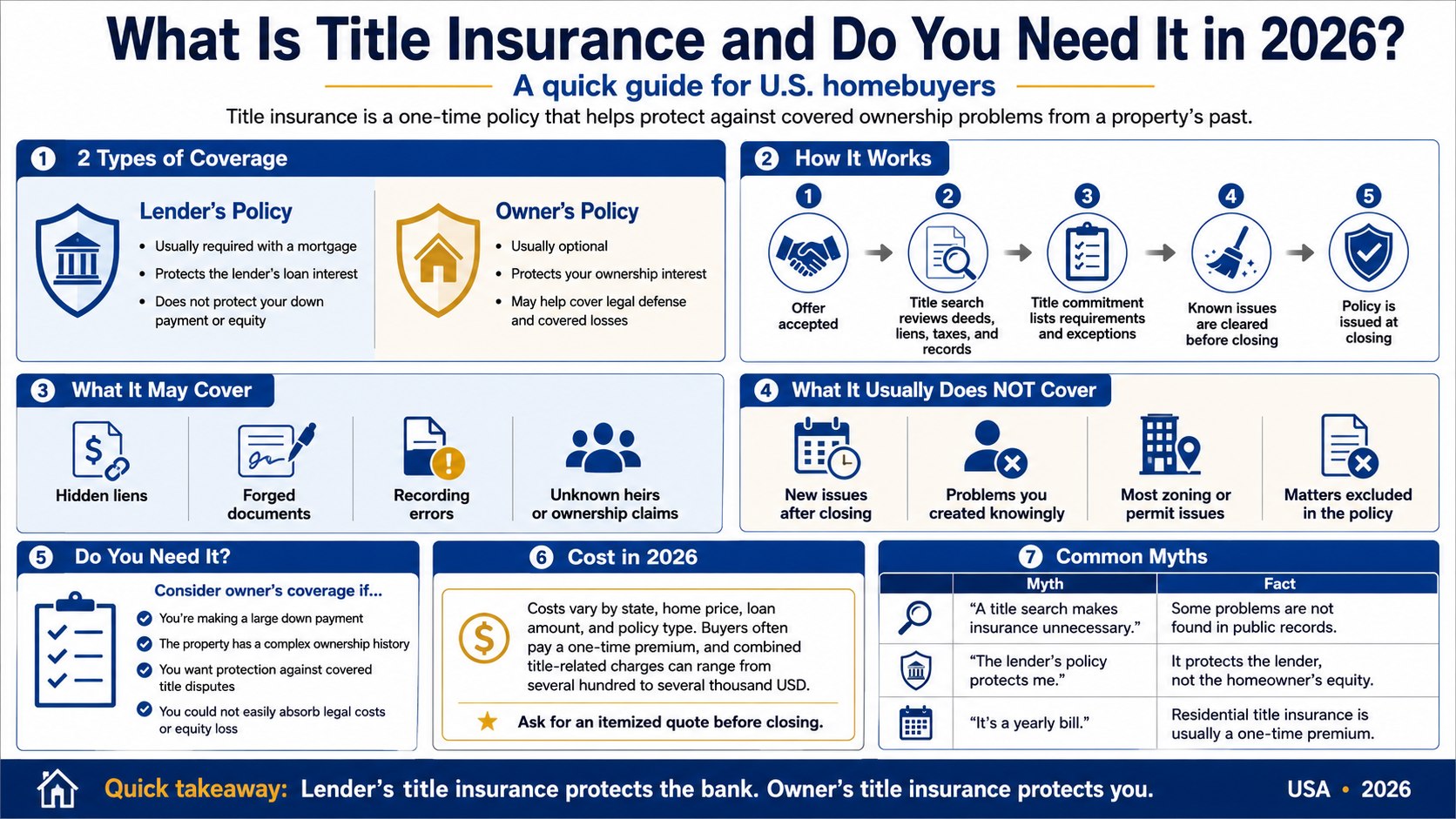

What is title insurance and do you need it? Title insurance is a one-time policy that protects a homebuyer or mortgage lender from covered ownership problems rooted in the property’s past. A lender will usually require its own policy, but that coverage does not protect your down payment or home equity. An owner’s policy is generally optional, yet it can defend your ownership rights and pay covered legal expenses, as the Baltimore Chronicle editorial team notes.

