A home-buying credit score is the number lenders use to judge how risky it is to approve your mortgage.

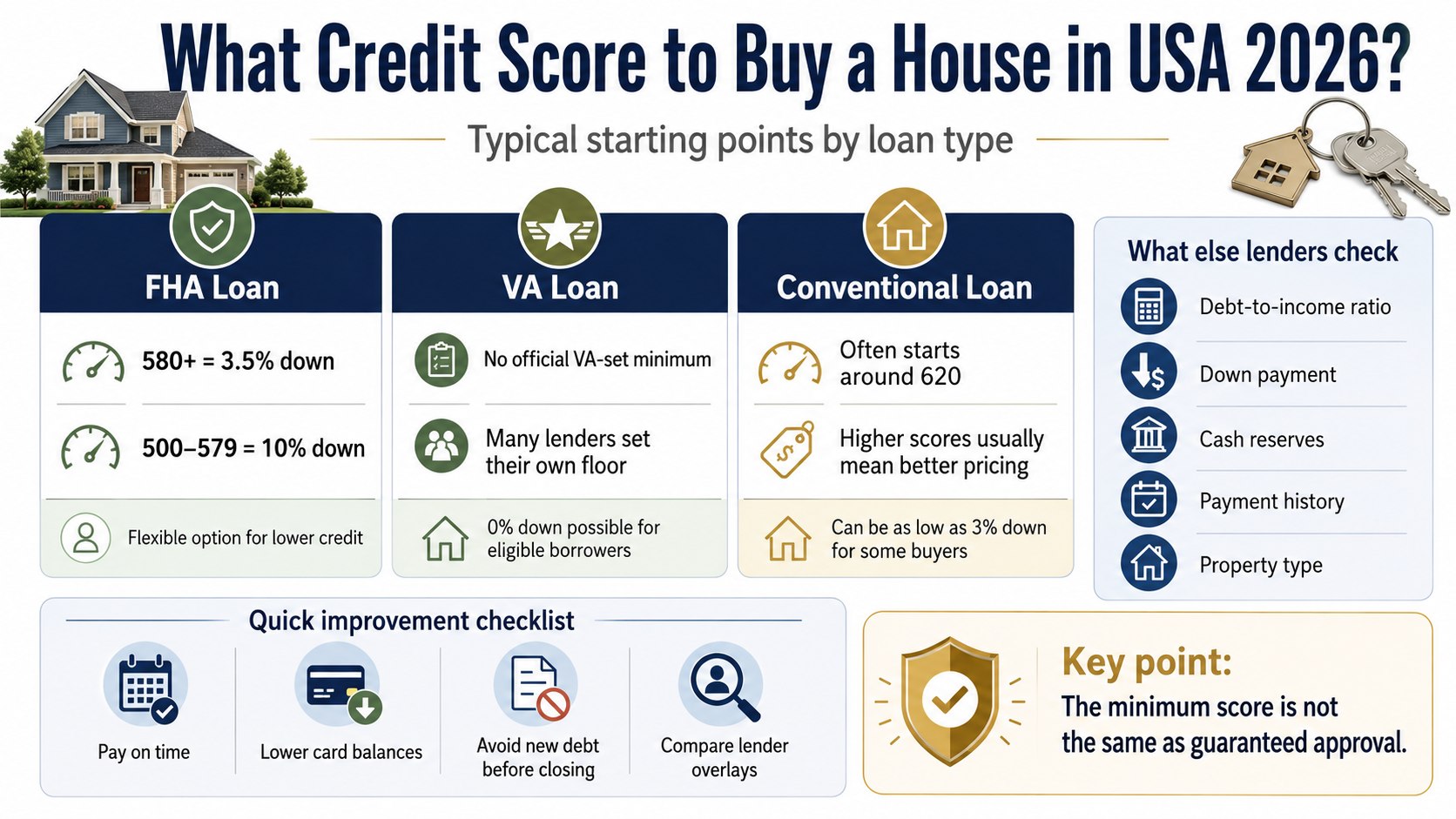

If you are asking what credit score to buy a house in USA 2026, the practical answer is: 580 can work for many FHA buyers with 3.5% down, 500–579 may work for FHA with 10% down, VA has no official VA-set minimum but lenders often set their own floor, and conventional loans commonly start around 620, аs noted by Baltimore Chronicle.

Key takeaways

- FHA is usually the most flexible path if your credit score is below 620 and you have steady income.

- VA loans can be powerful for eligible service members, veterans, and some surviving spouses, but lender rules still matter.

- A higher score can reduce your rate, mortgage insurance cost, and cash needed at closing in many 2026 loan scenarios.

The minimum score is not the same as approval. Lenders also review income, debt-to-income ratio, savings, employment history, property type, and the size of your down payment.

For buyers comparing rent renewal, home prices, and moving costs, the first step is to match the loan type to the score range. A renter in Texas with a 585 score may need a different plan than a freelancer in California with a 660 score and irregular income.

