step 7: Save beyond the minimum down payment

A $300,000 FHA purchase with 3.5% down requires $10,500 for the down payment. That figure does not include inspection, appraisal, prepaid taxes, insurance, or lender charges.

For a wider cost breakdown, read Baltimore Chronicle’s guide to how much down payment is needed for a house in 2026. It compares FHA, conventional, VA, USDA, and jumbo financing.

Your cash plan should cover several categories:

- Required down payment

- Earnest money deposit

- Home inspection and specialist inspections

- Mortgage appraisal

- Closing costs and prepaid expenses

- Moving and utility deposits

- Immediate repairs or safety work

- Emergency savings after closing

The earnest money deposit is normally credited during settlement. However, the contract determines when that deposit may be refundable.

Closing costs often add a meaningful amount beyond the down payment. The actual figure depends on the lender, location, taxes, title charges, and insurance requirements.

Seller concessions or lender credits can reduce upfront costs. They may carry limits or trade-offs. A lender credit often comes with a higher mortgage rate.

Do not spend every dollar at closing. A failed water heater, plumbing leak, or insurance deductible can create immediate credit-card debt.

Step 8: Get preapproved and protect the application

Apply for preapproval after correcting major errors and reducing expensive balances. Provide complete documents rather than estimates that cannot later be verified.

A preapproval establishes a practical purchase range. It also shows sellers that a lender reviewed your income, assets, credit, and debts.

Readers who need the entire sequence can use Baltimore Chronicle’s step-by-step guide to buying a house in the USA in 2026. It covers budgeting, property searches, offers, inspections, appraisals, and closing.

Preapproval is not final approval. The lender must still examine the selected property and updated financial information.

Until closing, avoid new loans, unexplained bank deposits, missed payments, and expensive card purchases. Lenders may check credit and employment again shortly before settlement.

Troubleshooting common mortgage problems

A rejected application often identifies a specific weakness. Use the lender’s written explanation before applying elsewhere.

- Score below the lender’s minimum: ask whether another FHA lender accepts lower scores or pause for targeted repairs.

- Debt-to-income ratio is too high: reduce monthly debts, lower the purchase price, or document eligible additional income.

- Recent late payments: establish a clean payment period and prepare a factual explanation with supporting records.

- Insufficient cash: investigate gift funds, state assistance, seller concessions, or a less expensive property.

- Self-employment income was reduced: ask which tax-return figures were used and what additional records may qualify.

Do not assume every denial requires a co-signer. The main obstacle may be disputed accounts, insufficient income, unstable employment, recent delinquency, or property condition.

Review the adverse-action notice carefully. Correct factual errors before submitting another application. Ask the loan officer which changes would produce a different decision.

A HUD-approved housing counselor may help explain available programs. Counseling is especially useful when credit problems, limited savings, and debt overlap.

Avoid companies promising guaranteed approval or immediate deletion of accurate credit information. Legitimate lenders and counselors explain risks, conditions, and costs in writing.

FAQ

Can I buy a house with a 500 credit score in 2026?

FHA rules may permit borrowers with scores from 500 through 579 to use 10% down. Many lenders set higher minimums, so available choices may be limited.

What score is needed for a 3.5% FHA down payment?

A score of at least 580 is the standard FHA threshold for maximum financing. Approval still depends on income, debts, payment history, savings, and lender requirements.

Can a co-signer help me qualify with bad credit?

Possibly. A qualified co-borrower may add usable income or strengthen the combined application. That person becomes fully responsible for repayment if payments are missed.

How quickly can credit improve before buying?

Lower card balances may appear after the next reporting cycle. Correcting errors and rebuilding payment history can require 30–180 days or longer.

Should I pay every collection before applying?

Not automatically. Treatment depends on the collection type, amount, loan program, underwriting result, and lender policy. Ask before using money reserved for closing.

Is FHA always cheaper than a conventional mortgage?

No. FHA may offer easier qualification, but mortgage insurance affects the cost. Compare official estimates for both loan types using the same property price.

Earlier we wrote about Commercial Video Editing Service for Business Growth and Brand Trust