The practical answer is simple. Buyers using a mortgage will probably need lender’s title insurance to close. An owner’s policy deserves serious consideration when losing the property, accumulated equity, or thousands of dollars in legal fees would create financial hardship.

Key takeaways

- Lender’s title insurance protects the mortgage company, not the buyer’s down payment, equity, or ownership rights.

- Owner’s title insurance may cover hidden liens, forged deeds, recording mistakes, unknown heirs, and related legal defense.

- Premiums depend on the state, home price, loan amount, policy form, endorsements, and available package discounts.

A title search lowers risk before closing, but it cannot guarantee that every problem will appear in public records. A forged signature may look valid. An old lien may have been indexed under the wrong name. An unknown heir may challenge a decades-old transfer after the buyer has moved into the home.

In plain English

Think of a property title as the home’s legal biography. It shows who owned the property, which loans were secured against it, and whether another person or organization holds enforceable rights.

A title search is like checking that biography for missing pages and contradictions. An examiner reviews deeds, mortgages, tax records, judgments, easements, probate filings, and other available records.

Title insurance is the backup plan when an undiscovered error survives that review. It does not insure the roof, foundation, plumbing, appliances, or personal property. Those risks belong to homeowners insurance, home warranties, and inspection negotiations.

“The lender’s policy only covers claims affecting the lender’s loan,” explains the Consumer Financial Protection Bureau.

This distinction matters because buyers may see 2 title policies on their closing paperwork and assume they are paying twice for identical protection. They are not. Each policy protects a different financial interest.

How it actually works

The title process usually begins after the seller accepts the buyer’s offer. A title company, settlement company, escrow provider, or real estate attorney receives the contract and starts reviewing the property’s legal history.

The examiner searches public records for defects and competing claims. Common findings include unpaid property taxes, unreleased mortgages, contractor liens, divorce judgments, recording mistakes, easements, and unresolved probate matters.

The title company then issues a preliminary report or title commitment. This document identifies the proposed insured parties, policy amount, requirements, exclusions, and property-specific exceptions.

Known problems usually must be cleared before the insurer issues coverage. A seller might need to pay a tax lien, obtain a missing mortgage release, correct a deed, or secure signatures from additional owners.

At closing, the buyer normally pays a one-time premium. The final policies are issued after the deed and mortgage documents have been signed, funded, and recorded.

- The signed purchase contract reaches the title or settlement provider.

- An examiner searches deeds, mortgages, liens, judgments, taxes, and probate records.

- The insurer issues a title commitment listing requirements and exceptions.

- The parties resolve known defects before ownership changes hands.

- The deed records, funds are released, and the final policies become effective.

The search and the insurance policy perform separate jobs. The search tries to identify defects before money changes hands. The policy responds to certain covered defects discovered after closing.

Title charges are only part of the cash required at settlement. Buyers can compare title premiums, lender fees, taxes, prepaid insurance, and recording expenses in Baltimore Chronicle’s guide to closing costs on a house in 2026.

The final cost should also be compared with the Loan Estimate and Closing Disclosure. A title commitment does not replace either federal mortgage document.

Lender’s title insurance versus owner’s title insurance

The central question is not whether buyers need 2 identical policies. It is whether both the mortgage lender and homeowner need protection for their separate interests.

| Feature | Lender’s title policy | Owner’s title policy |

|---|---|---|

| Protected party | Mortgage lender | Property owner |

| Usually required | Yes, for most financed purchases | No, but commonly recommended |

| Typical insured amount | Original mortgage amount | Usually the purchase price |

| Coverage duration | Generally ends when the insured loan is repaid | Usually continues while the insured owner retains an interest |

| Main purpose | Protects the lender’s lien position | Protects ownership and covered equity |

| Payment method | Usually a one-time closing premium | Usually a one-time closing premium |

Suppose a buyer purchases a $450,000 home with a $360,000 mortgage. The lender’s policy generally protects the lender’s insured interest in the $360,000 loan. It does not automatically reimburse the buyer’s $90,000 down payment.