Buyers who are still at the early planning stage can pair this guide with Baltimore Chronicle’s breakdown of how to buy a house in USA 2026, especially if they are comparing preapproval, property search, offer timing, and closing steps.

What credit score to buy a house in USA 2026 by loan type

The score you need depends mostly on whether the loan is FHA, VA, or conventional. FHA loans are insured by the Federal Housing Administration. VA loans are backed by the U.S. Department of Veterans Affairs for eligible borrowers. Conventional loans are not government-insured and are often sold to Fannie Mae or Freddie Mac.

| Loan type | Typical 2026 credit score starting point | Minimum down payment path | Best fit |

|---|---|---|---|

| FHA | 580 for 3.5% down; 500–579 may require 10% down | 3.5% or 10%, depending on score | Borrowers with limited savings or past credit problems |

| VA | No VA-set minimum; lender overlays often apply | 0% down for many eligible borrowers | Eligible veterans, active-duty service members, and qualifying spouses |

| Conventional | Often around 620, depending on automated underwriting | As low as 3% for some first-time buyers | Borrowers with stronger credit, stable income, and lower debt |

HUD says FHA borrowers with a Minimum Decision Credit Score below 500 are not eligible for FHA-insured financing, while FHA’s better-known 3.5% down path generally begins at 580. The official HUD answer is available through HUD’s FHA credit score guidance.

The VA states that it does not require a minimum credit score for VA-backed loans, but lenders may use credit scores to set their own approval standards. The VA explains this in its VA Home Loan Guaranty Buyer’s Guide.

In plain English

Think of your credit score like the first gate at a stadium. A ticket gets you to the entrance, but security still checks your bag before you reach your seat.

A 620 score may get a conventional loan file through the first gate. It does not guarantee approval if your credit cards are maxed out, your income is hard to document, or your bank account has no reserves after closing.

A 580 FHA score can be enough for the low-down-payment path, but the lender still has to believe the monthly payment is manageable. That includes principal, interest, property taxes, homeowners insurance, mortgage insurance, and any HOA dues.

This is why two buyers with the same FICO score can get different answers from Wells Fargo, Chase, Rocket Mortgage, a credit union, or a local mortgage broker. The score opens the conversation; the full file decides the outcome.

How it actually works

Mortgage lenders usually pull a tri-merge credit report from Equifax, Experian, and TransUnion. For many mortgage files, the lender uses the middle score when three scores are available.

For a joint application, the lender may use the lower representative score between the two borrowers. A couple in Florida could have one applicant at 740 and the other at 610, and the lower score may drive pricing or eligibility.

The lender then runs the file through automated underwriting. FHA files may use TOTAL Mortgage Scorecard. Conventional files may go through systems connected to Fannie Mae or Freddie Mac standards. VA files use VA rules plus lender overlays.

The result is not just “approved” or “denied.” The system may require more reserves, a lower debt-to-income ratio, proof of rent history, a larger down payment, or manual underwriting.

Loan pricing comes next. In 2026, a buyer with a 760 score usually has more room to shop for a lower rate than a buyer at 620, all else equal. The exact difference changes with market rates, lender fees, loan size, points, and property type.

Minimum for FHA, VA, and conventional loans

FHA minimum credit score

The most searched number for FHA loan credit score 2026 is 580. That is the common threshold for FHA’s 3.5% down payment option.

Borrowers from 500 to 579 may still be considered for FHA financing with 10% down, but many lenders are stricter than the FHA baseline. A lender can set its own minimum above the FHA floor.

On a $300,000 home, 3.5% down is $10,500 before closing costs. A 10% down payment is $30,000 before closing costs. That difference is why the score threshold matters in a real budget.

Buyers who are close to the FHA threshold should also calculate cash needed upfront. Baltimore Chronicle’s guide on how much down payment for a house in USA 2026 explains how down payment size changes the mortgage path, especially when savings are tight.

VA minimum credit score

The answer for VA loan minimum credit score is different because the VA does not set one national minimum. The lender still evaluates credit history, income, residual income, debts, and payment shock.

Many VA lenders prefer scores around 620, while some may consider lower scores if the borrower has strong compensating factors. Full entitlement can allow 0% down, but that does not remove underwriting.

VA borrowers should ask the lender whether the score rule is a VA rule or a lender overlay. That one question can prevent a qualified borrower from giving up after one denial.

Conventional minimum credit score

The common answer for conventional loan credit score 620 remains a useful planning benchmark. Conventional loans generally reward stronger credit more than FHA because pricing can change significantly by credit tier.

A buyer with 680 may qualify but pay more than a buyer with 740. A buyer under 620 may need to consider FHA, VA if eligible, USDA if the property and income qualify, or more time improving credit.

Conventional loans can become attractive when the buyer has enough credit strength to avoid expensive pricing and enough equity to remove private mortgage insurance later.

