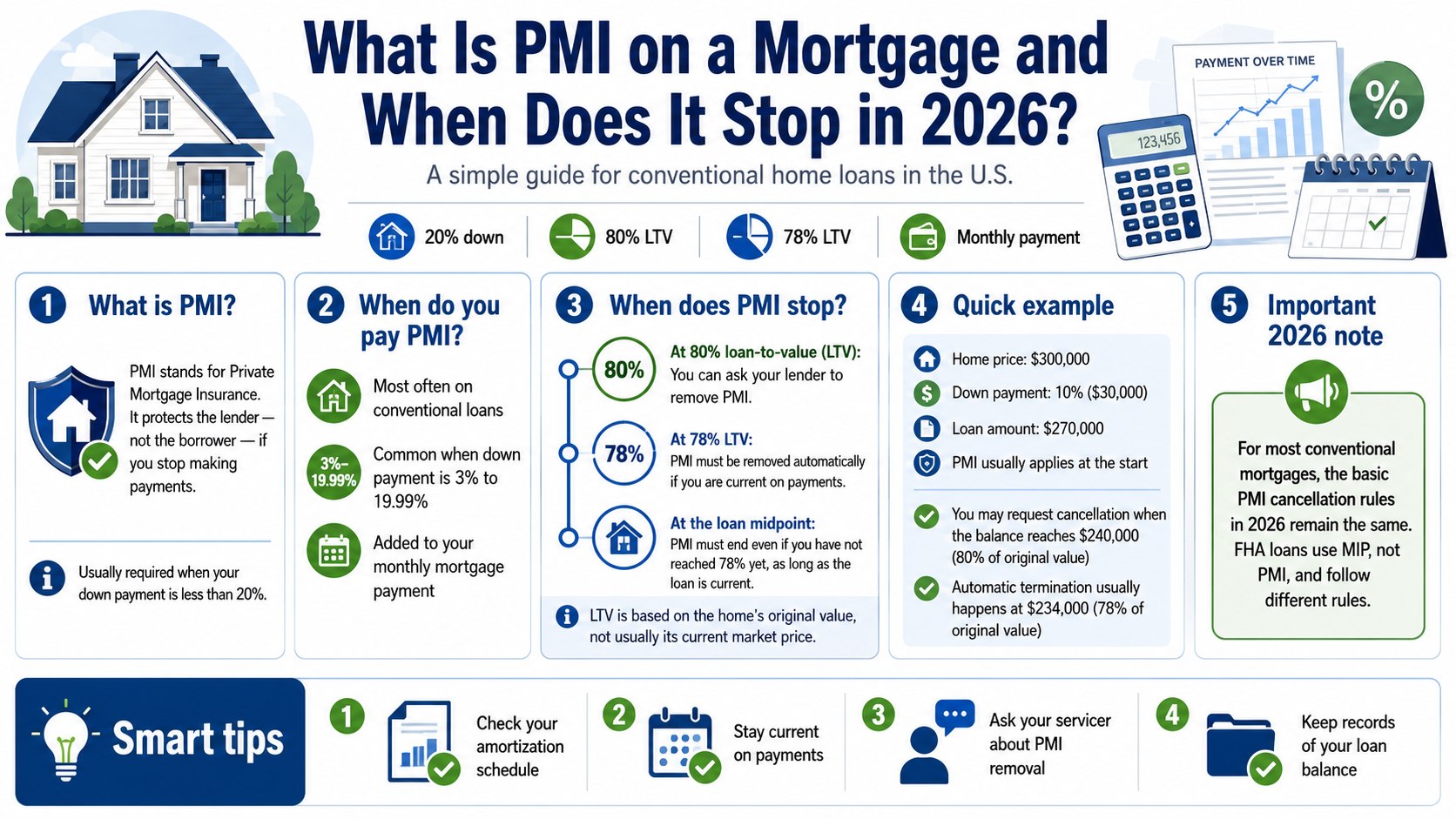

What is PMI on a mortgage and when does it stop? PMI is insurance that protects a conventional mortgage lender when a buyer makes a small down payment. It often applies below 20% equity. A borrower can generally request cancellation at 80% loan-to-value, while automatic termination usually occurs at 78%, as noted by the Baltimore Chronicle.

Homeowners should not assume the charge will disappear as soon as local property prices rise. The cancellation date depends on the loan type, original property value, principal balance, payment record, and mortgage servicer’s rules. Checking those details can remove an unnecessary monthly cost without refinancing the mortgage.

Key takeaways

- PMI usually applies to conventional mortgages when the buyer begins with less than 20% equity.

- Borrowers may request PMI cancellation at 80% LTV after meeting payment and property requirements.

- Automatic PMI termination generally occurs at 78% LTV when the mortgage is current.

The 80% and 78% thresholds serve different purposes. At 80%, the homeowner normally submits a request. At 78%, the servicer generally has a duty to terminate qualifying PMI automatically.