An owner’s policy may insure the buyer’s interest up to the policy limit. Enhanced policies can provide broader protection than standard forms, although names and available endorsements differ by state.

Large underwriters serving US markets include First American, Fidelity National Title, Old Republic Title, and Stewart. A local title agency may issue a policy backed by one of these companies.

The underwriter’s name matters, but policy language matters more. Buyers should read the exclusions, Schedule B exceptions, endorsements, and claims procedure before closing.

What is title insurance and do you need it for your purchase?

Do you need owner’s title insurance? Federal law does not generally require buyers to purchase it. State rules, lender requirements, local customs, and purchase contracts may still affect the transaction.

The strongest case for coverage involves a property with a complicated ownership history. Warning signs include foreclosure, probate, divorce, tax sales, repeated refinancing, boundary disagreements, or transfers involving trusts and business entities.

Coverage can also matter during an apparently simple suburban purchase. Public records may still contain forged documents, clerical mistakes, undisclosed heirs, or improperly released liens.

Use this checklist before deciding:

- Are you financing the home with a mortgage?

- Could you afford a prolonged ownership lawsuit without insurance?

- Does the title commitment contain unusual exceptions?

- Did the property pass through probate, foreclosure, divorce, or a tax sale?

- Are fences, garages, driveways, or additions close to property lines?

- Is the seller a trust, estate, corporation, or limited liability company?

- Does the survey conflict with the deed or recorded legal description?

- Can you obtain a simultaneous-issue or reissue discount?

A “yes” answer does not prove that a future claim will occur. It means the possible consequences deserve closer review before the buyer waives protection.

Cash buyers are often free to decline lender coverage because no mortgage lender is involved. However, they may have more personal capital exposed because the entire purchase price comes from their own funds.

Title review is one stage of a much larger transaction. Baltimore Chronicle’s guide on how to buy a house in the USA in 2026 covers budgeting, preapproval, property searches, offers, inspections, appraisals, and final closing documents.

Before rejecting an owner’s policy, request the complete title commitment. Discuss unusual exceptions with a qualified local real estate attorney rather than relying only on a verbal explanation.

Who it matters to in 2026

First-time homebuyers

First-time buyers often focus on the mortgage rate, inspection, and down payment. Title charges may appear late in the process and look optional without enough context.

These buyers should separate mandatory lender coverage from optional owner coverage. They should also compare providers before closing-day pressure limits their choices.

Cash buyers and real estate investors

Cash buyers have no lender demanding a policy. Their freedom to decline coverage also leaves them responsible for uncovered ownership losses and legal expenses.

Investors buying foreclosures, inherited properties, vacant lots, or distressed homes should examine the title commitment closely. A fast closing does not shorten the property’s legal history.

Homeowners refinancing in 2026

A refinance commonly requires a new lender’s title policy because the replacement mortgage creates a different insured loan. The owner’s existing policy usually remains connected to the original purchase and insured owner.

Homeowners should ask whether a refinance or reissue rate is available. Eligibility may depend on state rules, the age of the prior policy, and the insurer’s filed rates.

Buyers who see separate escrow charges can review Baltimore Chronicle’s explanation of how escrow works when buying a house. Escrow and title insurance serve different purposes.

Escrow holds funds or documents until contractual conditions are satisfied. Title insurance responds to certain covered defects affecting ownership or the lender’s lien.

How much title insurance costs in 2026

There is no reliable national flat price. Title insurance costs depend on the state, property value, mortgage amount, policy form, endorsements, title search fees, and local regulation.

As of 2026, combined title-related premiums can range from several hundred dollars to several thousand dollars. Expensive homes, larger loans, enhanced policies, and additional endorsements usually increase the bill.