Who it matters to in 2026

First-time buyers with thin credit

A first-time buyer may have paid rent for years but used little credit. That can produce a lower score or a limited credit file, even with responsible money habits.

For these buyers, FHA may be more realistic than conventional. Rent payment history, stable employment, and a clean 12-month payment record can help the file.

Renters deciding whether to renew

A renter facing a lease renewal in Maryland, Arizona, or Georgia may be trying to decide whether to buy now or wait six months. The score range can make that decision more concrete.

If the score is 570, the next goal may be reaching 580 and saving 3.5% down. If the score is 615, the next goal may be reaching 620 and comparing FHA with conventional options.

Freelancers and self-employed buyers

Freelancers can have strong income but messy documentation. Lenders usually want tax returns, bank statements, profit-and-loss details, and a stable income pattern.

A higher score can help, but it will not replace income documentation. A 700 score with inconsistent deposits may be harder to approve than a 660 score with clean two-year self-employment income.

What affects approval besides the score

The credit score is only one part of the file. Lenders want to know whether the mortgage payment fits the borrower’s full financial picture.

- Debt-to-income ratio: car loans, student loans, credit cards, child support, and the proposed mortgage payment all matter.

- Down payment: more cash down can reduce lender risk and sometimes offset weaker credit.

- Reserves: money left after closing can help, especially for conventional or self-employed borrowers.

- Payment history: recent late payments can hurt more than old problems that have been resolved.

- Property type: a condo, duplex, manufactured home, or investment property may face stricter rules.

A buyer shopping for a $425,000 home in Phoenix with 5% down may face different underwriting pressure than a buyer looking at a $240,000 home in Cleveland with 10% down. The loan amount, taxes, insurance, and local HOA dues change the monthly payment.

Closing costs also affect approval because lenders check whether the borrower has enough verified funds to finish the purchase. Baltimore Chronicle’s explainer on what closing cost on a house means in USA in 2026 is useful for buyers who already know their target score but still need to estimate cash to close.

Common myths

- Minimum credit score to buy a house means guaranteed approval. Correction: it only means the file may be eligible for review.

- You need a 20% down payment. Correction: FHA, VA, and some conventional programs allow much less for qualified borrowers.

- VA loans are only for perfect-credit borrowers. Correction: VA has no VA-set score minimum, though lenders can add overlays.

- FHA is only for first-time buyers. Correction: repeat buyers can use FHA if they meet program rules.

- A credit repair company can quickly erase accurate negatives. Correction: accurate late payments, collections, and charge-offs usually cannot be deleted just because they hurt.

The practical mortgage question is not “Is my score good?” It is “Which loan type fits my score, savings, income, and timeline?”

How to improve your mortgage position before applying

Small credit changes can matter when a buyer is close to a threshold. Moving from 577 to 582 can affect an FHA down payment path. Moving from 618 to 624 can open conventional conversations.

The highest-impact step is usually lowering credit card utilization. Paying a card from 88% of its limit to below 30% can help many scoring profiles, though the exact result varies.

Buyers should avoid opening store cards, financing furniture, or buying a car before closing. A new monthly payment can damage the debt-to-income ratio even if the credit score barely changes.

A practical preapproval checklist should include:

- Pull credit reports and dispute clear errors before the lender pull.

- Pay all accounts on time for at least the next 90 days.

- Lower revolving balances before statement closing dates.

- Save proof of down payment funds and closing cost reserves.

- Keep job and income documentation organized.

- Ask each lender about overlays, not just program minimums.

- Compare FHA, VA, and conventional estimates on the same purchase price.

FAQ

Can I buy a house with a 580 credit score in 2026?

Yes, a 580 score can fit FHA’s 3.5% down path if the rest of the file qualifies. Lenders may still require stronger income, fewer recent late payments, or additional documentation.

Can I buy a house with a 500 credit score?

FHA rules may allow 500–579 with 10% down, but many lenders do not approve loans that low. A borrower in this range should expect stricter review and fewer lender options.

What credit score is needed for a conventional mortgage?

Around 620 is the common planning benchmark for home loan credit score requirements on conventional mortgages. Higher scores can improve pricing and make approval easier when debt or savings are tight.

Does VA require a credit score?

The VA does not set a national minimum credit score for VA-backed home loans. Lenders can set their own minimums, so a denial from one lender does not always mean the borrower is ineligible for VA financing.

Is 700 a good credit score to buy a house?

A 700 score is generally strong enough to compare FHA, VA if eligible, and conventional options. The final answer still depends on income, debt, down payment, property taxes, insurance, and the lender’s underwriting system.

Should I improve my score before buying?

Improving the score can help if the buyer is close to a cutoff such as 580, 620, 680, or 740. Waiting makes the most sense when a realistic credit improvement could reduce the rate, down payment pressure, or mortgage insurance cost.

Earlier we wrote about French Door vs Side by Side Fridge 2026: Best Refrigerator for Space, Energy and Price