A borrower who has made extra principal payments may reach the request threshold earlier than the original schedule suggests. However, cancellation is not guaranteed until every applicable requirement has been satisfied. The mortgage statement and original PMI disclosure should provide the starting information.

In plain English

Think of PMI as a safety net purchased by the borrower for the lender. It does not make mortgage payments after job loss, illness, or disability. It reduces part of the lender’s potential loss if the borrower defaults and the home enters foreclosure.

Lenders face more risk when a buyer contributes only 3%, 5%, or 10% of the purchase price. There is less homeowner equity available to absorb a loss if the property must be sold. Private mortgage insurance allows lenders to approve some conventional mortgages without requiring a full 20% down payment.

Consider a buyer purchasing a $400,000 home in Maryland. A 10% down payment equals $40,000, leaving a $360,000 mortgage. The starting loan-to-value ratio is 90%, so the lender will usually require PMI.

The monthly premium varies by borrower and loan. Credit score, down payment, property type, occupancy, insurer, and loan term can all affect the price. Freddie Mac gives a broad estimate of about $30 to $150 monthly for every $100,000 borrowed. Actual 2026 quotes should always be confirmed with the lender.

How it actually works

Most borrowers pay PMI as part of their monthly mortgage bill. The charge may appear separately beside principal, interest, taxes, homeowners insurance, and escrow items. Some lenders offer single-premium, split-premium, or lender-paid mortgage insurance instead.

Lender-paid PMI does not mean the insurance is free. The lender may recover the cost through a higher interest rate or another pricing adjustment. That structure can make cancellation more difficult because there may be no removable monthly PMI line.

Mortgage insurers include companies such as MGIC, Arch MI, Radian, Enact, and National MI. However, homeowners usually communicate with the mortgage servicer rather than the insurer. The servicer collects payments and processes removal requests.

The main calculation is the loan-to-value ratio, commonly called LTV. Divide the unpaid principal by the relevant property value. Multiply the result by 100.

For example, a $320,000 balance against an original property value of $400,000 creates an 80% LTV. That is the standard request threshold for many conventional mortgages covered by federal cancellation rules.

| Mortgage position | LTV based on original value | Typical result |

|---|---|---|

| PMI commonly required | Above 80% | The borrower usually pays mortgage insurance on a conventional loan |

| Cancellation request | 80% | The homeowner may request removal after meeting the required conditions |

| Automatic termination | 78% | The servicer generally removes qualifying PMI when the loan is current |

| Final termination safeguard | Amortization midpoint | PMI generally ends after the scheduled midpoint once the mortgage becomes current |

These thresholds usually rely on the home’s original value, not its estimated 2026 market price. For a purchase, original value generally means the lower of the contract price or the appraisal used at closing.

A refinanced mortgage normally uses the value established during that refinance. Rising neighborhood prices may support an earlier request under separate current-value rules. They do not automatically change the federal scheduled termination date.

Homeowners should therefore calculate LTV both ways before contacting the servicer.

What is PMI on a mortgage and when does it stop under federal rules?

The federal Homeowners Protection Act establishes cancellation and termination protections for many residential mortgages with borrower-paid PMI. It generally covers qualifying conventional loans on a borrower’s principal residence. FHA, VA, USDA, lender-paid, and some high-risk mortgages follow different rules.

A homeowner may generally request cancellation when the scheduled principal balance reaches 80% of the original property value. The request should be submitted in writing. The servicer may require a satisfactory payment history and evidence that the property has not lost value.

The home must also be free from certain subordinate liens. A home equity loan or second mortgage can affect eligibility because it changes the lender’s risk position. The servicer may order an appraisal or another approved valuation at the borrower’s expense.

Automatic termination normally occurs when the scheduled balance reaches 78% of original value. The borrower must be current. If the mortgage is delinquent on the scheduled termination date, removal may be delayed until the account becomes current.

Federal law also provides a final termination safeguard. PMI generally ends after the loan reaches the midpoint of its original amortization schedule, provided the borrower is current. For a 30-year mortgage, that point normally arrives after 15 years.

“You have the right to request that your servicer cancel PMI when you have reached the date when the principal balance is scheduled to fall to 80% of the original value of your home.” — Consumer Financial Protection Bureau.

How to remove PMI before automatic termination

Extra principal payments can help a borrower reach 80% LTV earlier. Home appreciation may also support removal before the scheduled date. However, the servicer can apply different requirements when the request relies on the property’s current value.

A house purchased for $350,000 might later appraise for $450,000. If the remaining balance is $330,000, current-value LTV would be about 73.3%. Original-value LTV would still be about 94.3%, producing a very different result.

Borrowers should use the following process before paying for an appraisal:

- Confirm that the loan is conventional and includes borrower-paid PMI.

- Find the original property value in the closing or appraisal documents.

- Check the unpaid principal balance on the latest mortgage statement.

- Calculate LTV using both original and estimated current value.

- Ask the servicer for its written PMI removal requirements.

- Confirm which appraisal or valuation provider the servicer accepts.

- Submit the request and retain copies of every document.