Some states regulate premiums more heavily than others. Texas uses state-regulated title insurance rates. Florida also applies regulated premium structures, while other states permit greater competition among providers.

Local practice can change the final amount. Buyers in New York, Massachusetts, Georgia, and South Carolina may work more closely with closing attorneys. Buyers in California often encounter separate escrow and title service providers.

Some companies reduce the combined premium when lender’s and owner’s policies are issued together. A reissue discount may also apply when an eligible prior policy exists.

Request an itemized quote that separates the following charges:

- Lender’s title insurance premium

- Owner’s title insurance premium

- Title search or examination fee

- Settlement, escrow, or closing fee

- Recording and document preparation charges

- Survey, municipal search, and endorsement costs

Do not compare only the total at the bottom. One quote may include endorsements that another provider lists separately.

Another quote may combine search, settlement, and document fees under one label. Buyers should confirm which party pays every charge under the purchase agreement.

Review the initial Loan Estimate and compare it with the final Closing Disclosure. Ask about any unexplained increase before signing.

What title insurance covers and excludes

A standard owner’s policy may cover losses caused by specified defects that existed before the policy date. Examples can include an undisclosed lien, forged deed, recording error, or another party’s covered ownership claim.

The insurer may defend the homeowner against a covered lawsuit. It may also pay an insured loss up to the policy limit, subject to the contract’s conditions.

Policies usually exclude problems created after closing and defects knowingly caused by the insured. They may also exclude government regulations, eminent domain, environmental conditions, and matters already disclosed in the commitment.

Survey problems, encroachments, unrecorded easements, building permit issues, zoning disputes, and mechanic’s liens may require endorsements or enhanced protection. Availability varies by state and property type.

An owner’s policy is not a promise that the property has no defects. It is a contract covering specific risks, subject to exclusions, exceptions, limits, and notice requirements.

Common myths

- “A clean title search makes insurance unnecessary.” Searches can miss fraud, filing mistakes, and claims absent from public records.

- “The lender’s policy protects the homeowner.” It protects the lender’s insured mortgage interest, not the buyer’s equity.

- “Title insurance requires annual premiums.” Residential policies are generally purchased with a one-time premium.

- “Homeowners insurance covers ownership disputes.” Homeowners insurance mainly covers property damage, belongings, and liability risks.

- “Every title policy provides identical coverage.” Forms, endorsements, exclusions, and state regulations can create major differences.

These myths persist because title work is compressed into the final weeks before closing. Buyers receive several documents containing similar legal terms and unfamiliar charges.

Ask the provider to identify the insured party on each policy. Request the title commitment and a sample policy before the closing appointment.

Check whether enhanced coverage is available and what it adds. Do not assume every endorsement is automatically included.

Keep the final policy after closing. Store it with the recorded deed, survey, purchase contract, settlement statement, and other permanent property records.

FAQ

Is owner’s title insurance legally required?

Owner’s title insurance is generally optional in US residential purchases. A mortgage lender may still require a separate lender’s policy as a condition of financing.

Who normally pays for title insurance?

Payment customs vary by state, county, market, and contract. The buyer may pay both policies, or the seller may cover the owner’s policy in some regions.

Does title insurance cover boundary disputes?

Some policies exclude boundary and survey problems unless an endorsement provides coverage. Review the survey exceptions before closing.

Do cash buyers need title insurance?

Cash buyers can often decline it. They should compare the one-time premium with their exposure to legal fees, liens, and possible ownership loss.

Can I choose my own title company?

Buyers can often shop for title and settlement services. State rules, affiliated business arrangements, and purchase contracts may affect the available options.

What should I do if someone files a title claim?

Notify the title insurer promptly and follow the policy’s claim instructions. Do not settle the dispute or admit liability before receiving legal guidance.

Earlier we wrote about Apple Dual SIM Guide 2026: How US iPhone Owners Can Manage Calls on 2 Numbers