Do not order an independent appraisal before contacting the mortgage servicer. The company may accept only a valuation ordered through its approved system. An outside report could cost several hundred dollars and still be rejected.

Ask about the required LTV, loan seasoning, payment history, and valuation fee first. Major renovations may support a current-value request, but basic maintenance usually does not. Continue paying the full billed amount until the servicer confirms cancellation.

Borrowers preparing to purchase can reduce later surprises by reviewing the Baltimore Chronicle guide on how to get pre-approved for a mortgage in the USA in 2026. It explains the income records, credit checks, asset documents, and lender review involved before an offer is made.

Who it matters to in 2026

Recent buyers with a small down payment

A first-time buyer may choose a conventional mortgage with 3% or 5% down instead of postponing the purchase. PMI becomes part of the monthly housing cost. Buyers should compare principal, interest, taxes, homeowners insurance, HOA dues, and mortgage insurance together.

For a detailed affordability comparison, Baltimore Chronicle explains how much income is needed to buy a $400,000 house in the USA in 2026. The guide shows why the same sale price can produce different payment burdens.

Homeowners whose property value has increased

Owners in Maryland, Florida, Texas, Arizona, or California may have gained equity through appreciation. That gain does not automatically remove PMI. The borrower must ask whether the servicer permits cancellation based on current value.

Online estimates from Zillow, Redfin, or Realtor.com can provide an initial reference. They are not guaranteed substitutes for an approved appraisal. Recent comparable sales and the home’s condition will usually carry more weight.

Owners considering refinancing

A refinance can remove PMI when the new conventional mortgage remains at or below 80% LTV. However, the borrower may face lender fees, title charges, appraisal costs, and a different interest rate. Replacing a low-rate mortgage solely to eliminate PMI can be expensive.

Direct cancellation should be checked first. It may remove the premium without resetting the loan term.

Consumers still planning a purchase can use Baltimore Chronicle’s complete guide on how to buy a house in the USA in 2026 to compare budgeting, pre-approval, inspections, closing, and ongoing costs.

PMI is not FHA mortgage insurance

Many borrowers use “PMI” as a general name for every mortgage insurance charge. The term technically applies to private insurance on conventional mortgages. FHA mortgages use an upfront and annual mortgage insurance premium, usually called MIP.

For many FHA loans with case numbers assigned on or after June 3, 2013, annual MIP lasts 11 years when the original LTV was 90% or lower. It generally lasts for the mortgage term when the original LTV exceeded 90%. Refinancing into a conventional mortgage may be required to remove it.

VA-backed mortgages do not require monthly PMI or FHA-style annual MIP. The Department of Veterans Affairs may instead charge a one-time funding fee. Eligible veterans, service members, or surviving spouses may qualify for an exemption.

USDA guaranteed mortgages use upfront and annual guarantee fees. Those charges do not follow the conventional 80% and 78% cancellation rules. Borrowers should identify the exact loan program before estimating a removal date.

Common myths

PMI misinformation often comes from treating every loan and every equity calculation alike:

- “PMI ends after the home gains 20% in value.” Appreciation may help, but approved valuation and seasoning rules can apply.

- “PMI protects the homeowner.” It protects the lender against part of a default-related loss.

- “The lender must cancel PMI at 80%.” The homeowner normally requests removal and proves eligibility at 80%.

- “Every mortgage uses the 78% rule.” FHA, VA, USDA, and lender-paid structures operate differently.

- “Refinancing is always required.” Many conventional borrowers can remove PMI directly through their servicer.

Start by checking the Closing Disclosure and original PMI notice. These records identify the mortgage program and may show the expected termination date. Request replacement copies if the documents are missing.

Do not subtract PMI from the monthly payment before receiving written approval. An unauthorized short payment could create a delinquency or escrow shortage.

After removal, inspect the next 2 statements and ask about any premium collected after the effective date.

FAQ

Can PMI be removed without refinancing?

Yes. Many conventional borrowers can request cancellation at 80% LTV. Qualifying borrower-paid PMI usually terminates automatically at 78% when the mortgage is current.

Does PMI automatically stop after 5 years?

No universal 5-year rule applies. Removal depends on LTV, payment status, loan age, property value, mortgage type, and investor guidelines.

Will extra mortgage payments remove PMI faster?

Extra principal payments can help the balance reach the 80% request threshold earlier. Contact the servicer because automatic termination may still follow the original amortization schedule.

Can a new appraisal eliminate PMI?

It may support early removal when the servicer accepts current-value cancellation. The lender or investor may require minimum seasoning, strong payment history, and a specific valuation provider.

What if the mortgage servicer refuses to cancel PMI?

Request the reason and applicable policy in writing. Compare the response with the original PMI disclosure and federal guidance from the Consumer Financial Protection Bureau.

Is PMI tax-deductible in 2026?

Do not assume the premium is deductible. Federal tax provisions can change. Verify the current treatment with the IRS or a qualified tax professional before filing.

Earlier we wrote about DIY Dryer Vent Cleaning in 2026: Tools, Costs, Safety Checks, and Common Mistakes